You might also like

- Computer Maintenace Proposal Cost PDFDocument4 pagesComputer Maintenace Proposal Cost PDFjimoh0% (2)

- Bank Call Center - ProjectDocument9 pagesBank Call Center - ProjectSampath Kumar100% (1)

- Lion Financial ServicesDocument3 pagesLion Financial Servicesjeff mathews0% (1)

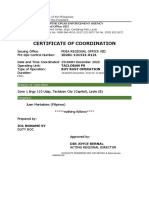

- Certificate of Coordination: Area(s) of OperationDocument3 pagesCertificate of Coordination: Area(s) of OperationervingabralagbonNo ratings yet

- BIR - Ruling - DA - C-148 - 406-09 - Collection On Behalf of NRFC Not Subject To WHTDocument6 pagesBIR - Ruling - DA - C-148 - 406-09 - Collection On Behalf of NRFC Not Subject To WHTjohn allen MarillaNo ratings yet

- Bir Ruling (Da 013 08)Document5 pagesBir Ruling (Da 013 08)Jake PeraltaNo ratings yet

- Kisan Call CentreDocument5 pagesKisan Call CentrePartha Pratim BharaliNo ratings yet

- EILER Final Report Transport-Related Call CenterDocument38 pagesEILER Final Report Transport-Related Call CenterNa LeNo ratings yet

- Commissioner - of - Internal - Revenue - v. - J.P. (TAX)Document17 pagesCommissioner - of - Internal - Revenue - v. - J.P. (TAX)Mary Rocelyn PabalayNo ratings yet

- #4. CIR Vs Morgan Bank. FTDocument9 pages#4. CIR Vs Morgan Bank. FTeizNo ratings yet

- CIR-v-JP MorganDocument14 pagesCIR-v-JP Morganclaudine uananNo ratings yet

- CIR Vs Chase BankDocument15 pagesCIR Vs Chase BankDianne Pari-an MedianeroNo ratings yet

- Contract of Subscription (OE TEKNIK MFG. CORP.)Document7 pagesContract of Subscription (OE TEKNIK MFG. CORP.)Violiza Mae RequirosoNo ratings yet

- ChhhaaarrrDocument3 pagesChhhaaarrredhen01No ratings yet

- 2022 September-BcpDocument10 pages2022 September-BcpHenry PalayaNo ratings yet

- Atomic Excellence Inc CaseDocument5 pagesAtomic Excellence Inc CaseZaighum SattarNo ratings yet

- Adv - IT Project Cost - FinalDocument10 pagesAdv - IT Project Cost - FinalAdamNo ratings yet

- Pdo Software ContractDocument7 pagesPdo Software Contractasif abdullahNo ratings yet

- Policy 2Document5 pagesPolicy 2RinkeshNo ratings yet

- Sample PMS Terms and ConditionsDocument12 pagesSample PMS Terms and ConditionsJosh Qc OngNo ratings yet

- MOA Amendment - Remittance Agent 8.30.2023 - 102015Document7 pagesMOA Amendment - Remittance Agent 8.30.2023 - 102015Precious Marga BaldeoNo ratings yet

- (2016) Sgca 19Document43 pages(2016) Sgca 19DavidNo ratings yet

- Week 2 TutorialDocument3 pagesWeek 2 TutorialnikhilNo ratings yet

- Contract of Services BerrengerveloxposDocument5 pagesContract of Services BerrengerveloxposRob ClosasNo ratings yet

- Position Paper - Arnold Carlos JMC RGC FZD JMCDocument23 pagesPosition Paper - Arnold Carlos JMC RGC FZD JMCRob LimNo ratings yet

- 3metropolitan Bank Trust Co. v. Fortuna20210429-11-17b3lihDocument29 pages3metropolitan Bank Trust Co. v. Fortuna20210429-11-17b3lihChristian John Dela CruzNo ratings yet

- Invitation For Expressions of InterestDocument16 pagesInvitation For Expressions of InterestRangga PermanaNo ratings yet

- Comments On The Findings Re On Site Inspection Dated 26 May 2022Document2 pagesComments On The Findings Re On Site Inspection Dated 26 May 2022Bplo CaloocanNo ratings yet

- Terms of Reference Project: Procurement of Manpower Services (Technical and Administrative Support) Fornhmfc For Cy 2020Document14 pagesTerms of Reference Project: Procurement of Manpower Services (Technical and Administrative Support) Fornhmfc For Cy 2020Shin SilvaNo ratings yet

- Utkarsh Small Finance BankDocument5 pagesUtkarsh Small Finance Banklovkyadav001No ratings yet

- Project Charter ScriptDocument4 pagesProject Charter ScriptRomen Samuel WabinaNo ratings yet

- Petitioner Vs Vs Respondent: Second DivisionDocument26 pagesPetitioner Vs Vs Respondent: Second DivisionSabNo ratings yet

- VSI Tapestry SOC 2Document7 pagesVSI Tapestry SOC 2NaveenchdrNo ratings yet

- Dela Cruz, Junel BDocument7 pagesDela Cruz, Junel BEden Dela CruzNo ratings yet

- BIR Ruling (DA-219-08)Document4 pagesBIR Ruling (DA-219-08)amadieuNo ratings yet

- Manoj K. Sharma: Worked On Country Version India Experienced in End User Assignment and 2 Support ProjectsDocument5 pagesManoj K. Sharma: Worked On Country Version India Experienced in End User Assignment and 2 Support ProjectssanjayNo ratings yet

- 4-Pager EADDocument4 pages4-Pager EADSarah SanoyNo ratings yet

- CCCCCCCC C !"C CDocument8 pagesCCCCCCCC C !"C CMichael Joe ToqueroNo ratings yet

- Retainers ContractDocument3 pagesRetainers ContractMeldin Arnold LimNo ratings yet

- Enable AP-Subscription Payment Collection System - 20091114Document9 pagesEnable AP-Subscription Payment Collection System - 20091114Cecil OwensNo ratings yet

- Reaction PaperDocument3 pagesReaction PaperChieMae Benson QuintoNo ratings yet

- Republic of The PhilippinesDocument3 pagesRepublic of The PhilippinesLara Mae Alfonso AndresNo ratings yet

- SBC Case StudyDocument5 pagesSBC Case StudyRaniel MamaspasNo ratings yet

- Citizen CharterDocument10 pagesCitizen CharterSatyajit PatraNo ratings yet

- RTP May2022 - Paper 7 EISSMDocument26 pagesRTP May2022 - Paper 7 EISSMYash YashwantNo ratings yet

- All Yr RTP Eis SMDocument225 pagesAll Yr RTP Eis SMShivam ChaudharyNo ratings yet

- Basic Procurement Management PlanDocument44 pagesBasic Procurement Management PlanNinna RiveraNo ratings yet

- Erawan (ASEANA) - PME - Plum - Civivl Certification Cost Proposal 2023Document2 pagesErawan (ASEANA) - PME - Plum - Civivl Certification Cost Proposal 2023Rhowelle TibayNo ratings yet

- Bidding Document Banking Reconciliation System - 0Document9 pagesBidding Document Banking Reconciliation System - 0Usman AmjadNo ratings yet

- The Extent To Which The Philippine Government Complied To Sections 27 and 28 of RDocument8 pagesThe Extent To Which The Philippine Government Complied To Sections 27 and 28 of RJanine PagtakhanNo ratings yet

- A Communication Plan A Detailed Asset Inventory A Data Restoration Priority Plan A Vendor Communication and Service Restoration PlanDocument4 pagesA Communication Plan A Detailed Asset Inventory A Data Restoration Priority Plan A Vendor Communication and Service Restoration PlanCông ĐạiNo ratings yet

- Final Report Loan RecoveryDocument35 pagesFinal Report Loan RecoveryPriyadharsshini100% (1)

- Computer Related: Repair and ServicesDocument11 pagesComputer Related: Repair and ServicesDan Maxwel Facinag VocalNo ratings yet

- Determination of Retention Fees For Dev-Asstd HL Accts and Transfer or Reg Fees For Retail HL AcctsDocument2 pagesDetermination of Retention Fees For Dev-Asstd HL Accts and Transfer or Reg Fees For Retail HL AcctsJonniel De GuzmanNo ratings yet

- Guidelines On Streamlining of Lgu Systems and Procedures On Business and Nonbusiness-Related Services For Cities and MunicipalitiesDocument30 pagesGuidelines On Streamlining of Lgu Systems and Procedures On Business and Nonbusiness-Related Services For Cities and MunicipalitiesStefhanie Khristine PormanesNo ratings yet

- MySAP Proposal CDocument86 pagesMySAP Proposal CNabeel RashidNo ratings yet

- Moa With LBPDocument12 pagesMoa With LBPryveducationNo ratings yet

- AaaaaaaaaDocument2 pagesAaaaaaaaachangbin love botNo ratings yet

- (STP) - As A Part of This Scheme, MIT Has Taken The Right Step at The Right Time in Establishing TheDocument25 pages(STP) - As A Part of This Scheme, MIT Has Taken The Right Step at The Right Time in Establishing TheJhilik PradhanNo ratings yet

- SETUP PresentationDocument23 pagesSETUP PresentationMark Vincent Jayson BaliñaNo ratings yet

- Tax Treatment of Software Payments FINALDocument20 pagesTax Treatment of Software Payments FINALEarl Charles VillarinNo ratings yet

- BPO Module 01Document15 pagesBPO Module 01Marinette MedranoNo ratings yet

- Direct InteractionsDocument14 pagesDirect InteractionsDan MonkNo ratings yet

- Daisy Samue: AnalystDocument2 pagesDaisy Samue: AnalystSAYALNo ratings yet

- 21St Century Computer Solutions: A Manual Accounting SimulationFrom Everand21St Century Computer Solutions: A Manual Accounting SimulationNo ratings yet

- Legal & Judicial Ethics & Practical Exercises SyllabusDocument8 pagesLegal & Judicial Ethics & Practical Exercises Syllabuservingabralagbon100% (1)

- Tacloban City Police Station: Hotline - 0998.598.6680Document2 pagesTacloban City Police Station: Hotline - 0998.598.6680ervingabralagbonNo ratings yet

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- People Vs MarbabiesDocument3 pagesPeople Vs MarbabieservingabralagbonNo ratings yet

- Ethics - FINALS - Additional CasesDocument12 pagesEthics - FINALS - Additional CaseservingabralagbonNo ratings yet

- 36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0Document10 pages36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0ervingabralagbonNo ratings yet

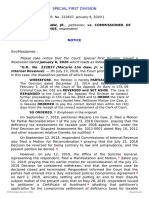

- 46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)Document9 pages46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)ervingabralagbonNo ratings yet

- 35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iDocument11 pages35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iervingabralagbonNo ratings yet

- 53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfDocument20 pages53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfervingabralagbonNo ratings yet

- Petitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueDocument19 pagesPetitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueervingabralagbonNo ratings yet

- Verint Managing Performance Back-Office Operations PDFDocument3 pagesVerint Managing Performance Back-Office Operations PDFBram ArdhiNo ratings yet

- LivePerson Chat ReportsDocument23 pagesLivePerson Chat ReportsEdenEtfNo ratings yet

- Capital OneDocument3 pagesCapital OneSoham PradhanNo ratings yet

- Icm 75 SchemaDocument649 pagesIcm 75 Schemavipinco2003No ratings yet

- Multiple QueuesDocument3 pagesMultiple Queuestuberose_13847748No ratings yet

- Blinc 360 and Ajna TechDocument14 pagesBlinc 360 and Ajna TechAlkame IncNo ratings yet

- Applications Customer Support Engineer in Burlington VT Resume Jeramy HammerDocument2 pagesApplications Customer Support Engineer in Burlington VT Resume Jeramy HammerJeramyHammerNo ratings yet

- Sip G7Document6 pagesSip G7routemansNo ratings yet

- Siebel CRMDocument16 pagesSiebel CRMshardullavandeNo ratings yet

- The Past, Present and Future of CRMDocument14 pagesThe Past, Present and Future of CRMRafaat Shaeer100% (1)

- Siebel 8 Applications - Technical Architecture Overview - V811Document87 pagesSiebel 8 Applications - Technical Architecture Overview - V811jorge_r_souza100% (3)

- Call Center Operations Improvement Business Case Sample PresentationDocument16 pagesCall Center Operations Improvement Business Case Sample PresentationMohammad Abd Alrahim ShaarNo ratings yet

- Avaya Aura Contact Center - Installation and Configuration: Duration: 5 Days Course Code: 3608CDocument2 pagesAvaya Aura Contact Center - Installation and Configuration: Duration: 5 Days Course Code: 3608CHaris SetiawanNo ratings yet

- T-Bytes Digital Customer Experience February Edition 2021Document82 pagesT-Bytes Digital Customer Experience February Edition 2021IT ShadesNo ratings yet

- Service Desk: Process FactsheetDocument3 pagesService Desk: Process FactsheetPaul James BirchallNo ratings yet

- AACC CS1000 Deployment GuideDocument414 pagesAACC CS1000 Deployment GuideCarlos TejadaNo ratings yet

- Uniphore - LeadershipDocument2 pagesUniphore - LeadershipconnectindiaNo ratings yet

- Tshepo Letsatsi Credit Report Nov 2019Document6 pagesTshepo Letsatsi Credit Report Nov 2019Thabiso letsatsiNo ratings yet

- Call Center Job Duties and ResponsibilitiesDocument2 pagesCall Center Job Duties and ResponsibilitiesOlaya alghareniNo ratings yet

- Avaya Call Recording: Graphical User InterfaceDocument4 pagesAvaya Call Recording: Graphical User InterfacejyotikothariNo ratings yet

- Top Interview Questions With Sample AnswersDocument8 pagesTop Interview Questions With Sample AnswersChanNo ratings yet

- Starlink Call CenterDocument1 pageStarlink Call Centerchaima bacNo ratings yet

- Research Paper Call CenterDocument4 pagesResearch Paper Call Centerrpmvtcrif100% (3)

- Indian Railways Conference With Industry and AcademiaDocument17 pagesIndian Railways Conference With Industry and AcademiaJigisha VasaNo ratings yet

- CALL CENTER Interview Questions N AnsDocument9 pagesCALL CENTER Interview Questions N AnsMohammed UmrazuddinNo ratings yet

- Siebel Marketing Manager Activity - GuideDocument55 pagesSiebel Marketing Manager Activity - Guidemanasamba33No ratings yet