You might also like

- Codification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23From EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23No ratings yet

- Status of Prior Audit RecommendationsDocument37 pagesStatus of Prior Audit RecommendationsAlicia NhsNo ratings yet

- Municipality of TAMPAKAN South Cotabato Agency Action Plan Status of Implementation (AAPSI)Document15 pagesMunicipality of TAMPAKAN South Cotabato Agency Action Plan Status of Implementation (AAPSI)Gier Rizaldo BulaclacNo ratings yet

- Part Iii - Status of Implementation of Prior Year'S Audit RecommendationsDocument5 pagesPart Iii - Status of Implementation of Prior Year'S Audit RecommendationsAlicia NhsNo ratings yet

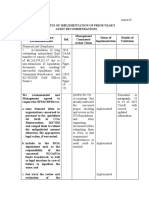

- Status of Implementation of Prior Years' Audit RecommendationsDocument20 pagesStatus of Implementation of Prior Years' Audit Recommendationssandra bolokNo ratings yet

- 10-BacacayAlbay2017 - Status of PYs Audit RecommendationsDocument10 pages10-BacacayAlbay2017 - Status of PYs Audit RecommendationsotabNo ratings yet

- Part Iii-Status of Implementation of Prior Years' Audit RecommendationsDocument7 pagesPart Iii-Status of Implementation of Prior Years' Audit RecommendationsAlicia NhsNo ratings yet

- 2018 SGLG Technical NotesDocument43 pages2018 SGLG Technical NotesGladys LunaNo ratings yet

- SGLG Technical NotesDocument43 pagesSGLG Technical NotesArjay Aleta100% (2)

- Para-Wise Replies To The Inspection Report, 2016Document5 pagesPara-Wise Replies To The Inspection Report, 2016MinlalNo ratings yet

- 8 COA Actions Taken FinalDocument4 pages8 COA Actions Taken FinalDOLE West Leyte Field OfficeNo ratings yet

- Status of Implementation of Prior Years' Unimplemented Audit RecommendationsDocument35 pagesStatus of Implementation of Prior Years' Unimplemented Audit Recommendationssandra bolokNo ratings yet

- Commission On AuditDocument207 pagesCommission On AuditJaniceNo ratings yet

- 10-CalapanCity2019 Part3-Status of PYs RecommDocument24 pages10-CalapanCity2019 Part3-Status of PYs RecommkQy267BdTKNo ratings yet

- Annex H Status of Implementation of PYs Audit Recommendations 2019Document7 pagesAnnex H Status of Implementation of PYs Audit Recommendations 2019LA AkutNo ratings yet

- Total Combined File-1Document36 pagesTotal Combined File-1Shefali TailorNo ratings yet

- RTS 2022 DARPO Davao Del SurDocument28 pagesRTS 2022 DARPO Davao Del SurLouie Mark lligan (COA - Louie Mark Iligan)No ratings yet

- 01 Technical Notes For SGLG LGPMSDocument59 pages01 Technical Notes For SGLG LGPMSMichi GoNo ratings yet

- Prior Years' Audit Recommendations StatusDocument8 pagesPrior Years' Audit Recommendations Statussandra bolokNo ratings yet

- San Luis, Batangas Implements 2017 Audit RecommendationsDocument7 pagesSan Luis, Batangas Implements 2017 Audit RecommendationsKei PaceñoNo ratings yet

- Status of Implementation of Prior Years' Audit RecommendationsDocument14 pagesStatus of Implementation of Prior Years' Audit RecommendationsAngel BacaniNo ratings yet

- Executive Summary: Highlights of Financial OperationsDocument12 pagesExecutive Summary: Highlights of Financial OperationsJaniceNo ratings yet

- SRE LLP Annual Report 2017-18Document9 pagesSRE LLP Annual Report 2017-18Saba MullaNo ratings yet

- Prior Audit Findings StatusDocument12 pagesPrior Audit Findings StatusAlicia NhsNo ratings yet

- Audit MTP 1 ADocument11 pagesAudit MTP 1 ATushar MalhotraNo ratings yet

- Audit Recommendations StatusDocument117 pagesAudit Recommendations StatusMaria KarlaNo ratings yet

- 10-TaclobanCity2018 Part3-Status of PY's RecommDocument13 pages10-TaclobanCity2018 Part3-Status of PY's Recommrobert lachicaNo ratings yet

- Draft Technical Notes SGLG 2023 - National Orientation 1Document116 pagesDraft Technical Notes SGLG 2023 - National Orientation 1aeron antonioNo ratings yet

- 2023 SGLG Technical Notes - As of 06 June 2023Document134 pages2023 SGLG Technical Notes - As of 06 June 2023Ann ManaloconNo ratings yet

- (Draft) Technical Notes SGLG 2023 Financial Adminsitration and SustainabilityDocument6 pages(Draft) Technical Notes SGLG 2023 Financial Adminsitration and SustainabilityDivina Joy Ventura-GonzalesNo ratings yet

- COA & COMELEC R4A - APMT 2017 ML SAOR With DetailsDocument8 pagesCOA & COMELEC R4A - APMT 2017 ML SAOR With DetailsVicky Danila AlbanoNo ratings yet

- Draft Technical Notes SGLG 2023 - National OrientationDocument115 pagesDraft Technical Notes SGLG 2023 - National OrientationMark Kenneth AcostaNo ratings yet

- (Draft) Technical Notes SGLG 2023 - National OrientationDocument95 pages(Draft) Technical Notes SGLG 2023 - National OrientationRhea TiemsemNo ratings yet

- STRATEGIES TO IMPROVE LOCAL AUTHORITY PERFORMANCEDocument9 pagesSTRATEGIES TO IMPROVE LOCAL AUTHORITY PERFORMANCEcholaNo ratings yet

- Status of Implementation of Prior Year'S Audit RecommendationsDocument15 pagesStatus of Implementation of Prior Year'S Audit RecommendationsGloria AlamilNo ratings yet

- La-Paz-Executive-Summary-2019Document10 pagesLa-Paz-Executive-Summary-2019Rene BalloNo ratings yet

- Status of Implementation of Prior Years' Audit RecommendationsDocument14 pagesStatus of Implementation of Prior Years' Audit RecommendationsFidela PaguioNo ratings yet

- Financial Statements YE 31.12.21Document15 pagesFinancial Statements YE 31.12.21maharajabby81No ratings yet

- Branch Auditor's Report: Raman Manoj& CoDocument25 pagesBranch Auditor's Report: Raman Manoj& CoDon bhaiNo ratings yet

- 01 - Technical Notes For SGLG LGPMS Field TestDocument58 pages01 - Technical Notes For SGLG LGPMS Field Testnorman100% (1)

- An Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsDocument38 pagesAn Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsPhrexilyn PajarilloNo ratings yet

- 09-PA2018 Part2-Observations and RecommendationsDocument29 pages09-PA2018 Part2-Observations and RecommendationsVERA FilesNo ratings yet

- COA Audit Report Highlights Issues with Financial Records and Accountabilities of Patnanungan MunicipalityDocument93 pagesCOA Audit Report Highlights Issues with Financial Records and Accountabilities of Patnanungan MunicipalityNascelAguilarGabitoNo ratings yet

- Executive Summary of Lugait Municipality Audit ReportDocument4 pagesExecutive Summary of Lugait Municipality Audit ReportOZ La NB AnamiNo ratings yet

- COA Audit Report on Taytay Municipality 2009Document57 pagesCOA Audit Report on Taytay Municipality 2009Ipah L. SaidNo ratings yet

- Government AccountingDocument28 pagesGovernment AccountingRazel TercinoNo ratings yet

- Performance in Figures: Balance Sheet Profit & Loss A/c Schedules Notes To AccountsDocument41 pagesPerformance in Figures: Balance Sheet Profit & Loss A/c Schedules Notes To Accountskarthik gunashekharNo ratings yet

- Monitoring Coa ValidationDocument14 pagesMonitoring Coa Validationnoelbautista.tsulawNo ratings yet

- COA-SaranganiPov2019 Audit ReportDocument186 pagesCOA-SaranganiPov2019 Audit ReportRascille LaranasNo ratings yet

- OSFI Internal Audit Report on Finance RevenueDocument19 pagesOSFI Internal Audit Report on Finance RevenueCharu Panchal Bedi100% (1)

- 2023 SGLG Technical Notes - As of 06 June 2023 1Document132 pages2023 SGLG Technical Notes - As of 06 June 2023 1LGU San Jose CSNo ratings yet

- Partially Implemented Audit RecommendationsDocument5 pagesPartially Implemented Audit RecommendationsJonson PalmaresNo ratings yet

- Executive Summary of Baao Municipality AuditDocument4 pagesExecutive Summary of Baao Municipality Auditsandra bolokNo ratings yet

- BinalonanWD-R1 ES2018Document4 pagesBinalonanWD-R1 ES2018J JaNo ratings yet

- Part Iii - Status of Implementation of Prior Year'S Audit RecommendationDocument4 pagesPart Iii - Status of Implementation of Prior Year'S Audit RecommendationAlicia NhsNo ratings yet

- Status of Implementation of Prior Year's Recommendations CY 2016Document8 pagesStatus of Implementation of Prior Year's Recommendations CY 2016Mary Jane Katipunan CalumbaNo ratings yet

- Nov 18 PaperDocument21 pagesNov 18 Paperritz meshNo ratings yet

- Republic of The Philippines Commonwealth Avenue, Quezon CityDocument5 pagesRepublic of The Philippines Commonwealth Avenue, Quezon CityOrlando V. Madrid Jr.No ratings yet

- © The Institute of Chartered Accountants of IndiaDocument9 pages© The Institute of Chartered Accountants of IndiaGJ ELASHREEVALLINo ratings yet

- Ankur TripathiDocument2 pagesAnkur TripathiThe Cultural CommitteeNo ratings yet

- Grade 8 - SPS PacquiaoDocument2 pagesGrade 8 - SPS PacquiaoAlicia NhsNo ratings yet

- 17th and 18th Centuries: Battle of Vienna Ottoman EmpireDocument1 page17th and 18th Centuries: Battle of Vienna Ottoman EmpireAlicia NhsNo ratings yet

- Austria 2Document1 pageAustria 2Alicia NhsNo ratings yet

- 3rd Quarter QuizDocument8 pages3rd Quarter QuizAlicia NhsNo ratings yet

- 19th Century: Congress of Vienna French Revolutionary Wars Napoleonic Wars Holy Roman EmpireDocument1 page19th Century: Congress of Vienna French Revolutionary Wars Napoleonic Wars Holy Roman EmpireAlicia NhsNo ratings yet

- Austria: Jump To Navigationjump To SearchDocument4 pagesAustria: Jump To Navigationjump To SearchAlicia NhsNo ratings yet

- Prehistory and Ancient History: Prehistoric North Africa North Africa During AntiquityDocument2 pagesPrehistory and Ancient History: Prehistoric North Africa North Africa During AntiquityAlicia NhsNo ratings yet

- AlgeriaDocument1 pageAlgeriaBercia MondialuNo ratings yet

- Middle Ages: Venus of Willendorf Museum of Natural History ViennaDocument1 pageMiddle Ages: Venus of Willendorf Museum of Natural History ViennaAlicia NhsNo ratings yet

- Modern: Arusha Declaration MonumentDocument2 pagesModern: Arusha Declaration MonumentAlicia NhsNo ratings yet

- Algeria 2Document1 pageAlgeria 2Alicia NhsNo ratings yet

- Algeria 5Document1 pageAlgeria 5Alicia NhsNo ratings yet

- Tanzania 3Document2 pagesTanzania 3Alicia NhsNo ratings yet

- Middle Ages: Medieval Muslim AlgeriaDocument2 pagesMiddle Ages: Medieval Muslim AlgeriaAlicia NhsNo ratings yet

- Albania 2Document1 pageAlbania 2Alicia NhsNo ratings yet

- Albania (: A (W) L - Nee-ƏDocument1 pageAlbania (: A (W) L - Nee-ƏAlicia NhsNo ratings yet

- Albania 4Document1 pageAlbania 4Alicia NhsNo ratings yet

- Post-Conflict PeriodDocument1 pagePost-Conflict PeriodAlicia NhsNo ratings yet

- Geography: Geography of Tanzania Zanzibar ArchipelagoDocument1 pageGeography: Geography of Tanzania Zanzibar ArchipelagoAlicia NhsNo ratings yet

- Rajapaksa Brothers in PowerDocument1 pageRajapaksa Brothers in PowerAlicia NhsNo ratings yet

- Tanzania (Tanzania (: Homo Homo Erectus Homo SapiensDocument2 pagesTanzania (Tanzania (: Homo Homo Erectus Homo SapiensAlicia NhsNo ratings yet

- Kandyan Period (1594-1815) : Kingdom of KandyDocument2 pagesKandyan Period (1594-1815) : Kingdom of KandyAlicia NhsNo ratings yet

- Tanzania 2Document2 pagesTanzania 2Alicia NhsNo ratings yet

- Crisis of The Sixteenth Century (1505-1594) : Portuguese InterventionDocument1 pageCrisis of The Sixteenth Century (1505-1594) : Portuguese InterventionAlicia NhsNo ratings yet

- Republic: Junius Jayewardene Tamil United Liberation Front Appapillai AmirthalingamDocument2 pagesRepublic: Junius Jayewardene Tamil United Liberation Front Appapillai AmirthalingamAlicia NhsNo ratings yet

- Sri Lankan Civil War 1987-89 JVP Insurrection: Main Articles: andDocument1 pageSri Lankan Civil War 1987-89 JVP Insurrection: Main Articles: andAlicia NhsNo ratings yet

- Polonnaruwa Period Kingdom of PolonnaruwaDocument2 pagesPolonnaruwa Period Kingdom of PolonnaruwaAlicia NhsNo ratings yet

- Sri Lanka (1948-Present) : IndependenceDocument1 pageSri Lanka (1948-Present) : IndependenceAlicia NhsNo ratings yet

- 1971 JVP Insurrection: Main ArticleDocument2 pages1971 JVP Insurrection: Main ArticleAlicia NhsNo ratings yet

- Prehistory of Sri Lanka: Early Inhabitants and Archaeological EvidenceDocument1 pagePrehistory of Sri Lanka: Early Inhabitants and Archaeological EvidenceAlicia NhsNo ratings yet

- Gonzales v. Hechanova, G.R. No. L-21897, (October 22, 1963), 118 PHIL 1065-1089Document9 pagesGonzales v. Hechanova, G.R. No. L-21897, (October 22, 1963), 118 PHIL 1065-1089RJCenitaNo ratings yet

- Навчання у НАВСDocument29 pagesНавчання у НАВСДана ТокарNo ratings yet

- FS Form 1071 (Statement of Ownership)Document2 pagesFS Form 1071 (Statement of Ownership)Benne James100% (3)

- Fifth Circuit Vaccine OrderDocument4 pagesFifth Circuit Vaccine OrderIan MillhiserNo ratings yet

- Fuentes Vs RocaDocument2 pagesFuentes Vs RocakamiruhyunNo ratings yet

- Insured May Sue Insurer Despite Policy Payable to MortgageeDocument7 pagesInsured May Sue Insurer Despite Policy Payable to MortgageeSometimes goodNo ratings yet

- Christian Tomuschat - Jean-Marc Thouvenin - The Fundamental Rules of The International Legal Order - Jus Cogens and Obligations Erga Omnes (2005)Document483 pagesChristian Tomuschat - Jean-Marc Thouvenin - The Fundamental Rules of The International Legal Order - Jus Cogens and Obligations Erga Omnes (2005)gargiii.singh09No ratings yet

- Appointment Letter-Contract: National Highway Authority of IndiaDocument2 pagesAppointment Letter-Contract: National Highway Authority of IndiaDeepak SinghNo ratings yet

- 54 Samson Vs AguirreDocument4 pages54 Samson Vs AguirreA M I R ANo ratings yet

- EFA AutoDesk Disbursement AuthorizationDocument1 pageEFA AutoDesk Disbursement AuthorizationKhoa PhanNo ratings yet

- Korean Airlines Co., LTD., Petitioner, vs. Court ofDocument2 pagesKorean Airlines Co., LTD., Petitioner, vs. Court ofJoshua OuanoNo ratings yet

- Schedules in Indian ConstitutionDocument4 pagesSchedules in Indian ConstitutionSurya Pratap SinghNo ratings yet

- DOE Application FormDocument2 pagesDOE Application FormAlyssa ValerioNo ratings yet

- Benguet Corp vs CBAA Tax Ruling on Tailings DamDocument2 pagesBenguet Corp vs CBAA Tax Ruling on Tailings DamFe FernandezNo ratings yet

- Request For Removal From The Register of Marriage CelebrantsDocument3 pagesRequest For Removal From The Register of Marriage Celebrantspretea msNo ratings yet

- Karen Tayag Vertido V The PhilippinesDocument4 pagesKaren Tayag Vertido V The PhilippinesAstrid Gopo Brisson100% (1)

- Fiduciary RelationshipsDocument29 pagesFiduciary RelationshipsRavikantDhanushDeshmukhNo ratings yet

- Narte, Luzvminda - Deed of Sale of Parcel of LandDocument2 pagesNarte, Luzvminda - Deed of Sale of Parcel of LandRL AVNo ratings yet

- Indosuez Wealth ManagementDocument5 pagesIndosuez Wealth ManagementMohjamNo ratings yet

- Commercial Dispatch Eedition 3-13-19Document16 pagesCommercial Dispatch Eedition 3-13-19The DispatchNo ratings yet

- Lost Holographic Will Copy AllowedDocument1 pageLost Holographic Will Copy AllowedJoesil Dianne SempronNo ratings yet

- Windows 8.1 SDK LicenseDocument20 pagesWindows 8.1 SDK LicenseJohan VargasNo ratings yet

- Court denies preliminary injunction for excavations on private roadDocument3 pagesCourt denies preliminary injunction for excavations on private roadCla BANo ratings yet

- Reference No. CEF15532025-43220905202102744314Document7 pagesReference No. CEF15532025-43220905202102744314Lenard UsonNo ratings yet

- Radio Communications of The Philippines, Inc Vs National Telecommunications Commission and Kayumanggi Radio Network IncDocument3 pagesRadio Communications of The Philippines, Inc Vs National Telecommunications Commission and Kayumanggi Radio Network IncBananaNo ratings yet

- Personal JurisdictionDocument10 pagesPersonal JurisdictionMorgyn Shae CooperNo ratings yet

- Metropolitan Trial Court: MemorandumDocument7 pagesMetropolitan Trial Court: Memorandum0506sheltonNo ratings yet

- 02 Government Procurement 101 Key Features of GPRA and Procurement OrganizationDocument59 pages02 Government Procurement 101 Key Features of GPRA and Procurement Organizationtess santosNo ratings yet

- ANTONIO M. SERRANO v. GALLANT MARITIME SERVICESDocument35 pagesANTONIO M. SERRANO v. GALLANT MARITIME SERVICESkhate alonzoNo ratings yet

- Community Immersion Program of PNPDocument40 pagesCommunity Immersion Program of PNParlene landocan91% (11)