You might also like

- JIM PassportDocument2 pagesJIM PassportJimNo ratings yet

- ObjectionDocument10 pagesObjectionMy-Acts Of-SeditionNo ratings yet

- Vat-Value Added Tax (Uae) : Naeem IqbalDocument64 pagesVat-Value Added Tax (Uae) : Naeem IqbalAlex ko100% (1)

- 3306B Industrial Engine-Maintenance Intervals PDFDocument36 pages3306B Industrial Engine-Maintenance Intervals PDFanon_485665212100% (1)

- Powerpoint-09.14.22-Smmc Vat Zero Rating PDFDocument92 pagesPowerpoint-09.14.22-Smmc Vat Zero Rating PDFGirlie BacaocoNo ratings yet

- Uae Vat PresentationDocument64 pagesUae Vat PresentationAhammed MuzammilNo ratings yet

- Office of Alumni Relations (SMU) Annual ReportDocument56 pagesOffice of Alumni Relations (SMU) Annual ReportTheingiZawNo ratings yet

- Input Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTDocument28 pagesInput Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTAjey MendiolaNo ratings yet

- Chapter 9 Input VatDocument10 pagesChapter 9 Input VatHazel Jane EsclamadaNo ratings yet

- Value Added TaxDocument9 pagesValue Added TaxĴõ ĔĺNo ratings yet

- Coca Cola Flow Chart 1Document2 pagesCoca Cola Flow Chart 1ScribdTranslationsNo ratings yet

- Kim Han 2012 Seoul PDFDocument13 pagesKim Han 2012 Seoul PDFBoin ChoiNo ratings yet

- Principles OF Sterile Technique: Prepared By: Mrs. R. M. Dimalibot RM, RN ManDocument36 pagesPrinciples OF Sterile Technique: Prepared By: Mrs. R. M. Dimalibot RM, RN ManCerisse RemoNo ratings yet

- Return For Remittance of Value Added TaxDocument2 pagesReturn For Remittance of Value Added TaxTendai ZamangweNo ratings yet

- ITX 240.01.B - VAT Monthly ReturnDocument2 pagesITX 240.01.B - VAT Monthly ReturnFredben BenardNo ratings yet

- Return For Remittance of Value Added TaxDocument2 pagesReturn For Remittance of Value Added TaxDSM DRIVING SCHOOLNo ratings yet

- VAT FormDocument2 pagesVAT FormGbenga Ogunsakin67% (3)

- Value Added TaxDocument17 pagesValue Added TaxkirigofortunateNo ratings yet

- 1 Basics of Value Added TaxDocument58 pages1 Basics of Value Added TaxHazel Andrea Garduque LopezNo ratings yet

- Bustax Chapter 9Document10 pagesBustax Chapter 9Pineda, Paula MarieNo ratings yet

- MIDTERMS Business and Transfer TaxationDocument13 pagesMIDTERMS Business and Transfer Taxationabrylle opinianoNo ratings yet

- FGFERWWYEDVSDFGAWERFGDocument2 pagesFGFERWWYEDVSDFGAWERFGMD. ANWAR UL HAQUENo ratings yet

- Vat Zero Rated SuppliesDocument2 pagesVat Zero Rated SuppliesPrecy B BinwagNo ratings yet

- VAT Powerpoint - 2022 - Tax2ABDocument47 pagesVAT Powerpoint - 2022 - Tax2ABNande JongaNo ratings yet

- Powerpoint-03 19 22Document126 pagesPowerpoint-03 19 22CrizziaNo ratings yet

- Chapter 9 Part 1 Input VatDocument25 pagesChapter 9 Part 1 Input VatChristian PelimcoNo ratings yet

- VAT of BangladeshDocument111 pagesVAT of BangladeshNahian HasanNo ratings yet

- VAT Powerpoint - 2023 - Tax2ABDocument43 pagesVAT Powerpoint - 2023 - Tax2ABPitso VingerNo ratings yet

- C9 Input VATDocument18 pagesC9 Input VATdraga pinasNo ratings yet

- VAT Guide 2023Document46 pagesVAT Guide 2023ELIJAHNo ratings yet

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- VAT Guide 2021Document56 pagesVAT Guide 2021C ChamaNo ratings yet

- 1 Understanding VAT For BusinessesDocument6 pages1 Understanding VAT For BusinessesBensonNo ratings yet

- Value Added Tax (Cap 476)Document15 pagesValue Added Tax (Cap 476)Triila manillaNo ratings yet

- VAT GuideZRADocument56 pagesVAT GuideZRADaniel Glen-WilliamsonNo ratings yet

- Vat+ +New+Requirements+for+Tax+InvoicesDocument3 pagesVat+ +New+Requirements+for+Tax+InvoicesCj Brits Finansiële DiensteNo ratings yet

- Value Added Tax-PDocument20 pagesValue Added Tax-PMa. Corazon CaramalesNo ratings yet

- Lecture Slides - Lecture 01 - VAT (Part 1)Document6 pagesLecture Slides - Lecture 01 - VAT (Part 1)nkosinathiNo ratings yet

- Final PaperDocument20 pagesFinal PaperLaila PaleyanNo ratings yet

- LU1 - Value-Added TaxDocument24 pagesLU1 - Value-Added Taxmandisanomzamo72No ratings yet

- Unit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Document23 pagesUnit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Bizu AtnafuNo ratings yet

- A. C. D. With:: If of Is If If of If IsDocument3 pagesA. C. D. With:: If of Is If If of If IsFerl Diane SiñoNo ratings yet

- TAXATION 2 Chapter 13 Input VATDocument2 pagesTAXATION 2 Chapter 13 Input VATKim Cristian MaañoNo ratings yet

- Tax.3213-7 Output Input and Vat PayableDocument11 pagesTax.3213-7 Output Input and Vat PayableMira Louise HernandezNo ratings yet

- Input VAT ch9 IncompleteDocument3 pagesInput VAT ch9 IncompleteMarionne GNo ratings yet

- 8VATDocument70 pages8VATNoelNo ratings yet

- ICAEW Principles of Taxation CH 11-13Document30 pagesICAEW Principles of Taxation CH 11-13ITALIANO hohNo ratings yet

- WTS Dhruva VAT Handbook PDFDocument40 pagesWTS Dhruva VAT Handbook PDFFaraz AkhtarNo ratings yet

- Value-Added TaxDocument33 pagesValue-Added TaxvicsNo ratings yet

- Document1BackgroundDocument3 pagesDocument1BackgroundCj Brits Finansiële DiensteNo ratings yet

- Value Added TaxDocument8 pagesValue Added TaxDaniel MweuNo ratings yet

- TAX 221-AVP (Atillo, Cañete, Dejan, Manlimos, Hortellano)Document50 pagesTAX 221-AVP (Atillo, Cañete, Dejan, Manlimos, Hortellano)reymardicoNo ratings yet

- Distinguish Nature of VATDocument2 pagesDistinguish Nature of VATMark Dela CruzNo ratings yet

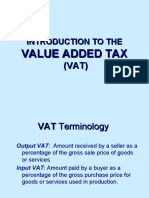

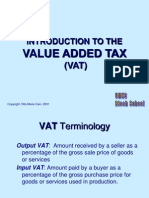

- Introduction To TheDocument11 pagesIntroduction To The9211420420No ratings yet

- Withholding Tax and Value Added TaxDocument11 pagesWithholding Tax and Value Added Taxadewumi mayowaNo ratings yet

- Basic Features of Value Added Tax (VAT) For ItesDocument24 pagesBasic Features of Value Added Tax (VAT) For ItesDebashishDolonNo ratings yet

- VATDocument11 pagesVATSaurav KumarNo ratings yet

- Main Features of VATDocument3 pagesMain Features of VATSiva Subramanian100% (2)

- Introduction To Value Added TaxDocument5 pagesIntroduction To Value Added TaxNYSHAN JOFIELYN TABBAYNo ratings yet

- Chapter 9 Input VatDocument2 pagesChapter 9 Input Vatnewlymade641No ratings yet

- Tax Base For VAT: Import StageDocument2 pagesTax Base For VAT: Import StageS. M. Saz Lul HoqueNo ratings yet

- Chapter 20 - VATDocument14 pagesChapter 20 - VATrottelosNo ratings yet

- VAT Slides Lecture 1Document34 pagesVAT Slides Lecture 1Londiwe GebedaNo ratings yet

- VAT ReturnsDocument39 pagesVAT ReturnsTaha AhmedNo ratings yet

- Value Added Tax Returns Form 002Document5 pagesValue Added Tax Returns Form 002JUDY OSUSUNo ratings yet

- Accounting For Indirect TaxesDocument40 pagesAccounting For Indirect TaxesSabaa if100% (1)

- Chapter 01Document41 pagesChapter 01amieyrahimahNo ratings yet

- SDFGDocument2 pagesSDFGKirba K.No ratings yet

- Cybenetics - Evaluation - Report - COMPARISON - VTE Bronze 600WDocument16 pagesCybenetics - Evaluation - Report - COMPARISON - VTE Bronze 600WRenan ZaninettiNo ratings yet

- INS200Document4 pagesINS200Miszz Bella Natallya'zNo ratings yet

- Revised Plans For Restoration Hardware Guesthouse (Mar. 7, 2017)Document79 pagesRevised Plans For Restoration Hardware Guesthouse (Mar. 7, 2017)crainsnewyork100% (1)

- Group 9 - High Rise StructuresDocument14 pagesGroup 9 - High Rise StructuresAarohi Sharma100% (1)

- Jva Z14 ManaulDocument48 pagesJva Z14 ManaulRaju.KonduruNo ratings yet

- Classification of Highway CurvesDocument8 pagesClassification of Highway CurvesMarc AlamoNo ratings yet

- Robusta Coffee Allowances and DiscountsDocument2 pagesRobusta Coffee Allowances and DiscountsCamiNo ratings yet

- Cobol (Common Business Oriented Language)Document56 pagesCobol (Common Business Oriented Language)Pradeep KumarNo ratings yet

- Best Forex Trading Robot EA User Manual 20190826 - MT4Document16 pagesBest Forex Trading Robot EA User Manual 20190826 - MT4Adegoke EmmanuelNo ratings yet

- Advanced 640 X 600 Pixel, Backside Illuminated Global Shutter, Ultra Compact Sensor, With High QE, High MTF, Excellent PLS, and Full-FeaturesDocument3 pagesAdvanced 640 X 600 Pixel, Backside Illuminated Global Shutter, Ultra Compact Sensor, With High QE, High MTF, Excellent PLS, and Full-FeaturesbananNo ratings yet

- IT - 601 Unit 5.doxDocument60 pagesIT - 601 Unit 5.doxAyush KumarNo ratings yet

- Cyber Security Policy NotesDocument2 pagesCyber Security Policy NotesRaúl Cálcamo AlonzoNo ratings yet

- SB2X 22 06Document7 pagesSB2X 22 06Michael BuntonNo ratings yet

- E-Commerce Product Quick View - OdooDocument5 pagesE-Commerce Product Quick View - OdooKeluarga GadjahNo ratings yet

- Candida AurisDocument5 pagesCandida Aurisarunkumar76No ratings yet

- Beams 12ge LN01Document41 pagesBeams 12ge LN01Setia Nurul MNo ratings yet

- Example ResumeDocument1 pageExample ResumeDanny PeckNo ratings yet

- CAT22C10: 256-Bit Nonvolatile CMOS Static RAMDocument10 pagesCAT22C10: 256-Bit Nonvolatile CMOS Static RAMvanmarteNo ratings yet

- DPWH Volume II - Intrastructure Main GuidelinesDocument154 pagesDPWH Volume II - Intrastructure Main GuidelinesJuliaMeeNo ratings yet

- Letter From ACLU of Illinois To Springfield City Council On PanhandlingDocument3 pagesLetter From ACLU of Illinois To Springfield City Council On PanhandlingDean OlsenNo ratings yet

- Pair Task Activity #03-00-05 555 LED Flasher: ComponentsDocument3 pagesPair Task Activity #03-00-05 555 LED Flasher: ComponentsRissy Kh XhieNo ratings yet