You might also like

- The Essential Guide To Using Poetry in The Classroom at Key Stages 1 and 2Document19 pagesThe Essential Guide To Using Poetry in The Classroom at Key Stages 1 and 2Anna MurrayNo ratings yet

- Fabulae LatinaeDocument148 pagesFabulae Latinaeremitens5810No ratings yet

- US Stock Bond CorrelationDocument24 pagesUS Stock Bond CorrelationSabyasachi MukherjeeNo ratings yet

- ReflectionDocument11 pagesReflectionVenunadhan B. PillaiNo ratings yet

- Marcellus LittleChamps PresentationDocument15 pagesMarcellus LittleChamps PresentationPawan ShroffNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaNo ratings yet

- Nursing Association of The Philippines - OARGADocument56 pagesNursing Association of The Philippines - OARGAMatelyn Oarga100% (1)

- Decentralization and Local GovernanceDocument31 pagesDecentralization and Local GovernanceNirwa-Gagha Lika100% (1)

- Marcellus Little-Champs PresentationDocument17 pagesMarcellus Little-Champs PresentationqwertyNo ratings yet

- Marcellus Little-Champs PresentationDocument18 pagesMarcellus Little-Champs PresentationSuyash BhiseNo ratings yet

- Marcellus Little-Champs Presentation DIRECTDocument19 pagesMarcellus Little-Champs Presentation DIRECTBijoy RaghavanNo ratings yet

- March-2022 Marcellus - Little-Champs - Presentation - DIRECTDocument19 pagesMarch-2022 Marcellus - Little-Champs - Presentation - DIRECTAGNo ratings yet

- Marcellus Little Champs Presentation June-2023 Final RegularDocument18 pagesMarcellus Little Champs Presentation June-2023 Final RegularSaikat HalderNo ratings yet

- Ambit Good & Clean Smallcap Fund (Emerging Giants) : Portfolio Management ServicesDocument26 pagesAmbit Good & Clean Smallcap Fund (Emerging Giants) : Portfolio Management ServicesSaurabh MukherjeeNo ratings yet

- Marcellus Rising Giants PMS June-2023 Direct Final CompressedDocument23 pagesMarcellus Rising Giants PMS June-2023 Direct Final Compressed123bingoNo ratings yet

- Marcellus Rising-Giants-PMS Direct 10dec21Document21 pagesMarcellus Rising-Giants-PMS Direct 10dec21maina00000No ratings yet

- Marcellus RisingGiants PMS DirectDocument23 pagesMarcellus RisingGiants PMS Directajay huddaNo ratings yet

- Sip Presentation - May 2020Document40 pagesSip Presentation - May 2020DBCGNo ratings yet

- Personal Financial Planning: End-Term ProjectDocument12 pagesPersonal Financial Planning: End-Term ProjectPoloJ20No ratings yet

- Marcellus Rising Giants PMS July-2023 Direct Final-1Document23 pagesMarcellus Rising Giants PMS July-2023 Direct Final-1Vaman ShenoyNo ratings yet

- Marcellus RisingGiants PMS Direct 230223 061127Document24 pagesMarcellus RisingGiants PMS Direct 230223 061127IndeevarBhattNo ratings yet

- Marcellus Rising Giants PMS: JANUARY 2022Document21 pagesMarcellus Rising Giants PMS: JANUARY 2022Devraj DashNo ratings yet

- Embrace Your Stereotype - Definitive Growth Equity Guide For The Rest of 2020Document16 pagesEmbrace Your Stereotype - Definitive Growth Equity Guide For The Rest of 2020OliverNo ratings yet

- Aptus Housing Finance LTD: SubscribeDocument5 pagesAptus Housing Finance LTD: SubscribeupsahuNo ratings yet

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- IDFC Factsheet November 2020Document62 pagesIDFC Factsheet November 2020dali faceNo ratings yet

- Leaflet Flexi Cap FundDocument4 pagesLeaflet Flexi Cap FundBhaskar Reddy NvsNo ratings yet

- Quarterly: Third Quarter of 2021Document71 pagesQuarterly: Third Quarter of 2021ForkNo ratings yet

- Taking Stock Quarterly Outlook en UsDocument4 pagesTaking Stock Quarterly Outlook en UsjayeshNo ratings yet

- RamSync BriefDocument5 pagesRamSync Briefjoshua arnettNo ratings yet

- For Those Who Play To Win.: Midcap Fund Midcap FundDocument4 pagesFor Those Who Play To Win.: Midcap Fund Midcap FundABCNo ratings yet

- Canara Robeco Emerging Equities: For Private CirculationDocument1 pageCanara Robeco Emerging Equities: For Private CirculationAadeesh JainNo ratings yet

- A Pair That Can Take You To Your Goal!: HDFC Large and Mid Cap FundDocument21 pagesA Pair That Can Take You To Your Goal!: HDFC Large and Mid Cap FundflplopaNo ratings yet

- ED+ Factsheet JuneDocument1 pageED+ Factsheet JunejagsNo ratings yet

- SageOne Investor Memo May 2021Document10 pagesSageOne Investor Memo May 2021Harsh AgrawalNo ratings yet

- Solid, Stable and Consistent: BOC Hong Kong (Holdings) LimitedDocument4 pagesSolid, Stable and Consistent: BOC Hong Kong (Holdings) LimitedRalph SuarezNo ratings yet

- Capital Growth FundDocument1 pageCapital Growth FundHimanshu AgrawalNo ratings yet

- Old Mutual Core Balanced FundDocument2 pagesOld Mutual Core Balanced FundSam AbdurahimNo ratings yet

- Navin Agarwal Article Sep 2021Document5 pagesNavin Agarwal Article Sep 2021Smeet GopaniNo ratings yet

- ALCHEMY - High Growth PMSDocument23 pagesALCHEMY - High Growth PMSgaurang29No ratings yet

- QED Capital Advisors LLP Annual Letter 2018 19 PDFDocument5 pagesQED Capital Advisors LLP Annual Letter 2018 19 PDFpurav31No ratings yet

- Welspun Enterprises LTD - Investor Presentation - 2Document36 pagesWelspun Enterprises LTD - Investor Presentation - 2Dwijendra ChanumoluNo ratings yet

- Invest in Mid Cap Fund - UTI Equity Mutual FundsDocument2 pagesInvest in Mid Cap Fund - UTI Equity Mutual FundsRinku MishraNo ratings yet

- A Review Post Global Credit Crisis: Indian NBFC SectorDocument6 pagesA Review Post Global Credit Crisis: Indian NBFC SectorsauravNo ratings yet

- Collective Insights: Minutes From Our Morning MeetingDocument2 pagesCollective Insights: Minutes From Our Morning Meetingapi-63645244No ratings yet

- Bonsai q2 2022 - XpelDocument9 pagesBonsai q2 2022 - XpelGeoffreyNo ratings yet

- SageOne Investor Memo May 2023Document9 pagesSageOne Investor Memo May 2023debarkaNo ratings yet

- Fujifilm VISION 2030Document7 pagesFujifilm VISION 2030FujiRumorsNo ratings yet

- AMBITGOOD&CLEAN - Midcap PMS - Jan - 2022 - PresentationDocument24 pagesAMBITGOOD&CLEAN - Midcap PMS - Jan - 2022 - Presentationbeza manojNo ratings yet

- Vanguard Global Stock Index FundDocument4 pagesVanguard Global Stock Index FundjorgeperezsidecarshotmailomNo ratings yet

- Bond Yields and Prices: Reference: Chapter 17Document30 pagesBond Yields and Prices: Reference: Chapter 17RosaNo ratings yet

- 4Q 2020 - Analyst Meeting (LONG FORM)Document80 pages4Q 2020 - Analyst Meeting (LONG FORM)Giang NguyenNo ratings yet

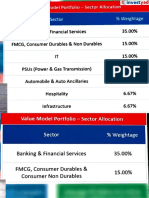

- Inf Power Fact Sheet Dec 2022Document3 pagesInf Power Fact Sheet Dec 2022GufranNo ratings yet

- MFin Employment Report - 2021FT - 2022INT - 1Document8 pagesMFin Employment Report - 2021FT - 2022INT - 1Zack ZhangNo ratings yet

- NIOF-Dec 2020Document1 pageNIOF-Dec 2020chqaiserNo ratings yet

- Finance Report MarketingDocument16 pagesFinance Report MarketingLKNo ratings yet

- AUSmall FinancebanklimitedDocument39 pagesAUSmall FinancebanklimitedDIPAN BISWASNo ratings yet

- Macro Investing, New Recommendations & More... : in This ReportDocument12 pagesMacro Investing, New Recommendations & More... : in This ReportPIYUSH GOPALNo ratings yet

- IDFC FIRST Bank Investor Presentation Q3 FY24Document111 pagesIDFC FIRST Bank Investor Presentation Q3 FY24Akash ingaleshwarNo ratings yet

- OMAlbaraka Equity FundDocument2 pagesOMAlbaraka Equity FundArdine FickNo ratings yet

- GS Global Macro ReportDocument26 pagesGS Global Macro ReportRyanNo ratings yet

- 2point2 Capital - Investor Update Q4 FY20Document6 pages2point2 Capital - Investor Update Q4 FY20Rakesh PandeyNo ratings yet

- Purple Style LabsDocument22 pagesPurple Style LabsRishav BothraNo ratings yet

- Bajaj Electrical - ARA - Ambit - Aug 2018 PDFDocument25 pagesBajaj Electrical - ARA - Ambit - Aug 2018 PDFADNo ratings yet

- Morgan Stanley Q4 2021 Strategic UpdateDocument21 pagesMorgan Stanley Q4 2021 Strategic UpdateZerohedgeNo ratings yet

- Valuation Policy For The Schemes of Motilal Oswal Mutual FundDocument1 pageValuation Policy For The Schemes of Motilal Oswal Mutual Fundsubham mohantyNo ratings yet

- Happiest Minds TechnologiesLtd IPO NOTE07092020Document7 pagesHappiest Minds TechnologiesLtd IPO NOTE07092020subham mohantyNo ratings yet

- Economy Watch - December 2020Document29 pagesEconomy Watch - December 2020subham mohantyNo ratings yet

- Portfolio Make StrategyDocument16 pagesPortfolio Make Strategysubham mohantyNo ratings yet

- Ramdeo Agarwal 10 PhilosophyDocument22 pagesRamdeo Agarwal 10 Philosophysubham mohanty100% (1)

- April Mutual Fund ReportDocument34 pagesApril Mutual Fund Reportsubham mohantyNo ratings yet

- UGB160 On-Campus Assessment Brief 2020-21Document9 pagesUGB160 On-Campus Assessment Brief 2020-21Hasan MahmoodNo ratings yet

- Richard Kitchener - Genetic Epistemology, Normative Epistemology, and PsychologismDocument25 pagesRichard Kitchener - Genetic Epistemology, Normative Epistemology, and PsychologismIva ShaneNo ratings yet

- Tle 6 Ict Week5 TGDocument19 pagesTle 6 Ict Week5 TGSunshine Lou BarcenasNo ratings yet

- Uq Assignment Cover SheetDocument4 pagesUq Assignment Cover Sheetewagq2yb100% (1)

- Comparison of Mortality Predictive Scoring Systems in Picu PatientsDocument32 pagesComparison of Mortality Predictive Scoring Systems in Picu Patientszeeshan yahooNo ratings yet

- Template For Phil Iri Pre Test 2019Document13 pagesTemplate For Phil Iri Pre Test 2019Kim Bautista MallariNo ratings yet

- SP-2 Project Report (18-219)Document21 pagesSP-2 Project Report (18-219)Kranthi VarmaNo ratings yet

- Biology Thesis ExampleDocument7 pagesBiology Thesis Examplejessicamyerseugene100% (2)

- Icebreaker Rationale StatementDocument2 pagesIcebreaker Rationale Statementapi-386092719No ratings yet

- 50 Kunci Soal Grammar Latihan Untuk Mahasiswa Semester AwalDocument4 pages50 Kunci Soal Grammar Latihan Untuk Mahasiswa Semester AwalayuvanaNo ratings yet

- 30 S. 2017Document7 pages30 S. 2017MaryroseNo ratings yet

- Alien Language Intermediate 47Document1 pageAlien Language Intermediate 47Carolina Jasso GNo ratings yet

- SMTDocument42 pagesSMTMirjana PrekovicNo ratings yet

- FedVTE Training CatalogDocument25 pagesFedVTE Training CatalogtallknightNo ratings yet

- Women Leadership Development TrainingDocument6 pagesWomen Leadership Development TrainingInterweave consultingNo ratings yet

- Mathematics in The Modern World - Course GuideDocument6 pagesMathematics in The Modern World - Course GuideRichard BacharNo ratings yet

- Anecdotal RecordsDocument3 pagesAnecdotal RecordsCherry DomingoNo ratings yet

- Iitm Spoc Wkshop PPT 01Document33 pagesIitm Spoc Wkshop PPT 01Balaji VenkataramanNo ratings yet

- B.A. III - Old Annual Pattern SyllabusDocument22 pagesB.A. III - Old Annual Pattern Syllabusprantik banerjeeNo ratings yet

- Brief Summary of Liminal Thinking 1 0Document7 pagesBrief Summary of Liminal Thinking 1 0Mayank SahuNo ratings yet

- Panjab UniversityDocument200 pagesPanjab UniversityAnkur KatariaNo ratings yet

- Nguyễn Thị Hương Giang Unit 1: Chemistry And Its BranchesDocument3 pagesNguyễn Thị Hương Giang Unit 1: Chemistry And Its BranchesGiang Nguyen Thi HuongNo ratings yet

- Cambridge PHD Thesis GuidelinesDocument7 pagesCambridge PHD Thesis Guidelinessuegangulifargo100% (3)

- Category Certifications Courses/Professional DegreeDocument5 pagesCategory Certifications Courses/Professional DegreeitssandypotterNo ratings yet

- Consolidation2021 2022Document3 pagesConsolidation2021 2022Joan Jambalos TuertoNo ratings yet