You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- User Types - MarczewskiDocument13 pagesUser Types - MarczewskiAriel JaraNo ratings yet

- Perumal Thirumozhi Pt1Document104 pagesPerumal Thirumozhi Pt1kok_oc25No ratings yet

- Robbery Complaint Ate GinaDocument6 pagesRobbery Complaint Ate GinaJameson UyNo ratings yet

- 35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iDocument11 pages35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iervingabralagbonNo ratings yet

- Accountancy NotesDocument198 pagesAccountancy NotesHaider Shah100% (2)

- FCE Result Revised SBDocument177 pagesFCE Result Revised SBInês Carvalho86% (7)

- Legal & Judicial Ethics & Practical Exercises SyllabusDocument8 pagesLegal & Judicial Ethics & Practical Exercises Syllabuservingabralagbon100% (1)

- Business Plan For Layer Cake BakeryDocument9 pagesBusiness Plan For Layer Cake BakeryHuong PhamNo ratings yet

- Certificate of Coordination: Area(s) of OperationDocument3 pagesCertificate of Coordination: Area(s) of OperationervingabralagbonNo ratings yet

- Tacloban City Police Station: Hotline - 0998.598.6680Document2 pagesTacloban City Police Station: Hotline - 0998.598.6680ervingabralagbonNo ratings yet

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- People Vs MarbabiesDocument3 pagesPeople Vs MarbabieservingabralagbonNo ratings yet

- 36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0Document10 pages36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0ervingabralagbonNo ratings yet

- Ethics - FINALS - Additional CasesDocument12 pagesEthics - FINALS - Additional CaseservingabralagbonNo ratings yet

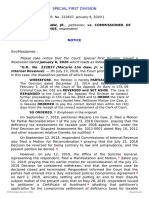

- 46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)Document9 pages46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)ervingabralagbonNo ratings yet

- 53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfDocument20 pages53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfervingabralagbonNo ratings yet

- 48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedDocument19 pages48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedervingabralagbonNo ratings yet

- Petitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueDocument19 pagesPetitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueervingabralagbonNo ratings yet

- Question-02 Human Resource ManagementDocument4 pagesQuestion-02 Human Resource ManagementRiya SinghNo ratings yet

- EN-eng 11A2 speed-control-configuration-PWM ModuleDocument7 pagesEN-eng 11A2 speed-control-configuration-PWM ModuleSreepriodas RoyNo ratings yet

- PRESS RELEASE Babylon Whore Mother of ProstitutesDocument6 pagesPRESS RELEASE Babylon Whore Mother of ProstitutesMichael MeadeNo ratings yet

- Java QADocument11 pagesJava QADeepa SureshNo ratings yet

- MediCard - MACE - Version 2 - User Manual - Coordinator - 10062017 - 1.19 - 2 PDFDocument80 pagesMediCard - MACE - Version 2 - User Manual - Coordinator - 10062017 - 1.19 - 2 PDFRonamae Pardiñas InteriorrNo ratings yet

- Job Recommendation Systems A Literature ReviewDocument4 pagesJob Recommendation Systems A Literature ReviewInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Cdot An-RaxDocument46 pagesCdot An-Raxneeraj kumar singh100% (2)

- Planning Zoning OrdinanceDocument253 pagesPlanning Zoning OrdinanceTrbvm0% (1)

- DBMS Unit-8 9Document67 pagesDBMS Unit-8 9hetmovaliya0010No ratings yet

- Form Generation in Architecture PDFDocument266 pagesForm Generation in Architecture PDFJudith AndresNo ratings yet

- UT Dallas Syllabus For Psy4343.001.09f Taught by Marion Underwood (Undrwd)Document5 pagesUT Dallas Syllabus For Psy4343.001.09f Taught by Marion Underwood (Undrwd)UT Dallas Provost's Technology GroupNo ratings yet

- Ffa24 084Document1 pageFfa24 084basilkollarmaliNo ratings yet

- Ethiopia - 2003 - Local Content Development Status and TrendsDocument152 pagesEthiopia - 2003 - Local Content Development Status and TrendsAmaha Diana0% (1)

- HIV/AIDS and The Family: A Review of Research in The First DecadeDocument18 pagesHIV/AIDS and The Family: A Review of Research in The First Decadevanessa waltersNo ratings yet

- Eman 21/11/2020: Class 9 Subject: Chemistry Topic: Chapter 5 and 6 (Moles)Document1 pageEman 21/11/2020: Class 9 Subject: Chemistry Topic: Chapter 5 and 6 (Moles)Rizwan AhmedNo ratings yet

- Grade 10 - 1st Monthly Exams - ScienceDocument21 pagesGrade 10 - 1st Monthly Exams - ScienceInah MasubayNo ratings yet

- Arcadia Share and Stock Broker PVT LTDDocument20 pagesArcadia Share and Stock Broker PVT LTDdivya priyaNo ratings yet

- Total Quiz HRM627Document28 pagesTotal Quiz HRM627Syed Faisal BukhariNo ratings yet

- Silo TipsDocument71 pagesSilo TipssitiNo ratings yet

- Chap 009Document24 pagesChap 009ShaifaliChauhanNo ratings yet

- Galvan y CompanaDocument1 pageGalvan y Companaangelo doceoNo ratings yet

- Valence Changing OperationsDocument13 pagesValence Changing OperationsTirza FrançaNo ratings yet

- Dissertation On Environmental Law in IndiaDocument8 pagesDissertation On Environmental Law in IndiaWriteMyPaperInApaFormatSingapore100% (1)

- Background and Origin of The Christian, The - Dikran Y. Hadidian PDFDocument11 pagesBackground and Origin of The Christian, The - Dikran Y. Hadidian PDFMonachus IgnotusNo ratings yet