You might also like

- Brokerage Business PlanDocument19 pagesBrokerage Business PlanMuhammad Ahmed50% (4)

- Absolute Deed of SaleDocument3 pagesAbsolute Deed of SaleNN DDL67% (3)

- Contoh Latihan SoalDocument6 pagesContoh Latihan SoalfidelaluthfianaNo ratings yet

- Intermediate Accounting Chapter 9 SolutionsDocument40 pagesIntermediate Accounting Chapter 9 SolutionsNatazia Ibañez80% (5)

- P4-12 AnswerDocument5 pagesP4-12 AnswerPutri Apriliana100% (1)

- Stocks 131-135Document3 pagesStocks 131-135Rej Patnaan100% (1)

- P11Document7 pagesP11Arif RahmanNo ratings yet

- CH16Document80 pagesCH16mahinNo ratings yet

- Ex Ch.15Document2 pagesEx Ch.15kenny 322016048No ratings yet

- Rika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02Document5 pagesRika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02MARCHO AGUSTANo ratings yet

- ACCT550 Homework Week 2Document5 pagesACCT550 Homework Week 2Natasha Declan100% (2)

- Internal Control Review - The Practical Approach - Group 2Document14 pagesInternal Control Review - The Practical Approach - Group 2Tiara Indah SariNo ratings yet

- Working 3Document6 pagesWorking 3Hà Lê DuyNo ratings yet

- Chapter 7 Problem 7.3 Nathali, Jeffrey, TasyaDocument6 pagesChapter 7 Problem 7.3 Nathali, Jeffrey, Tasyavtech netNo ratings yet

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- Wiley - Chapter 6: Accounting and The Time Value of MoneyDocument26 pagesWiley - Chapter 6: Accounting and The Time Value of MoneyIvan Bliminse100% (1)

- Chapter 16 Homework SolutionsDocument11 pagesChapter 16 Homework Solutionsyuri100% (2)

- Soal - Home Office Vs Branch (40%) : Total Informasi TambahanDocument2 pagesSoal - Home Office Vs Branch (40%) : Total Informasi Tambahanshani100% (1)

- KUNCI INDOGAWAI Ekuitas2015Document30 pagesKUNCI INDOGAWAI Ekuitas2015ELISABET NOVITASARI SINAGA100% (2)

- E7 25Document2 pagesE7 25Muhammad Syafiq RamadhanNo ratings yet

- Ch.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesDocument7 pagesCh.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesFaishal Alghi FariNo ratings yet

- Comprehensive Problems Solution Answer Key Mid TermDocument5 pagesComprehensive Problems Solution Answer Key Mid TermGabriel Aaron DionneNo ratings yet

- Soal Chapter 17Document6 pagesSoal Chapter 17Baiq Melaty Sepsa WindiNo ratings yet

- Tugas Latihan Soal EPSDocument4 pagesTugas Latihan Soal EPSNaoya FaldinyNo ratings yet

- 2.1 TOEFL - Reading.Strategy - Updated PDFDocument4 pages2.1 TOEFL - Reading.Strategy - Updated PDFboyssss88No ratings yet

- 2.5 Basic-List-Of-Word-Roots PDFDocument3 pages2.5 Basic-List-Of-Word-Roots PDFboyssss88No ratings yet

- PSECU Membership ApplicationDocument2 pagesPSECU Membership ApplicationdrewscribblerNo ratings yet

- Evidence Plan: Bookkeeping Nciii Page 1 of 2Document2 pagesEvidence Plan: Bookkeeping Nciii Page 1 of 2Roy SumugatNo ratings yet

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsan100% (1)

- Akuntansi BiayaDocument18 pagesAkuntansi BiayaMlfffNo ratings yet

- Akuntansi Keuangan Lanjutan 2Document6 pagesAkuntansi Keuangan Lanjutan 2Marselinus Aditya Hartanto TjungadiNo ratings yet

- AEB15 SM C18 v3Document33 pagesAEB15 SM C18 v3Aaqib Hossain100% (1)

- Tugas 5 (Soal) Auditing IIDocument6 pagesTugas 5 (Soal) Auditing IIrahmat idrusNo ratings yet

- Exercise 6Document1 pageExercise 6Kayla SheltonNo ratings yet

- Arini Alfahani - Tugas AKM IDocument2 pagesArini Alfahani - Tugas AKM Iarini alfahaniNo ratings yet

- Tugas Pertemuan 13 - Alya Sufi Ikrima - 041911333248Document3 pagesTugas Pertemuan 13 - Alya Sufi Ikrima - 041911333248Alya Sufi IkrimaNo ratings yet

- Bonds Yields and Prices, Ni Kadek WahyuniDocument5 pagesBonds Yields and Prices, Ni Kadek WahyuniWahyuni MertasariNo ratings yet

- CH 8Document13 pagesCH 8doc nurfatkhiyahNo ratings yet

- 12.1. Match The Term in The Left Column With Its Definition in The Right ColumnDocument1 page12.1. Match The Term in The Left Column With Its Definition in The Right ColumnNguyễn HồngNo ratings yet

- Soal Teori:: Petunjuk: Kerjakan SOAL TEORI Dan SOAL PRAKTIKA Pada Kolom Jawaban Yang Tersedia !!Document6 pagesSoal Teori:: Petunjuk: Kerjakan SOAL TEORI Dan SOAL PRAKTIKA Pada Kolom Jawaban Yang Tersedia !!irma purnama ningrumNo ratings yet

- KuisDocument11 pagesKuismc2hin9No ratings yet

- Jawaban Debt Investments (Mindmap, E17-1 p17-1)Document2 pagesJawaban Debt Investments (Mindmap, E17-1 p17-1)Rahmat DarmawanNo ratings yet

- Tugas CH 8 Dan 9Document13 pagesTugas CH 8 Dan 9muhammad alfariziNo ratings yet

- Tugas Materi KewajibanDocument2 pagesTugas Materi Kewajibansavira andayani0% (1)

- Chapter 6 and 7 NR and BPDocument2 pagesChapter 6 and 7 NR and BPCa Ada100% (1)

- Accounting For Derivatives and Hedging Activities: Answers To QuestionsDocument22 pagesAccounting For Derivatives and Hedging Activities: Answers To QuestionsGabyVionidyaNo ratings yet

- Firda Arfianti - LC53 - Equity Method, Two Consecutive YearsDocument5 pagesFirda Arfianti - LC53 - Equity Method, Two Consecutive YearsFirdaNo ratings yet

- Uts - Akm3 - Suci Purnama Devi - F0318108 - E17.9 & P21.13 PDFDocument4 pagesUts - Akm3 - Suci Purnama Devi - F0318108 - E17.9 & P21.13 PDFSuci Purnama Devi100% (1)

- KuisDocument22 pagesKuismc2hin9100% (1)

- Delaney Company Leases An Automobile With A Fair Value of 10000Document4 pagesDelaney Company Leases An Automobile With A Fair Value of 10000Kailash KumarNo ratings yet

- Preliminary ComputationsDocument3 pagesPreliminary ComputationsFarrell DmNo ratings yet

- Latsol AklDocument10 pagesLatsol AklAlya Sufi IkrimaNo ratings yet

- Test 2 HomeworkDocument12 pagesTest 2 HomeworkMiguel CortezNo ratings yet

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsanNo ratings yet

- IFRS Edition-2nd: Conceptual Framework For Financial ReportingDocument30 pagesIFRS Edition-2nd: Conceptual Framework For Financial ReportingAhmed SroorNo ratings yet

- Kasus Chapter 4.answerDocument3 pagesKasus Chapter 4.answermadesugandhiNo ratings yet

- Kelompok 6 Soal 12-8Document2 pagesKelompok 6 Soal 12-8clalalacNo ratings yet

- ACY4001 Individual Assignment 2 SolutionsDocument7 pagesACY4001 Individual Assignment 2 SolutionsMorris LoNo ratings yet

- Soal Ab1 (Tm-1) Cost ConceptDocument5 pagesSoal Ab1 (Tm-1) Cost ConceptAntonius Sugi SuhartonoNo ratings yet

- Completed Contract - Casper Co.-ProblemDocument2 pagesCompleted Contract - Casper Co.-ProblemEllyza Serrano100% (1)

- Calculus Company Makes Calculators For StudentsDocument2 pagesCalculus Company Makes Calculators For StudentsElliot RichardNo ratings yet

- Tugas 10Document3 pagesTugas 10Reyhan ArioNo ratings yet

- Quiz - Inter 2 UTS - Wo AnsDocument3 pagesQuiz - Inter 2 UTS - Wo AnsNike HannaNo ratings yet

- GBE AssignmentDocument4 pagesGBE AssignmentOlga KanashinaNo ratings yet

- 7.1 RoaDocument5 pages7.1 Roashana wolfNo ratings yet

- Limited Liability QA IGCSEDocument47 pagesLimited Liability QA IGCSEKhalilNo ratings yet

- Jawaban Soal - Vita Nur AryatiDocument4 pagesJawaban Soal - Vita Nur AryatiVita Nur AryatiNo ratings yet

- SPJAT SAMPLE PAPER No 2Document13 pagesSPJAT SAMPLE PAPER No 2Vita Nur AryatiNo ratings yet

- SPJAT SAMPLE PAPER No 1Document15 pagesSPJAT SAMPLE PAPER No 1Vita Nur AryatiNo ratings yet

- Spjat Sample Paper No 3Document13 pagesSpjat Sample Paper No 3Vita Nur AryatiNo ratings yet

- Reasons Why Students Don't Do Well On Multiple Choice TestsDocument1 pageReasons Why Students Don't Do Well On Multiple Choice TestsVita Nur AryatiNo ratings yet

- 16b35db47f2018293ba74320817a750eDocument19 pages16b35db47f2018293ba74320817a750eVita Nur AryatiNo ratings yet

- 16b35db47f2018293ba74320817a750eDocument19 pages16b35db47f2018293ba74320817a750eVita Nur AryatiNo ratings yet

- Myanma Foreign Trade Bank: Head OfficeDocument1 pageMyanma Foreign Trade Bank: Head OfficeVita Nur AryatiNo ratings yet

- Myanma Foreign Trade Bank: Head OfficeDocument1 pageMyanma Foreign Trade Bank: Head OfficeVita Nur AryatiNo ratings yet

- Citra True FinalDocument34 pagesCitra True FinalfranciskaNo ratings yet

- Letter To Cancel or Withdraw A Customer's Credit AccountDocument1 pageLetter To Cancel or Withdraw A Customer's Credit AccountVita Nur AryatiNo ratings yet

- Excel FunctionsDocument5 pagesExcel FunctionsVita Nur AryatiNo ratings yet

- FAQs On Entity Master 1Document13 pagesFAQs On Entity Master 1Shinil NambrathNo ratings yet

- Account Management & Client Services: Ashita Gupta 13PGDM136Document71 pagesAccount Management & Client Services: Ashita Gupta 13PGDM136Karan GuptaNo ratings yet

- Mutual Funds in IndiaDocument8 pagesMutual Funds in IndiaSimardeep SinghNo ratings yet

- ToaDocument80 pagesToaJuvy Dimaano100% (1)

- Trading NR7 SetupDocument24 pagesTrading NR7 SetupQuyên NguyễnNo ratings yet

- Aurora TextilesDocument14 pagesAurora TextilesYale Brendan CatabayNo ratings yet

- Housing Choice Voucher Payments ContractBody of Contract Part B 52641Document12 pagesHousing Choice Voucher Payments ContractBody of Contract Part B 52641shaundirelemonde100% (1)

- CRISIL Certificate Programme On Working Capital Appraisal and Monitoring Sept 2017Document4 pagesCRISIL Certificate Programme On Working Capital Appraisal and Monitoring Sept 2017rooptejaNo ratings yet

- ACCTG 16 FAR W2 Problems Part 2 PDFDocument6 pagesACCTG 16 FAR W2 Problems Part 2 PDFLabLab ChattoNo ratings yet

- Fatemi2017 PDFDocument65 pagesFatemi2017 PDFRichard AndersonNo ratings yet

- Philippine Society of Mechanical Engineers: To: Ferdinand B. Sales, DirectorDocument2 pagesPhilippine Society of Mechanical Engineers: To: Ferdinand B. Sales, DirectorJImlan Sahipa IsmaelNo ratings yet

- Euro MarketDocument35 pagesEuro MarketPari GanganNo ratings yet

- Appointment - LetterDocument3 pagesAppointment - LetteraarifNo ratings yet

- Mileage Allowance Rates 2011Document2 pagesMileage Allowance Rates 2011Fuzzy_Wood_PersonNo ratings yet

- Three Simple Ideas Ifrs17 IdDocument12 pagesThree Simple Ideas Ifrs17 IdNOCINPLUSNo ratings yet

- Q S Log Book KenyaDocument25 pagesQ S Log Book KenyaswazsurvNo ratings yet

- BPI Vs CA DigestDocument2 pagesBPI Vs CA DigestXyraKrezelGajeteNo ratings yet

- Cost Terminology and Cost BehaviorsDocument2 pagesCost Terminology and Cost BehaviorsNicole Anne Santiago SibuloNo ratings yet

- Practice Final Bus331 Spring2023Document2 pagesPractice Final Bus331 Spring2023Javan OdephNo ratings yet

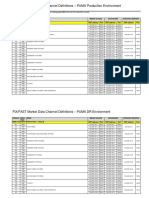

- FIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentDocument3 pagesFIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentVaibhav PoddarNo ratings yet

- IB Chapter # 12Document22 pagesIB Chapter # 12Ma Quang ThinhNo ratings yet

- QChartist Highly Profitable Trading SystemsDocument23 pagesQChartist Highly Profitable Trading SystemsJulien MoogNo ratings yet

- Tito Nanding 2015Document8 pagesTito Nanding 2015Hanabishi RekkaNo ratings yet

- MODULE 1 Overview of EntrepreneurshipDocument32 pagesMODULE 1 Overview of Entrepreneurshipjulietpamintuan100% (11)

- CalPERS Portfolio DataDocument34 pagesCalPERS Portfolio DataFortuneNo ratings yet

- Workbook PDFDocument116 pagesWorkbook PDFSuvodeep GhoshNo ratings yet