You might also like

- Tokio Marine Life - IHealth Plus Brochure-2019Document44 pagesTokio Marine Life - IHealth Plus Brochure-2019kinosraj kumaranNo ratings yet

- SVKM'S Nmims Anil Surendra Modi School of Commerce Sybcom Sem Iii (2019-22) Subject Name: Direct Taxation No. of Hours: 2 Hours InstructionsDocument20 pagesSVKM'S Nmims Anil Surendra Modi School of Commerce Sybcom Sem Iii (2019-22) Subject Name: Direct Taxation No. of Hours: 2 Hours InstructionsMadhuram SharmaNo ratings yet

- Bonifacio Vs MoraDocument2 pagesBonifacio Vs MoraMan2x SalomonNo ratings yet

- Bonifacio Brothers v. Mora, 20 SCRA 261Document2 pagesBonifacio Brothers v. Mora, 20 SCRA 261Sopongco ColeenNo ratings yet

- NG v. Asian CrusadersDocument1 pageNG v. Asian CrusadersAngelicaNo ratings yet

- Private International Law Case Digests 2Document2 pagesPrivate International Law Case Digests 2Jewelle Ann Lou SantosNo ratings yet

- ANTONINA LAMPANOvDocument5 pagesANTONINA LAMPANOvYour Public ProfileNo ratings yet

- Supreme Court Overrules Congress' Power to Strip CitizenshipDocument34 pagesSupreme Court Overrules Congress' Power to Strip CitizenshipGelle BaligodNo ratings yet

- Finman General Assurance Corp Vs InocencioDocument2 pagesFinman General Assurance Corp Vs InocencioAldrin TangNo ratings yet

- Part DDocument13 pagesPart DJovel LayasanNo ratings yet

- SC declares unconstitutional 3-month cap for monetary claims of illegally dismissed OFWsDocument2 pagesSC declares unconstitutional 3-month cap for monetary claims of illegally dismissed OFWsthelawyer07No ratings yet

- Pantranco VS BaesaDocument2 pagesPantranco VS BaesaDan Anthony BarrigaNo ratings yet

- Sulpicio Lines V SisanteDocument1 pageSulpicio Lines V Sisanteerikha_aranetaNo ratings yet

- Shafer V JudgeDocument2 pagesShafer V JudgeKenneth BuriNo ratings yet

- DBP Vs DoyonDocument5 pagesDBP Vs DoyonMelody Lim DayagNo ratings yet

- (Mercantile Law) Bar AnswersDocument17 pages(Mercantile Law) Bar AnswersJoseph Tangga-an GiduquioNo ratings yet

- Florendo v. Philam Plans, Inc., 666 SCRA 18 (2012)Document3 pagesFlorendo v. Philam Plans, Inc., 666 SCRA 18 (2012)Florence RoseteNo ratings yet

- Sequito Versus LetrondoDocument1 pageSequito Versus LetrondoJug HeadNo ratings yet

- UCPB vs. MasaganaDocument2 pagesUCPB vs. MasaganaQuennie Mae ZalavarriaNo ratings yet

- Philippine Phoenix Surety Insurance Inc. Vs WoodworksDocument3 pagesPhilippine Phoenix Surety Insurance Inc. Vs WoodworksKadzNituraNo ratings yet

- The Insular Life vs. Khu, GR 195176, April 18, 2016Document2 pagesThe Insular Life vs. Khu, GR 195176, April 18, 2016mhickey babonNo ratings yet

- SPL Digest CasesDocument12 pagesSPL Digest CasesMikaelGo-OngNo ratings yet

- Insurance DigestsDocument4 pagesInsurance DigestsLesly BriesNo ratings yet

- 10 Genil Vs RiveraDocument9 pages10 Genil Vs RiveraLimberge Paul CorpuzNo ratings yet

- Philippine Rabbit Bus Lines V IacDocument1 pagePhilippine Rabbit Bus Lines V IacKate Bernadette MadayagNo ratings yet

- G.R. No. 174156 FIlcar Transport Vs Espinas Registered OwnerDocument13 pagesG.R. No. 174156 FIlcar Transport Vs Espinas Registered OwnerChatNo ratings yet

- GSIS Vs CorderoDocument2 pagesGSIS Vs CorderoMei SuyatNo ratings yet

- Forensic Medicine Notes on Identification, Deception Detection and Death DeterminationDocument8 pagesForensic Medicine Notes on Identification, Deception Detection and Death DeterminationLloyd Anthony Valoria100% (1)

- Digest - PleadingsDocument6 pagesDigest - PleadingsJei Essa AlmiasNo ratings yet

- Manila Bankers Life v. Aban, 702 SCRA 417 (2013)Document8 pagesManila Bankers Life v. Aban, 702 SCRA 417 (2013)KristineSherikaChyNo ratings yet

- Cta 00 CV 06533 D 2003may16 Ass PDFDocument15 pagesCta 00 CV 06533 D 2003may16 Ass PDFAgnes PajilanNo ratings yet

- City Ordinance No. 5-2013Document2 pagesCity Ordinance No. 5-2013Lc FernandezNo ratings yet

- Litton Wins Case Against I/AME Piercing Corporate VeilDocument6 pagesLitton Wins Case Against I/AME Piercing Corporate VeilJoovs JoovhoNo ratings yet

- Oriental Assurance Corporation vs. Court of AppealsDocument6 pagesOriental Assurance Corporation vs. Court of AppealsJaja Ordinario Quiachon-Abarca100% (1)

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument12 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityPatricia Ann RueloNo ratings yet

- Great Pacific Life-vs-CADocument2 pagesGreat Pacific Life-vs-CAmario navalezNo ratings yet

- Batangas Laguna Bus Company vs Court of Appeals civil liability caseDocument1 pageBatangas Laguna Bus Company vs Court of Appeals civil liability caseBantogen BabantogenNo ratings yet

- Full Text Evidence. Module 1 CasesDocument102 pagesFull Text Evidence. Module 1 CasesCarla CariagaNo ratings yet

- Presumption of Negligence Pestano vs. Sumayang FactsDocument2 pagesPresumption of Negligence Pestano vs. Sumayang FactsJayNo ratings yet

- CIR v. P&G Philippine tax credit deniedDocument2 pagesCIR v. P&G Philippine tax credit deniedNaomi QuimpoNo ratings yet

- 05-Fortune Insurance and Surety Co., Inc. vs. CA (244 SCRA 308) - EscraDocument12 pages05-Fortune Insurance and Surety Co., Inc. vs. CA (244 SCRA 308) - EscraJNo ratings yet

- Some Credit CaseDocument6 pagesSome Credit CaseNadine Tubalinal SandinoNo ratings yet

- 1 Spouses Cha Vs CA PDFDocument6 pages1 Spouses Cha Vs CA PDFClarissa Degamo0% (1)

- Filipina Migrant Worker's Death Ruled HomicideDocument9 pagesFilipina Migrant Worker's Death Ruled HomicideJenniferPizarrasCadiz-CarullaNo ratings yet

- Insurance Case Digests by LuigoDocument3 pagesInsurance Case Digests by LuigoLuigi JaroNo ratings yet

- Insurance Digest 1Document13 pagesInsurance Digest 1joenelNo ratings yet

- Remulla v. MaliksiDocument4 pagesRemulla v. MaliksiSar FifthNo ratings yet

- UE Vs UEEADocument10 pagesUE Vs UEEAMarjorie Joy Rumbaoa CastilloNo ratings yet

- Sabina Exconde Vs Delfin and Dante CapunoDocument24 pagesSabina Exconde Vs Delfin and Dante CapunoCarlo ColumnaNo ratings yet

- Case Digest Del Carmen v. BacoyDocument4 pagesCase Digest Del Carmen v. BacoymagenNo ratings yet

- Pagcor vs. Bir - December 10, 2014Document6 pagesPagcor vs. Bir - December 10, 2014Cyruss Xavier Maronilla NepomucenoNo ratings yet

- Ching vs Rodriguez property disputeDocument3 pagesChing vs Rodriguez property disputeKenny Robert'sNo ratings yet

- Del Carmen Vs BacoyDocument14 pagesDel Carmen Vs BacoyKiks JampasNo ratings yet

- Finman General Assurance Corp vs Court of AppealsDocument2 pagesFinman General Assurance Corp vs Court of AppealsjayNo ratings yet

- 3.G.R. No. 103092Document5 pages3.G.R. No. 103092Lord AumarNo ratings yet

- 12 CIR vs. Phoenix (GR No. L-19727, May 20, 1965)Document13 pages12 CIR vs. Phoenix (GR No. L-19727, May 20, 1965)Alfred GarciaNo ratings yet

- 20 El Oriente, Fabrica de Tabacos, Inc., vs. Posadas 56 Phil. 147, September 21, 1931Document7 pages20 El Oriente, Fabrica de Tabacos, Inc., vs. Posadas 56 Phil. 147, September 21, 1931joyeduardoNo ratings yet

- Insurance Claim RulingDocument6 pagesInsurance Claim RulingJessica Magsaysay CrisostomoNo ratings yet

- OH HEK HOW Naturalization Oath ValidityDocument1 pageOH HEK HOW Naturalization Oath ValidityJacquelyn AlegriaNo ratings yet

- New Life Enterprises vs. CA, G.R. No. 94071Document9 pagesNew Life Enterprises vs. CA, G.R. No. 94071Victoria EscobalNo ratings yet

- ACCFA vs Alpha InsuranceDocument2 pagesACCFA vs Alpha InsuranceSebastian GarciaNo ratings yet

- Bonifacio Vs MoraDocument3 pagesBonifacio Vs MoraClaudine Christine A. VicenteNo ratings yet

- Political Law and PIL As of 2.6.2024Document239 pagesPolitical Law and PIL As of 2.6.2024Jubelle AngeliNo ratings yet

- St. Louis V CaDocument2 pagesSt. Louis V CaJubelle AngeliNo ratings yet

- de La Rama vs. de La RamaDocument7 pagesde La Rama vs. de La RamaJubelle Angeli100% (1)

- Agency & Trust - YoshizakiDocument4 pagesAgency & Trust - YoshizakiJubelle AngeliNo ratings yet

- St. Louis V CaDocument2 pagesSt. Louis V CaJubelle AngeliNo ratings yet

- Far East V CA RedactedDocument3 pagesFar East V CA RedactedJubelle AngeliNo ratings yet

- Alfonso vs. NatividadDocument5 pagesAlfonso vs. NatividadJubelle AngeliNo ratings yet

- Del Rosario vs. Del RosarioDocument2 pagesDel Rosario vs. Del RosarioJubelle AngeliNo ratings yet

- Bernardo vs. Court of AppealsDocument6 pagesBernardo vs. Court of AppealsJubelle AngeliNo ratings yet

- Uriarte vs. Court of First Instance of Negros Occ - DigestDocument3 pagesUriarte vs. Court of First Instance of Negros Occ - DigestJubelle AngeliNo ratings yet

- Supreme Court Rules on Will Probate CaseDocument5 pagesSupreme Court Rules on Will Probate CaseJubelle AngeliNo ratings yet

- Cuizon vs. RamoleteDocument5 pagesCuizon vs. RamoleteJubelle AngeliNo ratings yet

- Ignacio Nabong For Appellants.: VOL. 52, MARCH 2, 1929 871Document3 pagesIgnacio Nabong For Appellants.: VOL. 52, MARCH 2, 1929 871Jubelle AngeliNo ratings yet

- Dolar vs. Roman Catholic Bishop of JaroDocument3 pagesDolar vs. Roman Catholic Bishop of JaroJubelle AngeliNo ratings yet

- Court clarifies meaning of "residesDocument12 pagesCourt clarifies meaning of "residesJubelle AngeliNo ratings yet

- Uriarte vs. Court of First Instance of Negros OccDocument3 pagesUriarte vs. Court of First Instance of Negros OccJubelle AngeliNo ratings yet

- in Re Kaw SingcoDocument4 pagesin Re Kaw SingcoJubelle AngeliNo ratings yet

- Salazar v. CFI of LagunaDocument6 pagesSalazar v. CFI of LagunaJubelle AngeliNo ratings yet

- Case 12 Calvo Full TextDocument4 pagesCase 12 Calvo Full TextJubelle AngeliNo ratings yet

- Cayetano vs. LeonidasDocument8 pagesCayetano vs. LeonidasJubelle AngeliNo ratings yet

- Calvo Ruled a Common Carrier in Case Involving Damaged ShipmentDocument2 pagesCalvo Ruled a Common Carrier in Case Involving Damaged ShipmentJubelle AngeliNo ratings yet

- Sarkies Tours Philippines, Inc. vs. Court of Appeals (10th DivisionDocument5 pagesSarkies Tours Philippines, Inc. vs. Court of Appeals (10th DivisionJubelle AngeliNo ratings yet

- Transportation Law – Common Carriage of GoodsDocument57 pagesTransportation Law – Common Carriage of GoodsJubelle Angeli100% (1)

- Carrier liability for sunken cargoDocument4 pagesCarrier liability for sunken cargoJubelle AngeliNo ratings yet

- Sarkies Tours V CA (Case Digest)Document1 pageSarkies Tours V CA (Case Digest)Jubelle AngeliNo ratings yet

- Shipping Company Liable for Cargo Loss Due to NegligenceDocument2 pagesShipping Company Liable for Cargo Loss Due to NegligenceJubelle AngeliNo ratings yet

- Reputable Forwarder's liability for hijacked goodsDocument4 pagesReputable Forwarder's liability for hijacked goodsJubelle AngeliNo ratings yet

- (A. Subject Matter) Guingon vs. Del Monte, 20 SCRA 1043, No. L-22042 August 17, 1967Document4 pages(A. Subject Matter) Guingon vs. Del Monte, 20 SCRA 1043, No. L-22042 August 17, 1967Alexiss Mace JuradoNo ratings yet

- Uy V PalomarDocument12 pagesUy V PalomarJubelle AngeliNo ratings yet

- Bike InsuranceDocument2 pagesBike Insurancetuv srinuvasaNo ratings yet

- MDThuDocument28 pagesMDThuPatrick LongNo ratings yet

- Er Patient With Balance Prior To AdmissionDocument2 pagesEr Patient With Balance Prior To Admissionmelvin terrazolaNo ratings yet

- Easy EssayDocument7 pagesEasy Essayb71g37ac100% (2)

- IC-27 Health Insurance: AcknowledgementDocument36 pagesIC-27 Health Insurance: AcknowledgementChampaka Prasad RanaNo ratings yet

- Marine InsuranceDocument3 pagesMarine InsuranceJithinNo ratings yet

- Westfall Technik Inc. 2021 Summary Annual Report 501Document2 pagesWestfall Technik Inc. 2021 Summary Annual Report 501Miguel FrancoNo ratings yet

- Name: Class: Semester: Roll No.: Enrollment No.: Subject:: Vartika Srivastava Mba (HR)Document13 pagesName: Class: Semester: Roll No.: Enrollment No.: Subject:: Vartika Srivastava Mba (HR)Ceegi Singh SrivastavaNo ratings yet

- Warranties Liabilities Patents Bids and InsuranceDocument39 pagesWarranties Liabilities Patents Bids and InsuranceIVAN JOHN BITONNo ratings yet

- Kilbirnie Tennis Club 2020 Annual Report highlights steady growthDocument20 pagesKilbirnie Tennis Club 2020 Annual Report highlights steady growthConory GulowNo ratings yet

- Company Nurse Endorsement 2022Document3 pagesCompany Nurse Endorsement 2022Jim Kimberly TilapNo ratings yet

- Wa0029.Document6 pagesWa0029.anusha.veldandiNo ratings yet

- September Week 3Document118 pagesSeptember Week 3Praful GhodeswarNo ratings yet

- Full Download Ebook PDF Health Economics Core Concepts and Essential Tools Gateway To Healthcare Management PDFDocument48 pagesFull Download Ebook PDF Health Economics Core Concepts and Essential Tools Gateway To Healthcare Management PDFmichael.nightingale883100% (36)

- Unofficial Guide To Boston For Babson Students and PartnersDocument101 pagesUnofficial Guide To Boston For Babson Students and PartnersBaldev RawatNo ratings yet

- Bajaj Two Wheeler Insurance PolicyDocument7 pagesBajaj Two Wheeler Insurance PolicyManjunath BNo ratings yet

- The Anmeldung - How To Register An Address in Berlin - All About BerlinDocument8 pagesThe Anmeldung - How To Register An Address in Berlin - All About BerlinsamizarNo ratings yet

- CHOOSING THE RIGHT TERM PLANDocument1 pageCHOOSING THE RIGHT TERM PLANKumardasNsNo ratings yet

- Chapter 2Document20 pagesChapter 2AbhiNo ratings yet

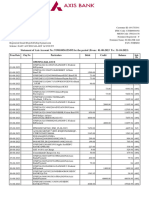

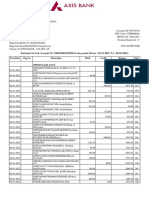

- Statement of Axis Account No:919010056153495 For The Period (From: 01-08-2023 To: 31-10-2023)Document5 pagesStatement of Axis Account No:919010056153495 For The Period (From: 01-08-2023 To: 31-10-2023)pooja.acharyaNo ratings yet

- QuotationDocument2 pagesQuotationMuhammad Syazwan MuskamNo ratings yet

- Star Health - Red CarpetDocument3 pagesStar Health - Red CarpetPradeep NadarNo ratings yet

- AC78 Chapter 3 Investment in Debt Securities Other Non Current Financial AssetsDocument78 pagesAC78 Chapter 3 Investment in Debt Securities Other Non Current Financial AssetsmerryNo ratings yet

- Internal Control QuestionaireDocument52 pagesInternal Control QuestionaireRiki HalimNo ratings yet

- Basic Examples and Calculations in Life InsuranceDocument42 pagesBasic Examples and Calculations in Life Insurancebranmondi8676No ratings yet

- 4.2. InsuranceDocument11 pages4.2. InsuranceThobo PeterNo ratings yet

- Acct Statement - XX4920 - 02022023Document4 pagesAcct Statement - XX4920 - 02022023Popi BhowmikNo ratings yet

- Medicare Appeals BacklogDocument13 pagesMedicare Appeals Backlogmamatha mamtaNo ratings yet