You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Nigerian Electricity Market Experiment - A Critical Appraisal of The PHCN Privatisation - LexologyDocument8 pagesThe Nigerian Electricity Market Experiment - A Critical Appraisal of The PHCN Privatisation - LexologySunny EnergyEfficiency EjimaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

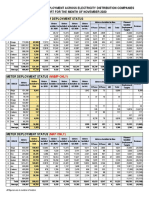

- Nov-2020 Meter Deployment StatusDocument1 pageNov-2020 Meter Deployment StatusSunny EnergyEfficiency Ejima100% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Connection Methodology I by NERCDocument5 pagesConnection Methodology I by NERCashameensNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- MAP FAQ FinalDocument5 pagesMAP FAQ FinalSunny EnergyEfficiency EjimaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- CommunismDocument4 pagesCommunismVeda meghanaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Sustainability Teams & CRM ExamplesDocument22 pagesSustainability Teams & CRM ExamplesNivedita TanyaNo ratings yet

- Howida BedirDocument1 pageHowida BedirSaly elhalfawyNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Dksksabs DDocument70 pagesDksksabs DShalin ParikhNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Guide To US AML Requirements 5thedition ProtivitiDocument474 pagesGuide To US AML Requirements 5thedition ProtiviticheejustinNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- CHAPTER 21 The Theory of Consumer ChoiceDocument5 pagesCHAPTER 21 The Theory of Consumer ChoiceNEIL OBINARIONo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- US Seniors Struggle with Healthcare CostsDocument13 pagesUS Seniors Struggle with Healthcare CostsAmna HayatNo ratings yet

- CIS309 MidtermDocument15 pagesCIS309 MidtermGabriel Garza100% (6)

- Template Presentasi Technical Exchange Forum 2021 + BriefingDocument25 pagesTemplate Presentasi Technical Exchange Forum 2021 + Briefingdenstar silalahiNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- UT Dallas Syllabus For Econ2301.001.10s Taught by Luba Ketsler (lxk010300)Document7 pagesUT Dallas Syllabus For Econ2301.001.10s Taught by Luba Ketsler (lxk010300)UT Dallas Provost's Technology GroupNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Carroway Environmental David JohnstonDocument8 pagesCarroway Environmental David JohnstonDave JohnstonNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Recycling: Reduce, Reuse, RecycleDocument10 pagesRecycling: Reduce, Reuse, RecycleNgânn Khánh ĐinhNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Fund Chapter 6Document18 pagesFund Chapter 6aryabhatmathsNo ratings yet

- BA 114.1 - Module2 - Receivables - Exercise 1 PDFDocument4 pagesBA 114.1 - Module2 - Receivables - Exercise 1 PDFKurt Orfanel0% (1)

- Impact of FDI in IndiaDocument24 pagesImpact of FDI in IndiaBinoy JoseNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Gamuda BerhadDocument2 pagesGamuda BerhadHui EnNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Reservation Information Itinerary ID: Total You Will Receive: IDR 1346400Document2 pagesReservation Information Itinerary ID: Total You Will Receive: IDR 1346400Achmad Furqon SyaifullahNo ratings yet

- Resilience - Samuel YazoDocument23 pagesResilience - Samuel YazoSamuel YazoNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- G.Tian - Microeconomic TheoryDocument253 pagesG.Tian - Microeconomic Theorytony_stoyanov2108No ratings yet

- 28pairs CS Basic ManualDocument61 pages28pairs CS Basic ManualNik Mohd FikriNo ratings yet

- (Mal) Nutrition North: A Failure of Policy Formation by The Canadian Government in NunavutDocument5 pages(Mal) Nutrition North: A Failure of Policy Formation by The Canadian Government in NunavutL J de GaraNo ratings yet

- 10TH TAMILfull Guide KalviexpressDocument424 pages10TH TAMILfull Guide KalviexpressT.A.S.K tricks affairs and science with KAPEL50% (6)

- Homeless College Student Reserach EssayDocument20 pagesHomeless College Student Reserach Essayapi-317134211100% (1)

- Corporate Governance ProjectDocument69 pagesCorporate Governance ProjectSiddiqueJoiyaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Paper 5Document4 pagesPaper 5hbyhNo ratings yet

- Interwood MobelDocument32 pagesInterwood MobelHSNo ratings yet

- Oman Roads and Bridges Project Snapshot: Batinah Coastal Road - Phase 2Document4 pagesOman Roads and Bridges Project Snapshot: Batinah Coastal Road - Phase 2ScribdInOmanNo ratings yet

- Table of ContentDocument6 pagesTable of Contentiola cher romeroNo ratings yet

- Services Marketing & Brand ManagementDocument29 pagesServices Marketing & Brand ManagementMansi KapoorNo ratings yet

- Formal Letter - A Dissatisfaction With A Broken Washing MachineDocument3 pagesFormal Letter - A Dissatisfaction With A Broken Washing MachineSHENNIE WONG PUI CHI MoeNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)