You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- BUSM4186 AssignmentDocument4 pagesBUSM4186 AssignmentKhánh LyNo ratings yet

- Automobile Industry in BangladeshDocument7 pagesAutomobile Industry in BangladeshnasirNo ratings yet

- Shanta Holdings Limited-PtdDocument13 pagesShanta Holdings Limited-PtdnasirNo ratings yet

- Linde Bangladesh Limited-PtdDocument14 pagesLinde Bangladesh Limited-PtdnasirNo ratings yet

- What Do You Mean by PreventionDocument8 pagesWhat Do You Mean by PreventionnasirNo ratings yet

- Khulna Power Company LTD-PTDDocument10 pagesKhulna Power Company LTD-PTDnasirNo ratings yet

- Berger Paints Bangladesh Limited-PtdDocument15 pagesBerger Paints Bangladesh Limited-PtdnasirNo ratings yet

- Eskayef Pharmaceuticals Limited-PtdDocument25 pagesEskayef Pharmaceuticals Limited-PtdnasirNo ratings yet

- Acme Laboratories Ltd. - Unsolicited-PtdDocument13 pagesAcme Laboratories Ltd. - Unsolicited-PtdnasirNo ratings yet

- M/S Print Point Galaxy: Credit AnalysisDocument3 pagesM/S Print Point Galaxy: Credit AnalysisnasirNo ratings yet

- Performance of Banking Industry: Exhibit 1: Government Initiatives To Support Businesses & Strengthening Banks' LiquidityDocument2 pagesPerformance of Banking Industry: Exhibit 1: Government Initiatives To Support Businesses & Strengthening Banks' LiquiditynasirNo ratings yet

- Impact of Covid 19 On Poultry-FinalDocument6 pagesImpact of Covid 19 On Poultry-FinalnasirNo ratings yet

- The Philippine Financial System FullDocument35 pagesThe Philippine Financial System FullFe ValenciaNo ratings yet

- Managerial Accounting Quiz.1992012172610Document4 pagesManagerial Accounting Quiz.1992012172610Go Turpin0% (1)

- (GLOBAL MKT - GROUP 1) Economic Factors Affecting FPT SoftwareDocument3 pages(GLOBAL MKT - GROUP 1) Economic Factors Affecting FPT SoftwareRCS Nguyễn Tuệ MẫnNo ratings yet

- Emerging Senegal - Dangote New PlantDocument8 pagesEmerging Senegal - Dangote New PlantRohit MotapartiNo ratings yet

- 03 Task Performance 2Document4 pages03 Task Performance 2Ash kaliNo ratings yet

- Balance of Payments WorksheetDocument4 pagesBalance of Payments Worksheetansh yadavNo ratings yet

- HTML 000001Document1 pageHTML 000001NILLOINo ratings yet

- 281 Kainantu Urban Local Level Government 281: Prepared By: Rosita Ben Tubavai A/financial ControllerDocument1 page281 Kainantu Urban Local Level Government 281: Prepared By: Rosita Ben Tubavai A/financial ControllerMichael MotanNo ratings yet

- Presentation 1Document24 pagesPresentation 1waseemniazjatoi100% (1)

- Service Sector Contribution in GDP Country WiseDocument4 pagesService Sector Contribution in GDP Country WisenumlumairNo ratings yet

- Corporate Governance in Real Estate Sector in India Under The Supervision of Prof J.P. SHARMA SONAL NAGPAL (Mcom, Mphil, D.U)Document1 pageCorporate Governance in Real Estate Sector in India Under The Supervision of Prof J.P. SHARMA SONAL NAGPAL (Mcom, Mphil, D.U)Sonal KhuranaNo ratings yet

- Economic Survey 2002-03Document240 pagesEconomic Survey 2002-03raza9871No ratings yet

- Ocean Carriers PresentationDocument12 pagesOcean Carriers PresentationIvaylo VasilevNo ratings yet

- WORLD BANK PresentationDocument30 pagesWORLD BANK PresentationAmna FarooquiNo ratings yet

- Marketing PlanDocument4 pagesMarketing PlanRence Terrado0% (1)

- Topic - China's Push For The Next World Superpower Lit ReviewDocument4 pagesTopic - China's Push For The Next World Superpower Lit Reviewumang tyagiNo ratings yet

- World Bank (IBRD & IDA)Document5 pagesWorld Bank (IBRD & IDA)prankyaquariusNo ratings yet

- Bemis Co Check Date Check Number: VOID - This Is Not A CheckDocument1 pageBemis Co Check Date Check Number: VOID - This Is Not A Checkfreeman p. donNo ratings yet

- International Financial Management PDFDocument134 pagesInternational Financial Management PDFRomelyn PagulayanNo ratings yet

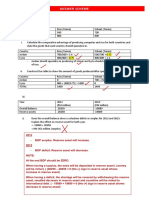

- T7 - Answer Scheme BopDocument5 pagesT7 - Answer Scheme BopAkai GunnerNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument35 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancevaraprasadNo ratings yet

- LÊ NGUYỄN ANH THƠ - preclass 2Document3 pagesLÊ NGUYỄN ANH THƠ - preclass 2Lê Nguyễn Anh ThơNo ratings yet

- Indian Financial System - CIADocument12 pagesIndian Financial System - CIASamar GhorpadeNo ratings yet

- Sino-ASEAN Relations in The Early 21th CenturyDocument16 pagesSino-ASEAN Relations in The Early 21th CenturyKha KhaNo ratings yet

- South Asian Free Trade AgreementDocument44 pagesSouth Asian Free Trade AgreementZeeshan Adeel100% (3)

- Trade Liberalization, Economic Reforms and Foreign Direct Investment - A Critical Analysis of The Political Transformation in VietnamDocument14 pagesTrade Liberalization, Economic Reforms and Foreign Direct Investment - A Critical Analysis of The Political Transformation in VietnamTRn JasonNo ratings yet

- United Kingdom Salary Survey 2010Document64 pagesUnited Kingdom Salary Survey 2010Mohsin MunirNo ratings yet

- Alpesh Raut FINANCIAL CONSULTANT-1-2Document2 pagesAlpesh Raut FINANCIAL CONSULTANT-1-2Alpesh RautNo ratings yet

- Cotton: World Markets and Trade: Record World Consumption Helps Lower Stocks in 2019/20Document29 pagesCotton: World Markets and Trade: Record World Consumption Helps Lower Stocks in 2019/20JigneshSaradavaNo ratings yet