You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

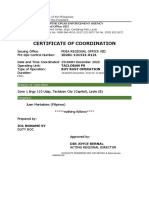

- Certificate of Coordination: Area(s) of OperationDocument3 pagesCertificate of Coordination: Area(s) of OperationervingabralagbonNo ratings yet

- Legal & Judicial Ethics & Practical Exercises SyllabusDocument8 pagesLegal & Judicial Ethics & Practical Exercises Syllabuservingabralagbon100% (1)

- Tacloban City Police Station: Hotline - 0998.598.6680Document2 pagesTacloban City Police Station: Hotline - 0998.598.6680ervingabralagbonNo ratings yet

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- People Vs MarbabiesDocument3 pagesPeople Vs MarbabieservingabralagbonNo ratings yet

- Ethics - FINALS - Additional CasesDocument12 pagesEthics - FINALS - Additional CaseservingabralagbonNo ratings yet

- 36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0Document10 pages36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0ervingabralagbonNo ratings yet

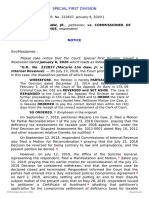

- 46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)Document9 pages46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)ervingabralagbonNo ratings yet

- 35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iDocument11 pages35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iervingabralagbonNo ratings yet

- Petitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueDocument19 pagesPetitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueervingabralagbonNo ratings yet

- 53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfDocument20 pages53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfervingabralagbonNo ratings yet

- 48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedDocument19 pages48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedervingabralagbonNo ratings yet

- VAT in Oracle EBSDocument8 pagesVAT in Oracle EBSAbhishek IyerNo ratings yet

- Third Division: Republic of Philippines Court of Tax Appeals QuezonDocument8 pagesThird Division: Republic of Philippines Court of Tax Appeals Quezonنيسريو جينوNo ratings yet

- 2019 - ACA Exam Dates and Deadlines - WebDocument2 pages2019 - ACA Exam Dates and Deadlines - WebSree Mathi SuntheriNo ratings yet

- Business and Other Transfer Taxes - PrelimDocument47 pagesBusiness and Other Transfer Taxes - PrelimYoseph WooNo ratings yet

- Ram BillDocument1 pageRam BillHarish Babu N KNo ratings yet

- Income Tax 2nd Quiz PrelimDocument5 pagesIncome Tax 2nd Quiz PrelimRenalyn ParasNo ratings yet

- Reissued Statement Reissued Statement: OMB No. 1545-0008 OMB No. 1545-0008Document1 pageReissued Statement Reissued Statement: OMB No. 1545-0008 OMB No. 1545-0008Sadiki LuhandeNo ratings yet

- Chap 001Document85 pagesChap 001Rong GuoNo ratings yet

- Tex BD Trading Corporation: Ahsania Mission Cancer & General HospitalDocument2 pagesTex BD Trading Corporation: Ahsania Mission Cancer & General HospitalMilon IslamNo ratings yet

- P2P Technical DetailesDocument5 pagesP2P Technical DetailesDoifode PralhadNo ratings yet

- Samsung 6.5 KG Activwash+ Fully Automatic Top Load Grey: 048P5Pbn100022Document1 pageSamsung 6.5 KG Activwash+ Fully Automatic Top Load Grey: 048P5Pbn100022Ravindar aNo ratings yet

- Basic Taxation - CAVSU - Teaching Demo - Feb 5, 2018Document30 pagesBasic Taxation - CAVSU - Teaching Demo - Feb 5, 2018Renalyn ParasNo ratings yet

- Trident Embassy Reso Price List-6Document2 pagesTrident Embassy Reso Price List-6praveenNo ratings yet

- Centre State RelationshipDocument3 pagesCentre State RelationshippritamNo ratings yet

- RequiredDocument2 pagesRequiredmohitgaba19No ratings yet

- Summary & Career Objective:: Curriculum VitaeDocument3 pagesSummary & Career Objective:: Curriculum VitaeJnanamNo ratings yet

- Ops Amw FRM D en SalesTaxAdjustmentForm AllStatesExceptWA2013Document6 pagesOps Amw FRM D en SalesTaxAdjustmentForm AllStatesExceptWA2013Ma'at MutamuntatNo ratings yet

- Form16 Fiserv 2018-19Document8 pagesForm16 Fiserv 2018-19SiddharthNo ratings yet

- Carmelino Pansacola v. CIRDocument2 pagesCarmelino Pansacola v. CIRVince MontealtoNo ratings yet

- Vanishing Deductions X Estate Tax ComputationDocument2 pagesVanishing Deductions X Estate Tax ComputationShiela Mae OblanNo ratings yet

- Assignment On Income From House PropertyDocument17 pagesAssignment On Income From House PropertySandeep ChawdaNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BMaddy GamerNo ratings yet

- Ann Julienne Aristoza Income Tax MatrixDocument5 pagesAnn Julienne Aristoza Income Tax MatrixJul A.No ratings yet

- Nitafan v. Cir Case DigestDocument1 pageNitafan v. Cir Case DigestNina Majica PagaduanNo ratings yet

- PF InvoiceDocument1 pagePF InvoiceALOKE GANGULYNo ratings yet

- Cost Flow ProductionDocument1 pageCost Flow ProductionHuzaifa WaseemNo ratings yet

- Assignment 01 Capital BudgetingDocument1 pageAssignment 01 Capital BudgetingChrisNo ratings yet

- EY Philippines Tax Bulletin July 2016Document26 pagesEY Philippines Tax Bulletin July 2016evealyn.gloria.wat20No ratings yet

- Installment MethodDocument2 pagesInstallment MethodevaNo ratings yet