You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- 2010-12 600 800 Rush Switchback RMK Service Manual PDFDocument430 pages2010-12 600 800 Rush Switchback RMK Service Manual PDFBrianCook73% (11)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Cambridge International As A Level Accounting Coursebook With Digital Access (2 Years) (Hopkins, David, Malpas, Deborah, Randall Etc.) (Z-Library)Document880 pagesCambridge International As A Level Accounting Coursebook With Digital Access (2 Years) (Hopkins, David, Malpas, Deborah, Randall Etc.) (Z-Library)capsfast100% (3)

- Lecture 24Document8 pagesLecture 24gewaray536No ratings yet

- 25 Through 35, Columns L Through AD To Make Sure That The Changes in Breeding Herd Numbers Matches The Planned Response ForDocument11 pages25 Through 35, Columns L Through AD To Make Sure That The Changes in Breeding Herd Numbers Matches The Planned Response ForcapsfastNo ratings yet

- Feed Value Estimator: Enter Information On A "AS-FED" BasisDocument2 pagesFeed Value Estimator: Enter Information On A "AS-FED" BasiscapsfastNo ratings yet

- Pregnancy Hard Count: # Calvings Needed / Month 10Document1 pagePregnancy Hard Count: # Calvings Needed / Month 10capsfastNo ratings yet

- Labour Calculation Worksheet: Hours With LivestockDocument3 pagesLabour Calculation Worksheet: Hours With LivestockcapsfastNo ratings yet

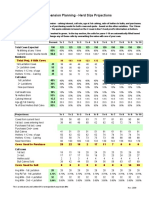

- Herd Expansion Planning - Herd Size ProjectionsDocument2 pagesHerd Expansion Planning - Herd Size ProjectionscapsfastNo ratings yet

- Dairy Cash Flow Ver7-14-11Document11 pagesDairy Cash Flow Ver7-14-11capsfastNo ratings yet

- PSU Ext - Growth ChartDocument10 pagesPSU Ext - Growth ChartcapsfastNo ratings yet

- Evaluation of Reproduction MeasuresDocument7 pagesEvaluation of Reproduction MeasurescapsfastNo ratings yet

- Transition Cow Pen Size CalculatorDocument1 pageTransition Cow Pen Size CalculatorcapsfastNo ratings yet

- Contract Milking - TemplateDocument10 pagesContract Milking - TemplatecapsfastNo ratings yet

- 10 - Calf RearingDocument14 pages10 - Calf RearingcapsfastNo ratings yet

- Compare Nutrient CostsDocument9 pagesCompare Nutrient CostscapsfastNo ratings yet

- 2011 DAIRY COW - 18000 LB Production - Corn Silage / Barley Silage RationDocument2 pages2011 DAIRY COW - 18000 LB Production - Corn Silage / Barley Silage RationcapsfastNo ratings yet

- Dairy - Feed BudgetDocument17 pagesDairy - Feed BudgetcapsfastNo ratings yet

- Cow Calf CalendarDocument5 pagesCow Calf CalendarcapsfastNo ratings yet

- Return On Assets and Return On EquityDocument2 pagesReturn On Assets and Return On EquitycapsfastNo ratings yet

- Good Health Records Setup Guide: For Dairy Comp 305® UsersDocument26 pagesGood Health Records Setup Guide: For Dairy Comp 305® UserscapsfastNo ratings yet

- 6 - Balance RationDocument14 pages6 - Balance RationcapsfastNo ratings yet

- Animal Health ChecklistDocument4 pagesAnimal Health ChecklistcapsfastNo ratings yet

- Chart of Accounts: Milk Production RevenueDocument5 pagesChart of Accounts: Milk Production RevenuecapsfastNo ratings yet

- UM0384Document35 pagesUM0384Pat 14HS1No ratings yet

- Numpy For Matlab UserDocument17 pagesNumpy For Matlab Userreza khNo ratings yet

- 24/10/2017. ",, IssnDocument2 pages24/10/2017. ",, IssnMikhailNo ratings yet

- Principles of Communication Systems LAB: Lab Manual (EE-230-F) Iv Sem Electrical and Electronics EngineeringDocument87 pagesPrinciples of Communication Systems LAB: Lab Manual (EE-230-F) Iv Sem Electrical and Electronics Engineeringsachin malikNo ratings yet

- Rec Peak EnergyDocument2 pagesRec Peak EnergyKNo ratings yet

- IptablesDocument3 pagesIptablessoomalikNo ratings yet

- Source of HeatDocument9 pagesSource of HeatSreekumar RajendrababuNo ratings yet

- CAPPC Presentation 12-5-05Document46 pagesCAPPC Presentation 12-5-05rahulNo ratings yet

- Test Data Management SoftwareDocument12 pagesTest Data Management SoftwareNNiveditaNo ratings yet

- Week 8-Wind Energy Generation - ELEC2300Document29 pagesWeek 8-Wind Energy Generation - ELEC2300Look AxxNo ratings yet

- Wordpress The Right WayDocument62 pagesWordpress The Right WayAdela CCNo ratings yet

- DYA Series 2018Document22 pagesDYA Series 2018Abo MohammedNo ratings yet

- Lecture 4 Design of Shallow FoundationDocument43 pagesLecture 4 Design of Shallow FoundationNadia Alentajan Abduka IINo ratings yet

- Difference Between CURE Clustering and DBSCAN Clustering - GeeksforGeeksDocument3 pagesDifference Between CURE Clustering and DBSCAN Clustering - GeeksforGeeksRavindra Kumar PrajapatiNo ratings yet

- IF184952 Digital Image ProcessingDocument3 pagesIF184952 Digital Image Processingshela malaNo ratings yet

- Re - Rockspace.local - Ap - SetupDocument6 pagesRe - Rockspace.local - Ap - SetuptrujillobresslerNo ratings yet

- Parametric Modeling A Simple ToolDocument6 pagesParametric Modeling A Simple ToolFatimeh ShahinNo ratings yet

- What Is Excel Swiss Knife - Excel Swiss KnifeDocument1 pageWhat Is Excel Swiss Knife - Excel Swiss KnifevaskoreNo ratings yet

- 2.motor Starters - Enclosed VersionsDocument106 pages2.motor Starters - Enclosed VersionsRAmesh SrinivasanNo ratings yet

- Ch23 Review ProblemsDocument25 pagesCh23 Review ProblemsحمدةالنهديةNo ratings yet

- Optimization of AirfoilsDocument9 pagesOptimization of AirfoilsMD SHAHRIARMAHMUDNo ratings yet

- 04 Spec Sheet PWM Controller ChipDocument16 pages04 Spec Sheet PWM Controller Chipxuanhiendk2No ratings yet

- D2 PPT 1 - AbdulDocument25 pagesD2 PPT 1 - AbdulAshish ShuklaNo ratings yet

- Revision Sheet Chapter 19Document58 pagesRevision Sheet Chapter 19annaninaibNo ratings yet

- Catálogo Greenleaf PDFDocument52 pagesCatálogo Greenleaf PDFAnonymous TqRycNChNo ratings yet

- RBK-PROC-MK3 Raychem MK3Document83 pagesRBK-PROC-MK3 Raychem MK3VictorNo ratings yet

- Physics Midterm Review PacketDocument6 pagesPhysics Midterm Review PacketJasper SendraNo ratings yet

- NSSCO Chemistry SyllabusDocument52 pagesNSSCO Chemistry SyllabusEbic GamerNo ratings yet