You might also like

- VATEUD Pilots ManualDocument32 pagesVATEUD Pilots ManualAndreas TzekasNo ratings yet

- General Education September 2016Document195 pagesGeneral Education September 2016Ronalyn AndaganNo ratings yet

- ICT Forex Trading NotesDocument110 pagesICT Forex Trading NotesLavier Trinta e Sete100% (4)

- DMC Bored Cast in Situ Pile ConcretingDocument38 pagesDMC Bored Cast in Situ Pile Concretingmaansi jakkidi100% (1)

- EY - NASSCOM - M&A Trends and Outlook - Technology Services VF - 0Document35 pagesEY - NASSCOM - M&A Trends and Outlook - Technology Services VF - 0Tejas JosephNo ratings yet

- Answers to Selected Problems in Multivariable Calculus with Linear Algebra and SeriesFrom EverandAnswers to Selected Problems in Multivariable Calculus with Linear Algebra and SeriesRating: 1.5 out of 5 stars1.5/5 (2)

- M 6 Problem Set SolutionsDocument8 pagesM 6 Problem Set SolutionsNiyati ShahNo ratings yet

- Immunization With FuturesDocument18 pagesImmunization With FuturesNiyati ShahNo ratings yet

- Personal Styling Service-Contract - No WatermarkDocument5 pagesPersonal Styling Service-Contract - No WatermarkLexine Emille100% (1)

- GitHub TrainingDocument21 pagesGitHub Trainingcyberfox786No ratings yet

- W2 II C12 Systematic Risk and Equity Risk PremiumDocument12 pagesW2 II C12 Systematic Risk and Equity Risk PremiumSophie LimNo ratings yet

- Tutorial 5 - SolutionDocument6 pagesTutorial 5 - SolutionNg Chun SenfNo ratings yet

- Assignment Risk and ReturnDocument3 pagesAssignment Risk and ReturnCheong Yu ShuangNo ratings yet

- Chapter 6 - Problem Solving (Risk)Document5 pagesChapter 6 - Problem Solving (Risk)Shresth KotishNo ratings yet

- 5250 Final 2019 PracticeDocument7 pages5250 Final 2019 Practice杜晓晚No ratings yet

- General Aptitude: Key: (C) SolDocument51 pagesGeneral Aptitude: Key: (C) SolAkash RoyNo ratings yet

- TA112.BQAF - .L Solution CMA January 2022 Examination PDFDocument8 pagesTA112.BQAF - .L Solution CMA January 2022 Examination PDFMohammed Javed UddinNo ratings yet

- Sensitivity Analyisis - Part 1Document8 pagesSensitivity Analyisis - Part 1RuanNo ratings yet

- Standard Deviation on Individual Security = σ = √σ: Risk Return Problems Problem 1Document3 pagesStandard Deviation on Individual Security = σ = √σ: Risk Return Problems Problem 1jakia yasminNo ratings yet

- Answers 3Document10 pagesAnswers 3akufarezahNo ratings yet

- Portfolio Management Handout 1 - AnswersDocument13 pagesPortfolio Management Handout 1 - AnswersPriyankaNo ratings yet

- 1.4.3 Regression Analysis SolutionsDocument10 pages1.4.3 Regression Analysis SolutionsmmcgrealjrNo ratings yet

- Adda247's Top Banking & SSC Exam Preparation AppDocument6 pagesAdda247's Top Banking & SSC Exam Preparation AppBhushan PawarNo ratings yet

- Financial Management - 2 Return and Risk: Beg EndDocument6 pagesFinancial Management - 2 Return and Risk: Beg EndYoseph WooNo ratings yet

- Risk and Return For PortfolioDocument5 pagesRisk and Return For PortfolioferuzbekNo ratings yet

- Analytical PS A01 A10 Solutions 2Document14 pagesAnalytical PS A01 A10 Solutions 2MarieNo ratings yet

- Solution Manual For Calculus Early Transcendentals 8Th Edition by Stewart Isbn 1285741552 9781285741550 Full Chapter PDFDocument36 pagesSolution Manual For Calculus Early Transcendentals 8Th Edition by Stewart Isbn 1285741552 9781285741550 Full Chapter PDFashleigh.berndt122100% (12)

- Percentage Class NotesDocument6 pagesPercentage Class NotesSid MalhotraNo ratings yet

- Applied Statistics in Business and Economics 4th Edition Doane Solutions Manual 1Document28 pagesApplied Statistics in Business and Economics 4th Edition Doane Solutions Manual 1michelle100% (34)

- Applied Statistics in Business and Economics 4Th Edition Doane Solutions Manual Full Chapter PDFDocument36 pagesApplied Statistics in Business and Economics 4Th Edition Doane Solutions Manual Full Chapter PDFtess.lechner250100% (15)

- Fa2 (A)Document5 pagesFa2 (A)kalowekamoNo ratings yet

- Practice Questions and SolutionsDocument7 pagesPractice Questions and SolutionsLiy TehNo ratings yet

- 02.SimplificationDocument2 pages02.SimplificationNeelam TiwariNo ratings yet

- VOL 1 CMA FINal ovedDocument12 pagesVOL 1 CMA FINal ovedrehaliya15No ratings yet

- CF T4Document19 pagesCF T4stellaNo ratings yet

- Homework Corporate FinanceDocument2 pagesHomework Corporate FinanceChester W.SiongNo ratings yet

- CIVL2330 - Assignment 1 SolutionsDocument5 pagesCIVL2330 - Assignment 1 Solutionsbrip selNo ratings yet

- Lesson 3 - Number System and ConversionDocument32 pagesLesson 3 - Number System and ConversionJomar DaclesNo ratings yet

- Risk Aversion and Capital AllocationDocument5 pagesRisk Aversion and Capital AllocationPrince ShovonNo ratings yet

- Convert From Decimal To BinaryDocument10 pagesConvert From Decimal To BinaryKEO PHEAKDEYNo ratings yet

- CBSE X Maths Case Study Practice Tests (3 Topics)Document7 pagesCBSE X Maths Case Study Practice Tests (3 Topics)Vishal MNo ratings yet

- PROBLEM SET-3 Discrete Probability - SolutionsDocument9 pagesPROBLEM SET-3 Discrete Probability - Solutionsmaxentiuss100% (5)

- Cfin 4 4th Edition Besley Solutions ManualDocument8 pagesCfin 4 4th Edition Besley Solutions Manualwadeperlid9d98k100% (28)

- P3.33 ReklaitisDocument32 pagesP3.33 ReklaitisMelyana ThoresiaNo ratings yet

- E) Investors Demand Higher Expected Rates of Return From Stocks With Returns That Are VeryDocument4 pagesE) Investors Demand Higher Expected Rates of Return From Stocks With Returns That Are Veryssunday giftNo ratings yet

- Math 2020 p1 Ms - Alt A: Q Content Mark SDocument7 pagesMath 2020 p1 Ms - Alt A: Q Content Mark S-NADWE-No ratings yet

- Queen's College Maths Exam SolutionsDocument8 pagesQueen's College Maths Exam SolutionsTO ChauNo ratings yet

- Chapter 7 Portfolio TheoryDocument41 pagesChapter 7 Portfolio TheoryRupesh DhindeNo ratings yet

- HW6 Solutions: Box-Cox Transformation Improves Residual PlotDocument4 pagesHW6 Solutions: Box-Cox Transformation Improves Residual PlotSouleymane CoulibalyNo ratings yet

- Dapan 6-0910 Hki-1Document2 pagesDapan 6-0910 Hki-1vuthoa20069463No ratings yet

- LSDDocument7 pagesLSDkasuwedaNo ratings yet

- First Course in The Finite Element Method Si Version 5Th Edition Logan Solutions Manual Full Chapter PDFDocument42 pagesFirst Course in The Finite Element Method Si Version 5Th Edition Logan Solutions Manual Full Chapter PDFJamesOrtegapfcs100% (9)

- Non Negative Assumption Solution by Graphical Method:: Linear ProgrammingDocument11 pagesNon Negative Assumption Solution by Graphical Method:: Linear ProgrammingSayantani SamantaNo ratings yet

- Exercise T4 Risk and ReturnDocument5 pagesExercise T4 Risk and ReturnAidil IdzhamNo ratings yet

- Calculating portfolio beta, variance, standard deviation and expected returnsDocument5 pagesCalculating portfolio beta, variance, standard deviation and expected returnsManuel BoahenNo ratings yet

- Exercises Chapt 3 SolutionsDocument6 pagesExercises Chapt 3 SolutionskilbanemNo ratings yet

- Bisection MethodDocument13 pagesBisection MethodFarizza Ann KiseoNo ratings yet

- PS1 Solution (8e)Document3 pagesPS1 Solution (8e)LUCKYTODAY IFEELNo ratings yet

- 435 - Problem Set 1 (Solution)Document9 pages435 - Problem Set 1 (Solution)Md Borhan Uddin 2035097660No ratings yet

- Unimathsity Vectors QuestionsDocument2 pagesUnimathsity Vectors Questionsapi-394057706No ratings yet

- Q 31-35Document6 pagesQ 31-35mahisacNo ratings yet

- Risk Return Demonstration Lecture QuestionsDocument6 pagesRisk Return Demonstration Lecture QuestionsTriet NguyenNo ratings yet

- FINM2003 - Mid Semester Exam Sem 1 2015 (Suggested Solutions)Document6 pagesFINM2003 - Mid Semester Exam Sem 1 2015 (Suggested Solutions)JasonNo ratings yet

- Class Problem-Portfolio Risk and ReturnDocument14 pagesClass Problem-Portfolio Risk and ReturnAzan ahmedNo ratings yet

- Multiple Choice Problems: 0 X, 1 1 X, 2 2 Y, 1 Y, 2Document7 pagesMultiple Choice Problems: 0 X, 1 1 X, 2 2 Y, 1 Y, 2roBinNo ratings yet

- Risk and Return A - SolutionsDocument3 pagesRisk and Return A - SolutionsmilotikyuNo ratings yet

- Be4z9 24a55Document7 pagesBe4z9 24a55samidan tubeNo ratings yet

- 01 TrabajoDocument18 pages01 TrabajoYuliza Carolina Capuñay SiesquenNo ratings yet

- TA112.BQA F.L Solution CMA May 2022 Examination PDFDocument6 pagesTA112.BQA F.L Solution CMA May 2022 Examination PDFMohammed Javed UddinNo ratings yet

- M 7 Problem Set SolutionsDocument9 pagesM 7 Problem Set SolutionsNiyati ShahNo ratings yet

- Portfolio Optimization Project 2 FIN 653 Professor Natalia Gershun Group Members: Reynold D'silva Hanxiang Tang Wen GuoDocument11 pagesPortfolio Optimization Project 2 FIN 653 Professor Natalia Gershun Group Members: Reynold D'silva Hanxiang Tang Wen GuoNiyati ShahNo ratings yet

- P 1: M S B P R C - D: A. IntroductionDocument34 pagesP 1: M S B P R C - D: A. IntroductionNiyati ShahNo ratings yet

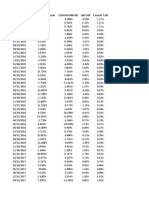

- Date Microsoft General Motors Delta Air Lines Walmart PfizerDocument11 pagesDate Microsoft General Motors Delta Air Lines Walmart PfizerNiyati ShahNo ratings yet

- M 5 Problem Set SolutionsDocument9 pagesM 5 Problem Set SolutionsNiyati ShahNo ratings yet

- Project 4 Tang, HanxiangDocument5 pagesProject 4 Tang, HanxiangNiyati ShahNo ratings yet

- Hedging With Interest Rate SwapsDocument16 pagesHedging With Interest Rate SwapsNiyati ShahNo ratings yet

- M 5 Problem Set SolutionsDocument9 pagesM 5 Problem Set SolutionsNiyati ShahNo ratings yet

- Review of The Lecture - Diversification and The Efficient FrontierDocument13 pagesReview of The Lecture - Diversification and The Efficient FrontierNiyati ShahNo ratings yet

- The Black Scholes FormulaDocument12 pagesThe Black Scholes FormulaNiyati ShahNo ratings yet

- Solution To 4.13Document5 pagesSolution To 4.13Niyati ShahNo ratings yet

- Project 3 CAPM and Fama-French Three Factor Model Professor Natalia Gershun Reynold D'silva Hanxiang Tang Wen GuoDocument7 pagesProject 3 CAPM and Fama-French Three Factor Model Professor Natalia Gershun Reynold D'silva Hanxiang Tang Wen GuoNiyati ShahNo ratings yet

- Intro To Options - TheoryDocument10 pagesIntro To Options - TheoryNiyati ShahNo ratings yet

- Siddharth Gala Project Part 1Document8 pagesSiddharth Gala Project Part 1Niyati ShahNo ratings yet

- Solution To 4.13Document5 pagesSolution To 4.13Niyati ShahNo ratings yet

- Three Perspectives On The Valuation of Derivative InstrumentsDocument10 pagesThree Perspectives On The Valuation of Derivative InstrumentsNiyati ShahNo ratings yet

- Date Gilat Satellite Networks CENTURYLINK INC S&P 500 3 Month T BillDocument3 pagesDate Gilat Satellite Networks CENTURYLINK INC S&P 500 3 Month T BillNiyati ShahNo ratings yet

- Lecture 1 - Review of Bond Concepts and Term Structure of Interest RatesDocument20 pagesLecture 1 - Review of Bond Concepts and Term Structure of Interest RatesNiyati ShahNo ratings yet

- Solution 4.17 Parts 3 and 4Document7 pagesSolution 4.17 Parts 3 and 4Niyati ShahNo ratings yet

- Project 3Document1 pageProject 3Niyati ShahNo ratings yet

- Project 4 Part 2Document13 pagesProject 4 Part 2Niyati ShahNo ratings yet

- Lecture - Eurodollar MarketDocument37 pagesLecture - Eurodollar MarketNiyati ShahNo ratings yet

- Duration Calculation ExampleDocument1 pageDuration Calculation ExampleNiyati ShahNo ratings yet

- HW For M8 - Hedging With OptionsDocument3 pagesHW For M8 - Hedging With OptionsNiyati ShahNo ratings yet

- Solution 4.17 Parts 3 and 4Document7 pagesSolution 4.17 Parts 3 and 4Niyati ShahNo ratings yet

- Book 1Document3 pagesBook 1Niyati ShahNo ratings yet

- Derivatives Problem SetDocument6 pagesDerivatives Problem SetNiyati ShahNo ratings yet

- Measurements and QoS Analysis SwissQualDocument6 pagesMeasurements and QoS Analysis SwissQualkshitij1979No ratings yet

- Gunning 2009Document7 pagesGunning 2009juan diazNo ratings yet

- Missing Number Series Questions Specially For Sbi Po PrelimsDocument18 pagesMissing Number Series Questions Specially For Sbi Po PrelimsKriti SinghaniaNo ratings yet

- Wiz107sr User Manual en v1.0Document29 pagesWiz107sr User Manual en v1.0Pauli Correa ArriagadaNo ratings yet

- C++ Module 2Document58 pagesC++ Module 2Kaye CariñoNo ratings yet

- Chemical EquationsDocument22 pagesChemical EquationsSiti Norasikin MuhyaddinNo ratings yet

- LCD PinoutsDocument1 pageLCD PinoutsPablo Daniel MagallanNo ratings yet

- Oracle ASMDocument46 pagesOracle ASMWaqas ChaudhryNo ratings yet

- Log-PASSAT IMMO-WVWZZZ3CZ7E064873-266870km-165825miDocument13 pagesLog-PASSAT IMMO-WVWZZZ3CZ7E064873-266870km-165825miMihalciuc AlexandruNo ratings yet

- Patient-Centred CareDocument15 pagesPatient-Centred CareMwanja MosesNo ratings yet

- 2D IconsDocument8 pages2D IconsJacky ManNo ratings yet

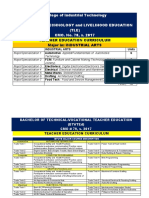

- College of Industrial Technology Bachelor of Technology and Livelihood Education (TLE) CMO. No. 78, S. 2017Document5 pagesCollege of Industrial Technology Bachelor of Technology and Livelihood Education (TLE) CMO. No. 78, S. 2017Industrial TechnologyNo ratings yet

- 001-Numerical Solution of Non Linear EquationsDocument16 pages001-Numerical Solution of Non Linear EquationsAyman ElshahatNo ratings yet

- DVD S2300Document106 pagesDVD S2300cristakeNo ratings yet

- Case Study of Vietinbank Dao Hoang NamDocument14 pagesCase Study of Vietinbank Dao Hoang NamNam ĐàoNo ratings yet

- Educ 13C Questions For MidtermDocument9 pagesEduc 13C Questions For MidtermSannie MonoyNo ratings yet

- ABB Surge Arrester POLIM-H SD - Data Sheet 1HC0075860 E02 ABDocument4 pagesABB Surge Arrester POLIM-H SD - Data Sheet 1HC0075860 E02 ABHan HuangNo ratings yet

- PRACTICA (1) (1) - Páginas-2-4Document3 pagesPRACTICA (1) (1) - Páginas-2-4EDDY POLICARPIO BRAVO HUAMANINo ratings yet

- Jasmine Nagata Smart GoalsDocument5 pagesJasmine Nagata Smart Goalsapi-319625868No ratings yet

- Manual ZappyDocument9 pagesManual Zappyapi-45129352No ratings yet

- PTL Ls Programme HandbookDocument34 pagesPTL Ls Programme Handbooksalak946290No ratings yet

- Unit 8 Grammar Short Test 1 A+B Impulse 2Document1 pageUnit 8 Grammar Short Test 1 A+B Impulse 2karpiarzagnieszka1No ratings yet

- OriginalDocument4 pagesOriginalJob ValleNo ratings yet