You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Hydrostatic Test Pressure For Flanges PDFDocument2 pagesHydrostatic Test Pressure For Flanges PDFChegg ChemNo ratings yet

- Financial Management Solution ZHJJJJJJJZBBZBZBBZDocument4 pagesFinancial Management Solution ZHJJJJJJJZBBZBZBBZJoylyn CombongNo ratings yet

- Econ 122 Week 1-9 by DwexDocument19 pagesEcon 122 Week 1-9 by Dwexjohn100% (3)

- QAMDocument10 pagesQAMRavi Krishna IIM, CalcuttaNo ratings yet

- Framework Quiz 1Document16 pagesFramework Quiz 1Joylyn CombongNo ratings yet

- Cabug-Os, Lovely A. (Assignment 6)Document8 pagesCabug-Os, Lovely A. (Assignment 6)Joylyn CombongNo ratings yet

- FdsedjwhajdhkudshdhxDocument28 pagesFdsedjwhajdhkudshdhxJoylyn CombongNo ratings yet

- Assignment 7 On Chapt 3 Problem 3 17 On Page 93Document2 pagesAssignment 7 On Chapt 3 Problem 3 17 On Page 93Joylyn CombongNo ratings yet

- Cabug-Os, Lovely A. (Assignment 7)Document2 pagesCabug-Os, Lovely A. (Assignment 7)Joylyn CombongNo ratings yet

- Final Exam Good GovernanceDocument2 pagesFinal Exam Good GovernanceJoylyn CombongNo ratings yet

- Cabug-Os, Lovely A. (Assignment 9)Document2 pagesCabug-Os, Lovely A. (Assignment 9)Joylyn CombongNo ratings yet

- Cabug-Os, Lovely A. (Assignment 7)Document2 pagesCabug-Os, Lovely A. (Assignment 7)Joylyn CombongNo ratings yet

- Answers To Assignment 1Document3 pagesAnswers To Assignment 1Joylyn CombongNo ratings yet

- Assignment 6Document12 pagesAssignment 6Joylyn CombongNo ratings yet

- Cabug-Os, Lovely A. (Assignment 7)Document2 pagesCabug-Os, Lovely A. (Assignment 7)Joylyn CombongNo ratings yet

- Common Mistakes of Students To Financial Activities: FL - Erudition Free Webinar by Abm 12Document38 pagesCommon Mistakes of Students To Financial Activities: FL - Erudition Free Webinar by Abm 12Larisha Frixie M. DanlagNo ratings yet

- Spectrum BillDocument2 pagesSpectrum BilldrikiddoNo ratings yet

- Nmat Quantitative Simulations (Mock 2) Section 1. Fundamental OperationsDocument2 pagesNmat Quantitative Simulations (Mock 2) Section 1. Fundamental OperationsRACKELLE ANDREA SERRANONo ratings yet

- NR - EE Chapter IDocument15 pagesNR - EE Chapter IGetachew GurmuNo ratings yet

- Clearance of BungroDocument88 pagesClearance of BungroApril Joy Sumagit HidalgoNo ratings yet

- ECON 200 F. Introduction To Microeconomics Homework 3 Name: - (Multiple Choice)Document11 pagesECON 200 F. Introduction To Microeconomics Homework 3 Name: - (Multiple Choice)Phan Hồng VânNo ratings yet

- Excerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalDocument34 pagesExcerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalKaren PerezNo ratings yet

- 600 - Materiality AvayaDocument19 pages600 - Materiality AvayaBrayan Nicolás Martínez RomeroNo ratings yet

- ECON3124 Behavioural Economics S12013 PartADocument7 pagesECON3124 Behavioural Economics S12013 PartAsyamilNo ratings yet

- Instruction Manual Blower Drive UnitDocument242 pagesInstruction Manual Blower Drive UnitBambang PriyambodoNo ratings yet

- An Introduction To Game TheoryDocument17 pagesAn Introduction To Game TheoryNicolas AliasNo ratings yet

- DOC-20240405-WA0001.Document7 pagesDOC-20240405-WA0001.Swetha PvNo ratings yet

- Product Manual For Plugs and Socket-Outlets For Household and Similar Purposes of Rated Voltage Up To and Including 250 V and Rated Current Up To and Including 16 A According ToDocument13 pagesProduct Manual For Plugs and Socket-Outlets For Household and Similar Purposes of Rated Voltage Up To and Including 250 V and Rated Current Up To and Including 16 A According Toakki3007No ratings yet

- Bargarh Handloom and Agro Producer CompanyDocument2 pagesBargarh Handloom and Agro Producer CompanyOrmas OdishaNo ratings yet

- BWN TicketDocument3 pagesBWN TicketSOUMMYA KARMAKARNo ratings yet

- Economy of OmanDocument8 pagesEconomy of OmanAman DecoraterNo ratings yet

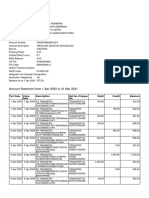

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNo ratings yet

- Sr. No. Name Contact Number Vendor: Kartik TanwarDocument8 pagesSr. No. Name Contact Number Vendor: Kartik TanwarAbhigyan MaityNo ratings yet

- Vacuum Packaging Manual New KorDocument44 pagesVacuum Packaging Manual New KorSameer KhanNo ratings yet

- PDFDocument7 pagesPDFNikhilreddy SingireddyNo ratings yet

- Final Corporate StrategyDocument1 pageFinal Corporate Strategyqikangdong7No ratings yet

- Strathern - Women in BetweenDocument392 pagesStrathern - Women in BetweenHelô SouzaNo ratings yet

- Product Roadmap Template LightDocument8 pagesProduct Roadmap Template LightDaniel MachadoNo ratings yet

- FLC Application FormDocument10 pagesFLC Application FormMuhammad Zaheer NaivasalNo ratings yet

- Comparative Development Expericences of India Its NeigborsDocument30 pagesComparative Development Expericences of India Its NeigborsshivangiNo ratings yet

- Trade Name Reservation ReceiptDocument1 pageTrade Name Reservation ReceiptHORUS TYPING & P.R.O SERVICESNo ratings yet

- IFYEC002 Economics (Автосохраненный)Document11 pagesIFYEC002 Economics (Автосохраненный)bunyod radjabovNo ratings yet