You might also like

- Assignment ThuDocument14 pagesAssignment ThuVu Thi ThuNo ratings yet

- Master FileDocument14 pagesMaster FileKAVVIKANo ratings yet

- Ventas Inmobiliarias de Goodyear2Document36 pagesVentas Inmobiliarias de Goodyear2Ayrton AjuNo ratings yet

- Service Operations Management Lecture IIDocument9 pagesService Operations Management Lecture IISiddharthaChowdaryNo ratings yet

- Copie de ExosInClassDocument4 pagesCopie de ExosInClassArbi AhmetajNo ratings yet

- Midsem SolutionDocument4 pagesMidsem SolutionEklavyaNo ratings yet

- Binomial Option Pricing: Parameters Results Binomial BS Analytical Call PutDocument4 pagesBinomial Option Pricing: Parameters Results Binomial BS Analytical Call PutSundeep KumarNo ratings yet

- Options Greeks CalculatorDocument6 pagesOptions Greeks CalculatorpraschNo ratings yet

- Problem 1 YTM CalculationDocument2 pagesProblem 1 YTM CalculationArbi AhmetajNo ratings yet

- Options Greeks CalculatorDocument6 pagesOptions Greeks CalculatoranbuNo ratings yet

- Homework 3Document33 pagesHomework 3indiraNo ratings yet

- Multiple Logistic Regression Model-LPDocument7 pagesMultiple Logistic Regression Model-LPmanjushreeNo ratings yet

- Cve 307 Practical Data - 034102Document2 pagesCve 307 Practical Data - 034102Samuel Oluwaseun OlatunjiNo ratings yet

- Fibo Nacchi and Gaann Degree CalculationDocument2 pagesFibo Nacchi and Gaann Degree CalculationVijay ShahNo ratings yet

- Option Valuation: Numerical ExampleDocument15 pagesOption Valuation: Numerical ExampleMarwa HassanNo ratings yet

- GABP Posiciones de Opciones ResueltaDocument53 pagesGABP Posiciones de Opciones ResueltaHajjiNo ratings yet

- Big Data ScienceassigmentDocument10 pagesBig Data Scienceassigmentgerrydenis20No ratings yet

- Essay Test MASDocument18 pagesEssay Test MASNguyen Cam Tu (K15 HL)No ratings yet

- Temp Diff EUDocument3 pagesTemp Diff EUSreeraja SreevilasanNo ratings yet

- Housing Prices Observation Price ($000) Square Feet Price ($000) Error Bedrooms Bathrooms Actual Forecasted (Residual)Document31 pagesHousing Prices Observation Price ($000) Square Feet Price ($000) Error Bedrooms Bathrooms Actual Forecasted (Residual)jodi setya pratamaNo ratings yet

- Assignment # 6 Solution: MS MS y T y T N NDocument6 pagesAssignment # 6 Solution: MS MS y T y T N Nsulaiman_GNo ratings yet

- Sample Question 1: TimestampDocument9 pagesSample Question 1: Timestampsaurabh kumarNo ratings yet

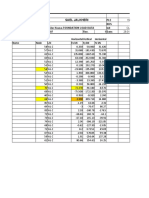

- Payslip LUBATON JOHN CYRIEL BICOYDocument1 pagePayslip LUBATON JOHN CYRIEL BICOYJohn Cyriel LubatonNo ratings yet

- FI6051 Dynamic Delta Gamma Hedging Example HullTable14!2!3Document4 pagesFI6051 Dynamic Delta Gamma Hedging Example HullTable14!2!3fmurphyNo ratings yet

- Assignment 4Document5 pagesAssignment 4carmen priscoNo ratings yet

- Calcium SilicateDocument1 pageCalcium Silicatemohd asrofi muslimNo ratings yet

- Survey Lab ReportDocument8 pagesSurvey Lab ReportJames Michael ChuNo ratings yet

- L2 ExamplesDocument5 pagesL2 ExamplesKruti BhattNo ratings yet

- Sensitivity Analysis Computer SolutionDocument10 pagesSensitivity Analysis Computer SolutionMikee N.J BuhisanNo ratings yet

- Stock Analysis of Power Finance CorporationDocument5 pagesStock Analysis of Power Finance CorporationDeepak YadavNo ratings yet

- Strike, K Volatity, σ Rf rate Per/Year Div yield, q # OptionsDocument8 pagesStrike, K Volatity, σ Rf rate Per/Year Div yield, q # OptionsSAGUN AGARWALNo ratings yet

- Level Sheet Distance and Elevation DataDocument2 pagesLevel Sheet Distance and Elevation DataRajitha RajapaksheNo ratings yet

- LPP Sensitivity ReportDocument7 pagesLPP Sensitivity ReportVenkatesh mNo ratings yet

- QTBDocument7 pagesQTBUmarNo ratings yet

- TIS/JIS STANDARDS FOR ANGLESDocument2 pagesTIS/JIS STANDARDS FOR ANGLESMURTY69No ratings yet

- Soal & Jawab STATISTIKDocument2 pagesSoal & Jawab STATISTIKIskandar ZulkarnainNo ratings yet

- Sensitivity Problem Solved and Assignment 2Document10 pagesSensitivity Problem Solved and Assignment 2afridaNo ratings yet

- Nama: Adi Nara Acchedya NIM: 041814353042 Magister Manajemen Angkatan 51 - Kelas SoreDocument4 pagesNama: Adi Nara Acchedya NIM: 041814353042 Magister Manajemen Angkatan 51 - Kelas SoreMonica WahyuningasriNo ratings yet

- OUTPUTDocument12 pagesOUTPUTmedictedNo ratings yet

- MyfileDocument2 pagesMyfileoliviawang011231No ratings yet

- Statistics Meeting 10Document3 pagesStatistics Meeting 10Muhammad Ali AkbarNo ratings yet

- Fin 647Document3 pagesFin 647Md. Junayed Hasan 2225417660No ratings yet

- 25m RCC T-Beam Bridge Bending Moment AnalysisDocument2 pages25m RCC T-Beam Bridge Bending Moment AnalysisSuman NakarmiNo ratings yet

- FI6051 Dynamic Delta Hedging Example HullTable14!2!3Document4 pagesFI6051 Dynamic Delta Hedging Example HullTable14!2!3fmurphyNo ratings yet

- Tank DimDocument5 pagesTank Dimiqramoyale022No ratings yet

- Project Job Number EngineerDocument1 pageProject Job Number EngineerjenniferNo ratings yet

- Berat Testis: DescriptivesDocument6 pagesBerat Testis: DescriptivesAmalia Rizqi RNo ratings yet

- Expt 4 HysterisisDocument13 pagesExpt 4 HysterisisKowsona ChakrabortyNo ratings yet

- A4 - REV Simple Design & MagnelDocument35 pagesA4 - REV Simple Design & MagnelVicky Faras Barunson PanggabeanNo ratings yet

- Gradation of SDBC GR 2: Weight of The Sample in GM Location CHDocument1 pageGradation of SDBC GR 2: Weight of The Sample in GM Location CHBinayalal PatraNo ratings yet

- Final Temp NewDocument7 pagesFinal Temp NewTeja MullapudiNo ratings yet

- ACET108 Revision PDFDocument12 pagesACET108 Revision PDFabiNo ratings yet

- Practice Questions - RevisionDocument12 pagesPractice Questions - RevisionNorhafizah Khairol AnuarNo ratings yet

- 513301-Trial Condition (After INCL)Document2 pages513301-Trial Condition (After INCL)phankhoa83-1No ratings yet

- Boiler Support 6 AprilDocument25 pagesBoiler Support 6 AprilKumar AbhishekNo ratings yet

- DrainDocument6 pagesDrainjohnNo ratings yet

- ConcreteDocument4 pagesConcreteSyed Kashif PervezNo ratings yet

- TelemedicineDocument3 pagesTelemedicineSWAGATA RANA GIRINo ratings yet

- Manometer ADocument3 pagesManometer ABalai K2 JatengNo ratings yet

- Solutions Manual to accompany Introduction to Linear Regression AnalysisFrom EverandSolutions Manual to accompany Introduction to Linear Regression AnalysisRating: 1 out of 5 stars1/5 (1)

- Powerpoint Concept Smjhne Security-Analysis-and-Portfolo-Management-Unit-4-Dr-Asma-KhanDocument66 pagesPowerpoint Concept Smjhne Security-Analysis-and-Portfolo-Management-Unit-4-Dr-Asma-KhanShailjaNo ratings yet

- 8 Index Models and APTDocument63 pages8 Index Models and APTShazelNo ratings yet

- Discounted Cash Flow ValuationDocument41 pagesDiscounted Cash Flow ValuationJkn PalembangNo ratings yet

- TIME VALUE OF MONEY INVESTMENTSDocument83 pagesTIME VALUE OF MONEY INVESTMENTSMustakim Bin Aziz 1610534630No ratings yet

- Coaching Actuaries Exam IFM Suggested Study Schedule: Phase 1: LearnDocument7 pagesCoaching Actuaries Exam IFM Suggested Study Schedule: Phase 1: LearnAndrew SaundersNo ratings yet

- Formulas: F - Future Value P - Present/Principal ValueDocument2 pagesFormulas: F - Future Value P - Present/Principal ValueJimuel Ace SarmientoNo ratings yet

- Assignment 1 (Part A and Part B)Document8 pagesAssignment 1 (Part A and Part B)botakmbg6035No ratings yet

- 7.2 Valuation of Contingent ClaimsDocument27 pages7.2 Valuation of Contingent ClaimsPunit SharmaNo ratings yet

- P10-10 & P10-21 Managerial FinanceDocument5 pagesP10-10 & P10-21 Managerial Financevincent alvinNo ratings yet

- Black Scholes ModelDocument15 pagesBlack Scholes Modelparinita raviNo ratings yet

- Parallel Cartoons of Fractal Models of FinanceDocument14 pagesParallel Cartoons of Fractal Models of FinanceChieh Chih ChiangNo ratings yet

- Nedl ArchDocument147 pagesNedl ArchMichaelNo ratings yet

- Security Analysis and Portfolio ManagementDocument21 pagesSecurity Analysis and Portfolio ManagementShiva ShankarNo ratings yet

- Monthly Return DataDocument3 pagesMonthly Return DataSubrata Chanda UthpalNo ratings yet

- Market Microstructure in PracticeDocument7 pagesMarket Microstructure in PracticeRicardo Ramos BezerraNo ratings yet

- Fundamental Analysis Redux-3Document25 pagesFundamental Analysis Redux-3Mantu KumarNo ratings yet

- Variance and Volatility Swaps in Energy Markets: Research Is Supported by NSERCDocument11 pagesVariance and Volatility Swaps in Energy Markets: Research Is Supported by NSERCPetr GorlichNo ratings yet

- Capital Asset Pricing ModelDocument17 pagesCapital Asset Pricing ModelChrisna Joyce MisaNo ratings yet

- Black-Scholes Abandon ProjectDocument4 pagesBlack-Scholes Abandon Projectf1940003No ratings yet

- Week 6 - Widget Factory SolutionDocument3 pagesWeek 6 - Widget Factory Solutionspotify2018 gmNo ratings yet

- Portfolio Optimization Maximizing Returns and Reducing RiskDocument8 pagesPortfolio Optimization Maximizing Returns and Reducing Riskpramodkumar808751528270No ratings yet

- A Guide To VIX Futures and OptionsDocument33 pagesA Guide To VIX Futures and OptionsSteve Zhang100% (2)

- GBA5204 Homework 4Document4 pagesGBA5204 Homework 4Allen GasparNo ratings yet

- Return and Risk ExcercisesDocument2 pagesReturn and Risk ExcercisesBảoNgọcNo ratings yet

- Module 2 Special Topics in Financial ManagementDocument16 pagesModule 2 Special Topics in Financial Managementkimjoshuadiaz12No ratings yet

- Businessfinance12 q3 Mod6.1 Basic Long Term Financial Concepts Simple and Compound InterestDocument27 pagesBusinessfinance12 q3 Mod6.1 Basic Long Term Financial Concepts Simple and Compound InterestMarilyn Tamayo100% (2)

- C3 ValuationDocument26 pagesC3 ValuationMinh Lưu NhậtNo ratings yet

- Lectures 5 & 7 - Intermediate Exercises - Attempt ReviewDocument18 pagesLectures 5 & 7 - Intermediate Exercises - Attempt ReviewHeidi DaoNo ratings yet

- Update Jan 08Document29 pagesUpdate Jan 08api-27370939100% (3)

- 2 Compound Interest FormulasDocument47 pages2 Compound Interest FormulasRiswan Riswan100% (1)