You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Managerial Accounting-Solutions To Ch05Document4 pagesManagerial Accounting-Solutions To Ch05Mohammed HassanNo ratings yet

- (Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountDocument1 page(Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total Amountsrikanth121No ratings yet

- EN-FAB Early Production Facility BrochureDocument22 pagesEN-FAB Early Production Facility Brochurecarmel BarrettNo ratings yet

- Managerial Accounting-Solutions To Ch09Document16 pagesManagerial Accounting-Solutions To Ch09Mohammed Hassan100% (1)

- Target CostingDocument36 pagesTarget CostingImran Umar100% (1)

- Managerial Accounting Ch06Document33 pagesManagerial Accounting Ch06Mohammed HassanNo ratings yet

- Managerial Accounting Ch07Document41 pagesManagerial Accounting Ch07Mohammed HassanNo ratings yet

- Managerial Accounting-Solutions To Ch06Document7 pagesManagerial Accounting-Solutions To Ch06Mohammed HassanNo ratings yet

- Ch09 ProblemsDocument7 pagesCh09 ProblemsMohammed HassanNo ratings yet

- Ch08 ProblemsDocument7 pagesCh08 ProblemsMohammed HassanNo ratings yet

- Managerial Accounting-Solutions To Ch08Document4 pagesManagerial Accounting-Solutions To Ch08Mohammed HassanNo ratings yet

- Managerial Accounting-Solutions To Ch07Document7 pagesManagerial Accounting-Solutions To Ch07Mohammed HassanNo ratings yet

- Ch07 ProblemsDocument6 pagesCh07 ProblemsMohammed HassanNo ratings yet

- Ch06 ProblemsDocument5 pagesCh06 ProblemsMohammed HassanNo ratings yet

- Ch05 ProblemsDocument3 pagesCh05 ProblemsMohammed HassanNo ratings yet

- CHAPTER 2 - Financial Reporting and Analysis-1Document16 pagesCHAPTER 2 - Financial Reporting and Analysis-1Mohammed HassanNo ratings yet

- Supply Chain of IciciDocument17 pagesSupply Chain of Icicishan birla100% (1)

- AMCAT Aptitude QuestionsDocument10 pagesAMCAT Aptitude QuestionsFast Tech Gadget'sNo ratings yet

- R34 Measures of LeverageDocument12 pagesR34 Measures of LeverageMoataz EmadNo ratings yet

- Impulse Technical, Nifty Algo Performance Sheet 50000Document17 pagesImpulse Technical, Nifty Algo Performance Sheet 50000Video JunctionNo ratings yet

- AJIO Null 1627137756324Document1 pageAJIO Null 1627137756324Rishi Kumar SinghNo ratings yet

- Tenets of Effective Monetary Policy in The Philippines: Jasmin E. DacioDocument14 pagesTenets of Effective Monetary Policy in The Philippines: Jasmin E. DacioKathyNo ratings yet

- Doctrine of MarshallingDocument4 pagesDoctrine of MarshallingchitraNo ratings yet

- SC&LogisticDocument15 pagesSC&LogisticSwti BhattNo ratings yet

- Steel Works Inventory+TablesDocument8 pagesSteel Works Inventory+TablesphitchowNo ratings yet

- Entreprepreneurship, Seminar TopicDocument13 pagesEntreprepreneurship, Seminar Topicadityakalani000oooNo ratings yet

- Inventory Management Implementation Model Based On SAK EMKM in Maintaining The Continuity of Micro and Small Businesses in Gorontalo CityDocument8 pagesInventory Management Implementation Model Based On SAK EMKM in Maintaining The Continuity of Micro and Small Businesses in Gorontalo CityInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Vikas Provisional ComputationDocument6 pagesVikas Provisional ComputationAmit TyagiNo ratings yet

- Empowered 4x - Final PresentationDocument22 pagesEmpowered 4x - Final Presentationapi-386295949No ratings yet

- Current Status of Derivative Products in India: An OverviewDocument17 pagesCurrent Status of Derivative Products in India: An OverviewSarojKumarSinghNo ratings yet

- Applied EconomicsDocument184 pagesApplied EconomicsMichael ZinampanNo ratings yet

- Crop and Water Productivity, Energy Auditing, Carbon Footprints and Soil Health Indicators of Bt-Cotton Transplanting Led System IntensificationDocument3 pagesCrop and Water Productivity, Energy Auditing, Carbon Footprints and Soil Health Indicators of Bt-Cotton Transplanting Led System IntensificationAmanNo ratings yet

- Large Long Period Difficult To Reverse So Much Risks UncertaintiesDocument13 pagesLarge Long Period Difficult To Reverse So Much Risks UncertaintiesLaila ContadoNo ratings yet

- San Mateo Municipal College: Accounting Information System Midterms Activity Understanding A Relational DatabaseDocument2 pagesSan Mateo Municipal College: Accounting Information System Midterms Activity Understanding A Relational Database버니 모지코No ratings yet

- In-Company Training BrochureDocument1 pageIn-Company Training BrochureRabia JamilNo ratings yet

- Management Accounting Versus Financial Accounting.: Takele - Fufa@aau - Edu.et...... orDocument6 pagesManagement Accounting Versus Financial Accounting.: Takele - Fufa@aau - Edu.et...... orDeselagn TefariNo ratings yet

- (IMF Working Papers) Front MatterDocument3 pages(IMF Working Papers) Front MatterHoucine AchmakouNo ratings yet

- 37 Practice+Questions+ (Working+Capital+Management)Document4 pages37 Practice+Questions+ (Working+Capital+Management)bahaa madiNo ratings yet

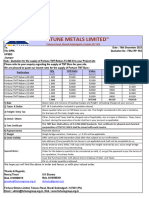

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Document1 page"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaNo ratings yet

- Invoice For Harbor Real Estate Dubai: CampaignsDocument2 pagesInvoice For Harbor Real Estate Dubai: CampaignsSyed Faseeh Ul HassanNo ratings yet

- Digital Marketing Assignment 2Document15 pagesDigital Marketing Assignment 2Bright MuzaNo ratings yet

- Train LawDocument3 pagesTrain Lawelisha1227No ratings yet

- Penilaian Kualitas Kinerja Keuangan Perusahaan PerDocument16 pagesPenilaian Kualitas Kinerja Keuangan Perusahaan PerCABE GEMINGNo ratings yet