You might also like

- NDA TemplateDocument8 pagesNDA TemplateCha AgaderNo ratings yet

- Why Don't I Feel Good Enough Using Attachment Theory To Find A Solution (Helen Dent)Document265 pagesWhy Don't I Feel Good Enough Using Attachment Theory To Find A Solution (Helen Dent)Rucsandra MurzeaNo ratings yet

- Sosus TodayDocument43 pagesSosus TodayBùi Trường GiangNo ratings yet

- Coins of England & the United Kingdom (2021): Decimal IssuesFrom EverandCoins of England & the United Kingdom (2021): Decimal IssuesEmma HowardNo ratings yet

- Free Playgirl Magazine PDFDocument2 pagesFree Playgirl Magazine PDFTay9% (11)

- Community Currency Slide ShowDocument33 pagesCommunity Currency Slide ShowCarl MullanNo ratings yet

- Serial Number DatingDocument13 pagesSerial Number DatingFederico SanchezNo ratings yet

- 图解市场Document37 pages图解市场meganmaoNo ratings yet

- Global Mineral Exploration, Production and TechnologyDocument30 pagesGlobal Mineral Exploration, Production and TechnologyLuis MacedoNo ratings yet

- Olve Torvanger Einar H. Bandlien Svein E. JohansenDocument32 pagesOlve Torvanger Einar H. Bandlien Svein E. Johansengt295038No ratings yet

- CHester Norbert Partnership POADocument4 pagesCHester Norbert Partnership POAMatthew Bloomfield0% (1)

- Sales Made by Each SalesmanDocument3 pagesSales Made by Each SalesmanKanchan Gandhi OdNo ratings yet

- Poblacion FuturaDocument2 pagesPoblacion FuturaLisbeth YagualNo ratings yet

- Project 5 PDFDocument3 pagesProject 5 PDFapi-509845050No ratings yet

- Beauty Andarsurakshabahar OferDocument2 pagesBeauty Andarsurakshabahar Oferharik ReddyNo ratings yet

- History of Hydraulic FracturingDocument7 pagesHistory of Hydraulic FracturingMaicol AlfaroNo ratings yet

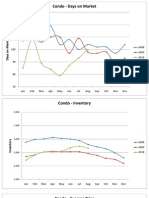

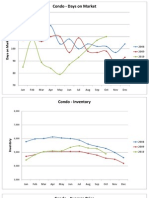

- August 2010 Newsletter Charts - CondoDocument2 pagesAugust 2010 Newsletter Charts - CondopsobaniaNo ratings yet

- October 2010 - Newsletter Charts CondoDocument2 pagesOctober 2010 - Newsletter Charts CondopsobaniaNo ratings yet

- Assignment1 SolutionDocument21 pagesAssignment1 SolutionxxxNo ratings yet

- 2010 November (Monthly Review)Document2 pages2010 November (Monthly Review)v_banaru3395No ratings yet

- Stats ExcelDocument8 pagesStats ExcelVaishali NegiNo ratings yet

- Calcular El Periodo de DiseñoDocument14 pagesCalcular El Periodo de DiseñoDANTE MARTINNo ratings yet

- Serial Numbers Vincent BachDocument1 pageSerial Numbers Vincent BachAli Navali ArceNo ratings yet

- Semanas Ventas PMS/N2 PMS/3 1 1850 2 1890 3 1920 1870 4 1950 1905 1887 5 1930 1935 1920 6 1980 1940 1933 7Document2 pagesSemanas Ventas PMS/N2 PMS/3 1 1850 2 1890 3 1920 1870 4 1950 1905 1887 5 1930 1935 1920 6 1980 1940 1933 7CLAUDIA ANDREA AristizabalNo ratings yet

- August 2010 Newsletter Charts - RESDocument2 pagesAugust 2010 Newsletter Charts - RESpsobaniaNo ratings yet

- Newsletter - May 2011 - Charts - CondoDocument2 pagesNewsletter - May 2011 - Charts - CondopsobaniaNo ratings yet

- 2 3 DifferencingDocument58 pages2 3 DifferencingkatakitoNo ratings yet

- Bus 525, AssignmentDocument9 pagesBus 525, AssignmentSamia Mahmud100% (1)

- Lacaste ResidenceDocument3 pagesLacaste Residenceadriann orculloNo ratings yet

- June 2010 MLS Charts ResDocument2 pagesJune 2010 MLS Charts RespsobaniaNo ratings yet

- Intro The Solow Model of GrowthDocument33 pagesIntro The Solow Model of GrowthJuandra Alandi IrdhamNo ratings yet

- October 2010 - Newsletter Charts ResDocument2 pagesOctober 2010 - Newsletter Charts RespsobaniaNo ratings yet

- Constructia de Baraje in RomaniaDocument2 pagesConstructia de Baraje in RomaniaPintilescu CarmenNo ratings yet

- Red River at EmersonDocument21 pagesRed River at EmersonKoert OosterhuisNo ratings yet

- April 2011 Stats For May Newsletter-ConDocument2 pagesApril 2011 Stats For May Newsletter-ConpsobaniaNo ratings yet

- Ps1sol 6218Document25 pagesPs1sol 6218Ashikur RahmanNo ratings yet

- Decibel-Watt (DBW)Document6 pagesDecibel-Watt (DBW)Fetsum LakewNo ratings yet

- Pot Calc1Document3 pagesPot Calc1Anonymous QgauLK2jdnNo ratings yet

- California Population GrowthDocument2 pagesCalifornia Population GrowthsurfviperNo ratings yet

- CabinetDocument4 pagesCabinetNica DellosaNo ratings yet

- Estuaries: A Brief Introduction To Natural and Human-Induced Processes in EstuariesDocument23 pagesEstuaries: A Brief Introduction To Natural and Human-Induced Processes in EstuariesHifza ShahidNo ratings yet

- Solution 9 8Document17 pagesSolution 9 8Kristal Fialho Costa JolyNo ratings yet

- Adobe Scan 20 Jan 2022Document1 pageAdobe Scan 20 Jan 2022Yashwant SahaNo ratings yet

- AE451 Study2 ExcelDocument11 pagesAE451 Study2 ExcelAlptuğ GürNo ratings yet

- Emulsion Multiliir: 1 Jan - 28 Fib19Document2 pagesEmulsion Multiliir: 1 Jan - 28 Fib19harik ReddyNo ratings yet

- The Visual Display of Quantitative Information: Edward R. TufteDocument44 pagesThe Visual Display of Quantitative Information: Edward R. TufteFaam001 FANo ratings yet

- TornoDocument2 pagesTornoJewel Alayon CondinoNo ratings yet

- She Does Not Need To Pay in Both Months. Keep The PHP 5, 500 in The Mean Time.)Document2 pagesShe Does Not Need To Pay in Both Months. Keep The PHP 5, 500 in The Mean Time.)Jewel Alayon CondinoNo ratings yet

- Aluminium and Its AlloysDocument5 pagesAluminium and Its AlloysMax ghNo ratings yet

- Monthly Report: July AA & Nylon 66 Chip Market ReportDocument5 pagesMonthly Report: July AA & Nylon 66 Chip Market ReportNISHSHANKANo ratings yet

- My Woods Revised Price List 14th FebDocument1 pageMy Woods Revised Price List 14th FebAvdhesh Kumar SharmaNo ratings yet

- Vincent Bach Serial No. IndexDocument4 pagesVincent Bach Serial No. IndexДмитро КняжицькийNo ratings yet

- PLN - Environmental Impact Phase Two - OCT 28 2020Document11 pagesPLN - Environmental Impact Phase Two - OCT 28 2020Al-Karim JiwaniNo ratings yet

- Floorplan 3 StoreyDocument1 pageFloorplan 3 StoreyMarielSevillaNo ratings yet

- Mas Anton 1-ATAPDocument1 pageMas Anton 1-ATAPdinodinableNo ratings yet

- Tables & Graphs Writing 1Document8 pagesTables & Graphs Writing 1MistaNo ratings yet

- Slides1 - The Science of MacroDocument17 pagesSlides1 - The Science of Macroalia trikiNo ratings yet

- Cabbage Value Chain Profile: 1. Description of The IndustryDocument26 pagesCabbage Value Chain Profile: 1. Description of The Industryj KiizaNo ratings yet

- Lecture Slides Chap01-1Document27 pagesLecture Slides Chap01-122000492No ratings yet

- 2005-05 CRETACEOUS PETROLEUM SYSTEM - RamirezDocument12 pages2005-05 CRETACEOUS PETROLEUM SYSTEM - RamirezFelix A. RamirezNo ratings yet

- Cat Black 3 Blue Cat White 4 Fiess Dog Brown 2 Giehs Mouse Grey 7 Cat White 4 Huriie Horse White 3 Cow Brown 0 Dog White 7 Mouse Grey 8Document4 pagesCat Black 3 Blue Cat White 4 Fiess Dog Brown 2 Giehs Mouse Grey 7 Cat White 4 Huriie Horse White 3 Cow Brown 0 Dog White 7 Mouse Grey 8Jitendra SoniNo ratings yet

- Figuresand PlatesDocument76 pagesFiguresand PlatesJohn KennedyNo ratings yet

- Bayesian Value-at-Risk and The Capital Charge Puzzle: Matthew Pollard 13th November 2007Document26 pagesBayesian Value-at-Risk and The Capital Charge Puzzle: Matthew Pollard 13th November 2007JonNo ratings yet

- Capital Market Assumptions: Five-Year OutlookDocument11 pagesCapital Market Assumptions: Five-Year OutlookJonNo ratings yet

- The Next Five Years: What Investors Can ExpectDocument52 pagesThe Next Five Years: What Investors Can ExpectJonNo ratings yet

- Forecasting: Francis X. Diebold University of PennsylvaniaDocument323 pagesForecasting: Francis X. Diebold University of PennsylvaniaJonNo ratings yet

- GRC Architects PresentationDocument26 pagesGRC Architects Presentationkhiara asmaeNo ratings yet

- History of The Church in The Philippines 1521 1898 Detailed NotesDocument120 pagesHistory of The Church in The Philippines 1521 1898 Detailed NotesAndrei RefugidoNo ratings yet

- Topic 2 Cultural Diversity PrelimDocument9 pagesTopic 2 Cultural Diversity PrelimRhaven GutierrezNo ratings yet

- The Mystery of Marie RogetDocument48 pagesThe Mystery of Marie Rogetkrisno royNo ratings yet

- Colours in CultureDocument9 pagesColours in CultureMeriam KasraouiNo ratings yet

- Lesson 3 - Transactional and Transformational Leadership - Part 5Document19 pagesLesson 3 - Transactional and Transformational Leadership - Part 5Viet HungNo ratings yet

- Nmmss Andhra PradeshDocument700 pagesNmmss Andhra PradeshGautham NagendraNo ratings yet

- FIELD STUDY 1 E10.1 On Teacher's Philosophy of EducationDocument7 pagesFIELD STUDY 1 E10.1 On Teacher's Philosophy of EducationLeila TaminaNo ratings yet

- Certificate 150579Document1 pageCertificate 150579hmuranjanNo ratings yet

- Ruben Masson-Orta, A025 408 267 (BIA Nov. 9, 2017)Document2 pagesRuben Masson-Orta, A025 408 267 (BIA Nov. 9, 2017)Immigrant & Refugee Appellate Center, LLCNo ratings yet

- Vis.I.8 S.III.344 S.III.344Document15 pagesVis.I.8 S.III.344 S.III.344Than PhyoNo ratings yet

- Rizwan CVDocument8 pagesRizwan CVAnonymous UlojE8No ratings yet

- MI Tinius Olsen MP1200 Manual 2Document8 pagesMI Tinius Olsen MP1200 Manual 2김민근No ratings yet

- Critical Reviews in Oral Biology & Medicine: Cementum and Periodontal Wound Healing and RegenerationDocument12 pagesCritical Reviews in Oral Biology & Medicine: Cementum and Periodontal Wound Healing and RegenerationsevattapillaiNo ratings yet

- Social AuditDocument2 pagesSocial Auditमन्नू लाइसेंसीNo ratings yet

- Career PathDocument2 pagesCareer PathLove GonzalesNo ratings yet

- Fast Lap SequenceDocument1 pageFast Lap SequenceHerik HamzahNo ratings yet

- FIFA World Cup 2010Document3 pagesFIFA World Cup 2010rizwan akhtarNo ratings yet

- IBISWorld Video Games Industry Report PDFDocument48 pagesIBISWorld Video Games Industry Report PDFsangaru raviNo ratings yet

- SSRN Id3594888Document22 pagesSSRN Id3594888Kamal ElhartyNo ratings yet

- Infant ERIKSON: TRUST VS MISTRUSTDocument7 pagesInfant ERIKSON: TRUST VS MISTRUSTMaikel LopezNo ratings yet

- Designing Aluminium CansDocument5 pagesDesigning Aluminium CansAsghar Ali100% (1)

- Multinational Business Finance Assignment 3Document6 pagesMultinational Business Finance Assignment 3AnjnaKandariNo ratings yet

- DLL G6 Tleia Q3 W8Document7 pagesDLL G6 Tleia Q3 W8Jose Pasag ValenciaNo ratings yet

- PWD Service PresentationDocument26 pagesPWD Service PresentationJahid HasnainNo ratings yet

- IV. Data Presentation, Interpretation and AnalysisDocument43 pagesIV. Data Presentation, Interpretation and AnalysisMaykel JekNo ratings yet

- Mergers & Inquisitions - Financial Institutions Group - FIG Investment Banking GuideDocument43 pagesMergers & Inquisitions - Financial Institutions Group - FIG Investment Banking GuideGABRIEL SALONICHIOSNo ratings yet