You might also like

- 2009.12.19 ASFPrincipalForbearanceMarketViewLetterDocument39 pages2009.12.19 ASFPrincipalForbearanceMarketViewLetterfred.joseph3321No ratings yet

- Deed of ReconveyanceDocument1 pageDeed of ReconveyanceKaren DyNo ratings yet

- Chapter 01+02 Investment Bodie Test BankDocument73 pagesChapter 01+02 Investment Bodie Test BankTami DoanNo ratings yet

- Loan Modification CalculatorDocument4 pagesLoan Modification CalculatorElizabeth ThomasNo ratings yet

- CPA Financial Statement Documentation WPsDocument569 pagesCPA Financial Statement Documentation WPsChinh Le DinhNo ratings yet

- Personal Monthly BudgetDocument2 pagesPersonal Monthly Budgetbernadeth_remaNo ratings yet

- Personal Budget TemplateDocument18 pagesPersonal Budget TemplateJimoh AladeNo ratings yet

- Financial Goal Tracker Version 4 (Dec 25 2017)Document351 pagesFinancial Goal Tracker Version 4 (Dec 25 2017)Parminder SinghNo ratings yet

- Home Mortgage CalculatorDocument1 pageHome Mortgage Calculatorpweaver1973No ratings yet

- Personal Budget SpreadsheetDocument7 pagesPersonal Budget Spreadsheetamiller1987No ratings yet

- Dashboard: Profit & Loss StatementDocument3 pagesDashboard: Profit & Loss StatementKhairie Rahim0% (1)

- Personal Financial StatementDocument1 pagePersonal Financial StatementDharmaMaya ChandrahasNo ratings yet

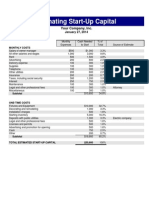

- Estimating Start-Up Capital: Your Company, IncDocument1 pageEstimating Start-Up Capital: Your Company, IncnightclownNo ratings yet

- Business Financial PlanDocument10 pagesBusiness Financial PlanMónica EstefaníaNo ratings yet

- Personal-Monthly-Budget 1Document6 pagesPersonal-Monthly-Budget 1api-296696430No ratings yet

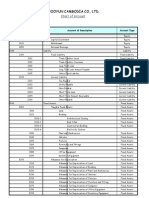

- Worksheet in Chart AccountDocument3 pagesWorksheet in Chart AccountthorseiratyNo ratings yet

- (Template) Asset and Equipment TrackingDocument6 pages(Template) Asset and Equipment TrackingSaren NovinzaNo ratings yet

- Personal Budget SpreadsheetDocument8 pagesPersonal Budget SpreadsheetCraig Richard Minson100% (1)

- Tax Cheatsheet LandscapeDocument2 pagesTax Cheatsheet LandscapeEeLin Chan100% (1)

- Accounting Excel Reports - Report Generalledger ExcelDocument36 pagesAccounting Excel Reports - Report Generalledger ExcelMark Ceddrick MioleNo ratings yet

- Wave Fearless Accounting GuideDocument114 pagesWave Fearless Accounting Guidepta123100% (1)

- Personal Budget TemplateDocument6 pagesPersonal Budget TemplateMrsRainesNo ratings yet

- Personal BudgetDocument40 pagesPersonal BudgetSpreadsheetZONENo ratings yet

- Family Monthly Budget PlannerDocument4 pagesFamily Monthly Budget PlannerastephenrajNo ratings yet

- Excel Timeline TemplateDocument8 pagesExcel Timeline TemplatesapcanNo ratings yet

- Zero Based Budget Template - 0Document4 pagesZero Based Budget Template - 0Nabila ArifannisaNo ratings yet

- Home Budget Worksheet: Income CategoriesDocument3 pagesHome Budget Worksheet: Income Categoriesdavidjc77No ratings yet

- Setting Up Chart of AccountsDocument11 pagesSetting Up Chart of AccountsFaithful ChenNo ratings yet

- Doc-Balance Sheet Cheat Sheet PDFDocument2 pagesDoc-Balance Sheet Cheat Sheet PDFConnor McloudNo ratings yet

- Household Budget PlannerDocument5 pagesHousehold Budget PlannerNedim Fiennes Hrustich100% (1)

- Excel Advanced Excel For Finance EXERCISEDocument91 pagesExcel Advanced Excel For Finance EXERCISEhaz002No ratings yet

- Real Estate Closing Transaction ChecklistDocument2 pagesReal Estate Closing Transaction ChecklistFrancine FelskeNo ratings yet

- Real - Estate - Analysis 3Document10 pagesReal - Estate - Analysis 3Cris MárquezNo ratings yet

- Excel Business Plan TemplateDocument26 pagesExcel Business Plan TemplateAdil Hassan100% (1)

- Financial Calculator Find Future Value - Time Line: Solving ForDocument3 pagesFinancial Calculator Find Future Value - Time Line: Solving ForPiyush KakkarNo ratings yet

- Monthly BudgetDocument8 pagesMonthly BudgetNhanVoNo ratings yet

- Household Budget PlannerDocument5 pagesHousehold Budget PlannerHaruna.2008 Ghareeb2003No ratings yet

- Profit and Loss WorksheetDocument1 pageProfit and Loss WorksheetNEWS CENTER MaineNo ratings yet

- GnattDocument4 pagesGnattapi-273809196No ratings yet

- Line Item Renovation Budget: Cost As % of Total Accepted Bid or Cost Change OrdersDocument4 pagesLine Item Renovation Budget: Cost As % of Total Accepted Bid or Cost Change Ordersbillybob801No ratings yet

- Loan Processing or Underwriting Customer Service (Call Center) oDocument4 pagesLoan Processing or Underwriting Customer Service (Call Center) oapi-76958881No ratings yet

- Employee Handbook Template 04Document9 pagesEmployee Handbook Template 04petebakarNo ratings yet

- Family Budget PlannerDocument11 pagesFamily Budget Plannercgaona88No ratings yet

- Monthly Budget PlannerDocument6 pagesMonthly Budget Plannerppavan_hr3376No ratings yet

- Personal Net Worth Calculator1Document3 pagesPersonal Net Worth Calculator1Sofian SukamtoNo ratings yet

- Business-Budget 12monthsDocument5 pagesBusiness-Budget 12monthsEyob SNo ratings yet

- Greensheet Kenai PDFDocument2 pagesGreensheet Kenai PDFBen GorrNo ratings yet

- D2451 Basic TQM-Toolbox 2007 AlumnosDocument17 pagesD2451 Basic TQM-Toolbox 2007 AlumnosRafael HBNo ratings yet

- Home Budget TemplateDocument2 pagesHome Budget TemplatemanojNo ratings yet

- Property Info: Operation CostsDocument2 pagesProperty Info: Operation CostsKilogram LossNo ratings yet

- Formulas and Sample CalculationsDocument8 pagesFormulas and Sample CalculationsBrave KingNo ratings yet

- SCDIS 200 Information Security and Privacy StandardsDocument201 pagesSCDIS 200 Information Security and Privacy Standardssadim22No ratings yet

- Cost Estimate TemplateDocument61 pagesCost Estimate TemplateCorbyFrielNo ratings yet

- Budgeting Calculator Spreadsheet With Guidelines Ver 1 61Document4 pagesBudgeting Calculator Spreadsheet With Guidelines Ver 1 61Thomas McquillanNo ratings yet

- Personal Budget: Percentage of Income SpentDocument4 pagesPersonal Budget: Percentage of Income SpentRob CrispNo ratings yet

- Seller's PacketDocument13 pagesSeller's PacketKelsey DeMers75% (4)

- Budget Rock Star (Worksheets)Document8 pagesBudget Rock Star (Worksheets)Nursuhaidah SukorNo ratings yet

- Sample Budget Template 1: (Agency Name) (Program Name)Document9 pagesSample Budget Template 1: (Agency Name) (Program Name)harvjagNo ratings yet

- Personal Budget SpreadsheetDocument6 pagesPersonal Budget Spreadsheetotiliab84No ratings yet

- Monthly Budget Template: Sheet1Document2 pagesMonthly Budget Template: Sheet1Rufino Gerard Moreno IIINo ratings yet

- Simple Home Affordability Analysis Chart1Document1 pageSimple Home Affordability Analysis Chart1ameliaNo ratings yet

- Buy A House or RentDocument4 pagesBuy A House or RentUmair KamranNo ratings yet

- Home Mortgage CalculatorDocument26 pagesHome Mortgage CalculatorianachieviciNo ratings yet

- Annual CalendarDocument1 pageAnnual CalendarRomi RobertoNo ratings yet

- Shift ScheduleDocument2 pagesShift ScheduleRomi RobertoNo ratings yet

- Camping Checklist: Essentials / Survival Sleep GearDocument2 pagesCamping Checklist: Essentials / Survival Sleep GearRomi Roberto100% (1)

- Income StatementDocument3 pagesIncome StatementRomi RobertoNo ratings yet

- Bisnis Cost StartupDocument11 pagesBisnis Cost StartupRomi RobertoNo ratings yet

- January 2019: (Calendar Title)Document12 pagesJanuary 2019: (Calendar Title)Romi RobertoNo ratings yet

- Fax Cover LetterDocument1 pageFax Cover LetterRomi RobertoNo ratings yet

- Weekly Meal PlannerDocument12 pagesWeekly Meal PlannerRomi RobertoNo ratings yet

- Car Bill of SaleDocument1 pageCar Bill of SaleRomi Roberto100% (1)

- Basic Meeting AgendaDocument1 pageBasic Meeting AgendaRomi RobertoNo ratings yet

- Purchase Order: (Company Name)Document4 pagesPurchase Order: (Company Name)Romi RobertoNo ratings yet

- House and Wire Real Estate PPT Templates Widescreen1Document2 pagesHouse and Wire Real Estate PPT Templates Widescreen1Romi RobertoNo ratings yet

- Free PPT Templates: InsertDocument2 pagesFree PPT Templates: InsertRomi RobertoNo ratings yet

- Attendance RecordDocument1 pageAttendance RecordRomi RobertoNo ratings yet

- Markting Initiatives Roadmap TemplateDocument7 pagesMarkting Initiatives Roadmap TemplateRomi RobertoNo ratings yet

- Digital Marketing Plan TemplateDocument13 pagesDigital Marketing Plan TemplateRomi Roberto0% (1)

- MapansaDocument2 pagesMapansaJay Cabale AcevedoNo ratings yet

- A Recession Is When Your Neighbour Loses His Job. A Depression Is When You Lose Your JobDocument83 pagesA Recession Is When Your Neighbour Loses His Job. A Depression Is When You Lose Your JobAppurva SharmaNo ratings yet

- Madura FMI9e IM Ch13Document9 pagesMadura FMI9e IM Ch13Stanley HoNo ratings yet

- ICARE Preweek FAR by Sir RainDocument13 pagesICARE Preweek FAR by Sir Rainjohn paulNo ratings yet

- Bar Questions For FinalsDocument9 pagesBar Questions For Finalsarielramada100% (1)

- 1 s2.0 S0264837722001508 MainDocument15 pages1 s2.0 S0264837722001508 Mainsulhi_08No ratings yet

- 3 Vda de Urbano V GSIS Sales PDFDocument3 pages3 Vda de Urbano V GSIS Sales PDFNikki MendozaNo ratings yet

- DP 4 - 5 Influences On Financial Management ActivitiesDocument8 pagesDP 4 - 5 Influences On Financial Management ActivitiesChristian McLoughlinNo ratings yet

- Silicon Valley Bank Unit EconomicsDocument5 pagesSilicon Valley Bank Unit EconomicsPierpaolo VergatiNo ratings yet

- Spouses Mallari vs. Prudential Bank DigestDocument2 pagesSpouses Mallari vs. Prudential Bank DigestkristofferNo ratings yet

- Mirasol V CADocument3 pagesMirasol V CAAnonymous 5MiN6I78I0100% (1)

- Repossessions in ScotlandDocument17 pagesRepossessions in ScotlandprincessmeyaNo ratings yet

- Core Banking Systems SurveyDocument71 pagesCore Banking Systems Surveyborisg3100% (1)

- GMAT RC - Mixed - Set 1 (Questions) (Veritas)Document4 pagesGMAT RC - Mixed - Set 1 (Questions) (Veritas)Kay QNo ratings yet

- Act No. 21 of 2005. The Himachal Pradesh Apartment and Property Regulation Act, 2005Document27 pagesAct No. 21 of 2005. The Himachal Pradesh Apartment and Property Regulation Act, 2005Anuj LakhanpalNo ratings yet

- DEDUCTIONSDocument21 pagesDEDUCTIONSlet me live in peaceNo ratings yet

- MCQs - Secondary MarketsDocument8 pagesMCQs - Secondary Marketskazi A.R RafiNo ratings yet

- Research Paper For Credit CrisisDocument31 pagesResearch Paper For Credit CrisisShabana KhanNo ratings yet

- Wa0047.Document2 pagesWa0047.daniellparisNo ratings yet

- Pledge, Antichresis and Mortgage (Case Digests by @mcvinicious) PDFDocument33 pagesPledge, Antichresis and Mortgage (Case Digests by @mcvinicious) PDFVeen Galicinao FernandezNo ratings yet

- Solicitors Accounts Uk NotesDocument4 pagesSolicitors Accounts Uk NotesMaizaRidzuanNo ratings yet

- Bamboo Loan (LBP-DBP)Document6 pagesBamboo Loan (LBP-DBP)Enrique SantosNo ratings yet

- The Sociology of Finance Carruthers and Kim ARS PaperDocument24 pagesThe Sociology of Finance Carruthers and Kim ARS PaperThais MoreiraNo ratings yet

- Foreclosing Modifications - How Servicer Incentives Discourage Loan ModificationsDocument86 pagesForeclosing Modifications - How Servicer Incentives Discourage Loan ModificationsRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Case Digest Tolentino vs. GonzalesDocument2 pagesCase Digest Tolentino vs. GonzalesDiane Dee Yanee75% (4)

- Retail BankingDocument200 pagesRetail BankingJugnu mahourNo ratings yet

- An Analysis of Retail Banking in Indian Banking SectorDocument90 pagesAn Analysis of Retail Banking in Indian Banking SectorShailendra Soni50% (4)