You might also like

- The 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsFrom EverandThe 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsRating: 5 out of 5 stars5/5 (1)

- Making Off Without Payment NotesDocument5 pagesMaking Off Without Payment Notes259bjfcsc9No ratings yet

- Fraud& MisrepresentationDocument8 pagesFraud& MisrepresentationKunaal SaxenaNo ratings yet

- Fraud and Making Off Without Payment: LAW04: Criminal Law (Offences Against Property)Document50 pagesFraud and Making Off Without Payment: LAW04: Criminal Law (Offences Against Property)Moeen AslamNo ratings yet

- Debt Collection: HandbookDocument16 pagesDebt Collection: HandbookMikhael Yah-Shah Dean: Veilour0% (2)

- Fraud and Deceit in Torts ExplainedDocument6 pagesFraud and Deceit in Torts ExplainedLAVANYA SNo ratings yet

- RIVERA, Lyka A. (Assign 4 - Law)Document4 pagesRIVERA, Lyka A. (Assign 4 - Law)Lysss EpssssNo ratings yet

- 02updated Old 2004 OutlineDocument140 pages02updated Old 2004 Outlinemnm222No ratings yet

- Contracts CAN: Winter 2015 - Misrepresentation, Rescission and BarsDocument88 pagesContracts CAN: Winter 2015 - Misrepresentation, Rescission and BarsJjjjmmmmNo ratings yet

- Free Consent (Business Law)Document36 pagesFree Consent (Business Law)Sidra AjmalNo ratings yet

- DeceitDocument15 pagesDeceitAnchita BerryNo ratings yet

- Chap 6 Presentation ScriptDocument3 pagesChap 6 Presentation ScriptThanh TuyềnNo ratings yet

- BP22Document11 pagesBP22Nyl AnerNo ratings yet

- Week 8 - Crimes Against Property - Part 2Document13 pagesWeek 8 - Crimes Against Property - Part 2Angelica PallarcaNo ratings yet

- Teaching DemoDocument28 pagesTeaching DemoJudilyn RavilasNo ratings yet

- Essential Requisites of ContractsDocument16 pagesEssential Requisites of ContractsAmie Jane MirandaNo ratings yet

- Negotiable Instruments Case Digests: Philippine Education Co., Inc. v. Mauricio Soriano FactsDocument4 pagesNegotiable Instruments Case Digests: Philippine Education Co., Inc. v. Mauricio Soriano FactsRem SerranoNo ratings yet

- Week 8 - Estafa - ExplainedDocument7 pagesWeek 8 - Estafa - ExplainedKate Serrano ManlutacNo ratings yet

- WEEK 5 - Contract Part 2Document36 pagesWEEK 5 - Contract Part 2Ts. Mohd Tarmizie MohteeNo ratings yet

- DeceitDocument15 pagesDeceitAnchita BerryNo ratings yet

- Mu 0051Document20 pagesMu 0051Garima SrivastavaNo ratings yet

- Collection Laws From The Federal Trade CommissionDocument4 pagesCollection Laws From The Federal Trade CommissionT100% (3)

- Free Consent at Contract LawDocument22 pagesFree Consent at Contract Lawalsahr100% (3)

- Essay EnglishDocument4 pagesEssay EnglishIsrar AhmadNo ratings yet

- Kle BL M5Document19 pagesKle BL M5pramit04No ratings yet

- FraudDocument7 pagesFraudnhsajibNo ratings yet

- Quick Attack SheetDocument2 pagesQuick Attack SheetBrianStefanovicNo ratings yet

- Free ConsentDocument25 pagesFree ConsentAnooshay100% (1)

- How to stop the IRS with Debt Collection statutesDocument28 pagesHow to stop the IRS with Debt Collection statutesKraft Dinner100% (1)

- FreeconsentDocument43 pagesFreeconsentMaisha SamihaNo ratings yet

- Secured Transactions Outline JDDocument176 pagesSecured Transactions Outline JDJesse Danoff92% (13)

- Debt Collection GuidelineDocument51 pagesDebt Collection GuidelineGregory KagoohaNo ratings yet

- Fraud in ContractsDocument7 pagesFraud in Contractsseshadrimn seshadrimnNo ratings yet

- Making Off Without Payment: S. 3 (1) of T.A. 1978 Provides That: "Subject To Sub-SectionDocument2 pagesMaking Off Without Payment: S. 3 (1) of T.A. 1978 Provides That: "Subject To Sub-SectionMahdi Bin MamunNo ratings yet

- How To Protect Yourself From Debt CollectorsDocument5 pagesHow To Protect Yourself From Debt CollectorsHarvey18100% (2)

- SIT - Bcd1004.lecture5 - VitiatingFactorsDocument37 pagesSIT - Bcd1004.lecture5 - VitiatingFactorsalixirwong99scribdNo ratings yet

- Law of Contract Sa 9 1 21Document40 pagesLaw of Contract Sa 9 1 21Aparna JRNo ratings yet

- LLB 1 Criminal Liability Notes-1Document25 pagesLLB 1 Criminal Liability Notes-1okello peterNo ratings yet

- Gct-2, Law of Torts Saba AlamDocument10 pagesGct-2, Law of Torts Saba AlamSaba AlamNo ratings yet

- Identity Theft WebquestDocument2 pagesIdentity Theft Webquestapi-256420163No ratings yet

- Essential Elements of A Valid ContractDocument13 pagesEssential Elements of A Valid ContractpriamNo ratings yet

- Legal ResearchDocument9 pagesLegal ResearchRon ManNo ratings yet

- Negotiable Instruments LawDocument40 pagesNegotiable Instruments Lawliboanino100% (1)

- Qualified Theft and Estafa JurisprudenceDocument3 pagesQualified Theft and Estafa JurisprudenceGabriel Jhick SaliwanNo ratings yet

- Indian Contract Act, 1872Document110 pagesIndian Contract Act, 1872viky@bcba50% (2)

- Topic: Free Consent: Sub: Business LawDocument22 pagesTopic: Free Consent: Sub: Business LawSHREEYA ARASNo ratings yet

- For UploadDocument5 pagesFor UploadDon CorleoneNo ratings yet

- Misrepresentation: With V O'FlanaganDocument3 pagesMisrepresentation: With V O'Flanagannicole camnasioNo ratings yet

- 1st QuizDocument3 pages1st QuizAlimozaman BuatNo ratings yet

- Legal Environment of Business: Lecture 12 Free Consent by DR Nazrul Islam, Mba, PHD, LLBDocument37 pagesLegal Environment of Business: Lecture 12 Free Consent by DR Nazrul Islam, Mba, PHD, LLBChristine IrvingNo ratings yet

- ObliconDocument3 pagesObliconBorgonia, Khryzlin May C.No ratings yet

- Day 7Document37 pagesDay 7Bhavya JainNo ratings yet

- Wage Garnishment Procedure: Form DC/CV65Document3 pagesWage Garnishment Procedure: Form DC/CV65James neteru100% (2)

- ConsentDocument5 pagesConsentPranav Dev Singh SambyalNo ratings yet

- DECLARATION OF FRAUD AGAINST DEBT COLLECTORSDocument4 pagesDECLARATION OF FRAUD AGAINST DEBT COLLECTORSWesley Barnard100% (2)

- Chapter 13 Bankruptcy in the Western District of TennesseeFrom EverandChapter 13 Bankruptcy in the Western District of TennesseeNo ratings yet

- Civil Law Review 2 - Final ExaminationDocument4 pagesCivil Law Review 2 - Final ExaminationFerdinand PadillaNo ratings yet

- Motion by Riccardo Silva To Compel Reddit To Provide Any Identifying InformationDocument21 pagesMotion by Riccardo Silva To Compel Reddit To Provide Any Identifying InformationChefs Best Statements - NewsNo ratings yet

- PICOP vs. AsuncionDocument16 pagesPICOP vs. Asuncionalwayskeepthefaith8No ratings yet

- Supplemental Judicial AffidavitDocument3 pagesSupplemental Judicial AffidavitSarj Luzon100% (2)

- Understanding Executor Office and Use of The Executor Letter 10.28.10Document24 pagesUnderstanding Executor Office and Use of The Executor Letter 10.28.10colin879098% (44)

- Sca Case DigestDocument2 pagesSca Case DigestpiaNo ratings yet

- 10 CDDocument2 pages10 CDLyn Dela Cruz DumoNo ratings yet

- Nollora vs. PeopleDocument4 pagesNollora vs. PeopleAngelica DavidNo ratings yet

- People VS William ChingDocument1 pagePeople VS William ChingKristine Guia CastilloNo ratings yet

- Court Visit ReportDocument2 pagesCourt Visit ReportSUDIP MONDALNo ratings yet

- 8.lanuza vs. BF CorpDocument7 pages8.lanuza vs. BF CorpRomy IanNo ratings yet

- RUPA vs CA Agricultural Tenancy DisputeDocument4 pagesRUPA vs CA Agricultural Tenancy DisputeEmmanuel OrtegaNo ratings yet

- People Vs VillarDocument2 pagesPeople Vs VillaroabeljeanmoniqueNo ratings yet

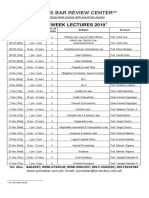

- 2019 Schedule of Preweek LecturesDocument1 page2019 Schedule of Preweek LecturesVioletNo ratings yet

- (Appendix IV Form No. 1Document23 pages(Appendix IV Form No. 1Rajshree GuptaNo ratings yet

- Ayala Alabang land sale disputeDocument10 pagesAyala Alabang land sale disputeulticonNo ratings yet

- United States Court of Appeals, Tenth CircuitDocument5 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- In Re: Tax Refund Litigation. Barrister Associates, Paul Belloff, Robert Gold, Parliament Securities Corp., Irving Cohen, Madison Library, Inc., Universal Publishing Resources, Ltd. And Geoffrey Townsend, Ltd., (Re: 90-6015), Irving Cohen, Paul Belloff and Robert Gold, (Re: 90-6015), Cross-Appellants (Re: 90-6033) v. United States of America, (Re: 90-6015), Cross-Appellee (Re: 90-6033), 915 F.2d 58, 2d Cir. (1990)Document3 pagesIn Re: Tax Refund Litigation. Barrister Associates, Paul Belloff, Robert Gold, Parliament Securities Corp., Irving Cohen, Madison Library, Inc., Universal Publishing Resources, Ltd. And Geoffrey Townsend, Ltd., (Re: 90-6015), Irving Cohen, Paul Belloff and Robert Gold, (Re: 90-6015), Cross-Appellants (Re: 90-6033) v. United States of America, (Re: 90-6015), Cross-Appellee (Re: 90-6033), 915 F.2d 58, 2d Cir. (1990)Scribd Government DocsNo ratings yet

- China Banking V CiarcoDocument3 pagesChina Banking V CiarcoTeresa CardinozaNo ratings yet

- Due Diligence Abuse Violations by Unqualified LawyersDocument2 pagesDue Diligence Abuse Violations by Unqualified LawyersSTILAS Board of Supervising AttorneysNo ratings yet

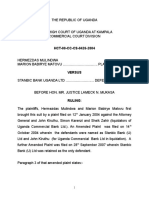

- Hermezdas Mulindwa Vs Stanbic BankDocument18 pagesHermezdas Mulindwa Vs Stanbic BankKellyNo ratings yet

- Rynearson v. Ferguson Et Al First Amendment CyberstalkingDocument8 pagesRynearson v. Ferguson Et Al First Amendment Cyberstalkingchristopher kingNo ratings yet

- Ecthr 2006 Becciev Vs MoldovaDocument25 pagesEcthr 2006 Becciev Vs MoldovanicoletttaNo ratings yet

- CARP Coverage Protest - Heirs of Ramiro JocsonDocument5 pagesCARP Coverage Protest - Heirs of Ramiro JocsonKara Gonzaga Cuarom100% (1)

- Lyceum Philippines University: College of LawDocument3 pagesLyceum Philippines University: College of LawSusannie AcainNo ratings yet

- Standard Data Protection Clauses IDTADocument36 pagesStandard Data Protection Clauses IDTAandres.rafael.carrenoNo ratings yet

- Aratuc v. COMELECDocument30 pagesAratuc v. COMELECAlvin ComilaNo ratings yet

- STAY - SC OrderDocument3 pagesSTAY - SC OrdermvsarmaNo ratings yet

- Additional DigestDocument7 pagesAdditional DigestMel Manatad100% (1)

- ContractsDocument6 pagesContractsOnofre Algara Jr.No ratings yet