You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Manager'S Check Is As Good As The Money It Represents PNB vs. Amelio TriaDocument3 pagesManager'S Check Is As Good As The Money It Represents PNB vs. Amelio TriaThrift TravelsNo ratings yet

- Equitable Vs SSPDocument2 pagesEquitable Vs SSPThrift TravelsNo ratings yet

- New Pacific Timber & Supply Company vs. SenerisDocument2 pagesNew Pacific Timber & Supply Company vs. SenerisThrift TravelsNo ratings yet

- BPI Vs CADocument2 pagesBPI Vs CAThrift TravelsNo ratings yet

- Philippine Bank of Commerce vs. CADocument3 pagesPhilippine Bank of Commerce vs. CAThrift TravelsNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Ncert Solutions For Class 11 Accountancy Chapter 5 Bank Reconciliation StatementDocument24 pagesNcert Solutions For Class 11 Accountancy Chapter 5 Bank Reconciliation StatementLivin Verghese LijuNo ratings yet

- Module 10 (Abhishek)Document12 pagesModule 10 (Abhishek)abhishek gautamNo ratings yet

- Session 7 - SORDocument18 pagesSession 7 - SORNilisha DeshbhratarNo ratings yet

- Teller: Click To Edit Master Text Styles Second Level Third LevelDocument52 pagesTeller: Click To Edit Master Text Styles Second Level Third LevelhuongdtNo ratings yet

- Cooperative BankDocument70 pagesCooperative BankMonil MittalNo ratings yet

- MarksonDocument2 pagesMarksonyaregalNo ratings yet

- B-Inggris YesDocument3 pagesB-Inggris YesdadansuryawanNo ratings yet

- Compiled Loan DigestsDocument12 pagesCompiled Loan Digestscharmaine magsinoNo ratings yet

- Fundamentals of AccountancyDocument3 pagesFundamentals of AccountancySheena RobiniolNo ratings yet

- BPI Deposit Account RatesDocument5 pagesBPI Deposit Account Ratesparekoy1014No ratings yet

- FABM 2 2nd Quarter (Week 1) Students Copy 2Document45 pagesFABM 2 2nd Quarter (Week 1) Students Copy 2tjhunter077No ratings yet

- RBI Master Circular On Customer Service in BanksDocument105 pagesRBI Master Circular On Customer Service in BanksParveen KumarNo ratings yet

- Bank of The Philippine Islands v. Court of Appeals, 326 SCRA 641 (2000)Document2 pagesBank of The Philippine Islands v. Court of Appeals, 326 SCRA 641 (2000)CMESDMNo ratings yet

- AbejuelaDocument2 pagesAbejuelaGrise SakulNo ratings yet

- Sample - GuardianshipDocument6 pagesSample - GuardianshipJan Lorenzo100% (1)

- IDM-DT GroupAssignment 1 D H IDocument46 pagesIDM-DT GroupAssignment 1 D H IIshikaNo ratings yet

- Banking Cases 2nd SetDocument40 pagesBanking Cases 2nd SetDiane Dee YaneeNo ratings yet

- BANK Documents and ReconciliationDocument47 pagesBANK Documents and ReconciliationGlenn Altar100% (1)

- FA1 HandoutDocument104 pagesFA1 HandoutDevansh nayakNo ratings yet

- Introduction of Banking InstrumentsDocument15 pagesIntroduction of Banking InstrumentstriratnacomNo ratings yet

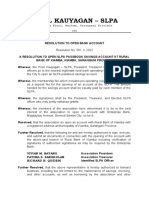

- Resolution To Open Bank Account 1Document3 pagesResolution To Open Bank Account 1Hanz HernandezNo ratings yet

- Terms & Conditions For 811 Account OpeningDocument8 pagesTerms & Conditions For 811 Account OpeningMr. UNKNOWN manNo ratings yet

- Midxx New and Other Products Sbkri Sbpen and SBSDF FormsDocument2 pagesMidxx New and Other Products Sbkri Sbpen and SBSDF Formsankitshinde1No ratings yet

- Banking Cases 2nd SetDocument40 pagesBanking Cases 2nd SetyaneedeeNo ratings yet

- Banking Cases Week 1Document5 pagesBanking Cases Week 1Katrina PerezNo ratings yet

- Multiple Bank Accounts Registration FormDocument2 pagesMultiple Bank Accounts Registration FormgoutamNo ratings yet

- SBOrder 092018Document301 pagesSBOrder 092018Amy SawNo ratings yet

- Paglaum ItDocument4 pagesPaglaum ItIvan BendiolaNo ratings yet

- Bpi V CA 232 Scra302Document11 pagesBpi V CA 232 Scra302frank japosNo ratings yet

- Creating Memo Pad in Finacle, Memo Pad Part - 2 - Finacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersDocument3 pagesCreating Memo Pad in Finacle, Memo Pad Part - 2 - Finacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersShubham PathakNo ratings yet