You might also like

- Week 2Document21 pagesWeek 2IDKNo ratings yet

- Cash Return on Capital Invested: Ten Years of Investment Analysis with the CROCI Economic Profit ModelFrom EverandCash Return on Capital Invested: Ten Years of Investment Analysis with the CROCI Economic Profit ModelRating: 5 out of 5 stars5/5 (3)

- B220 - MI01 - Lecture NotesDocument37 pagesB220 - MI01 - Lecture NotesLIN XIAOLINo ratings yet

- Unit 1 Exam Review Packet-RevisedDocument6 pagesUnit 1 Exam Review Packet-RevisedNoelia OliveroNo ratings yet

- Limits Alternatives and Choices PDFDocument7 pagesLimits Alternatives and Choices PDFRachelle EscanoNo ratings yet

- #1 Introduction To Economics - 2020Document30 pages#1 Introduction To Economics - 2020Rachmad AriefNo ratings yet

- Economics Today The Micro 17th Edition Roger Leroy Miller Solutions ManualDocument25 pagesEconomics Today The Micro 17th Edition Roger Leroy Miller Solutions ManualDiamondSmithoawky100% (61)

- Theme 1.1 Scarcity As The Central Economic Problem Part 1 PDFDocument26 pagesTheme 1.1 Scarcity As The Central Economic Problem Part 1 PDFhajuNo ratings yet

- Economics Today The Macro 17th Edition Roger Leroy Miller Solutions ManualDocument25 pagesEconomics Today The Macro 17th Edition Roger Leroy Miller Solutions ManualDianaFloresfowc100% (57)

- Economics IntroductionDocument15 pagesEconomics IntroductionShiv BaghelNo ratings yet

- Economics Today The Micro 17th Edition Roger Leroy Miller Solutions ManualDocument13 pagesEconomics Today The Micro 17th Edition Roger Leroy Miller Solutions Manualroyhilda0zccp100% (11)

- Dwnload Full Economics Today The Micro 17th Edition Roger Leroy Miller Solutions Manual PDFDocument36 pagesDwnload Full Economics Today The Micro 17th Edition Roger Leroy Miller Solutions Manual PDFirisybarrous100% (9)

- Dwnload Full Economics Today The Macro 17th Edition Roger Leroy Miller Solutions Manual PDFDocument35 pagesDwnload Full Economics Today The Macro 17th Edition Roger Leroy Miller Solutions Manual PDFdavidhughestxxs100% (11)

- Economics Today The Macro 17th Edition Roger Leroy Miller Solutions ManualDocument35 pagesEconomics Today The Macro 17th Edition Roger Leroy Miller Solutions Manualroyhilda0zccp100% (30)

- Basic Microeconomics ReviewerDocument11 pagesBasic Microeconomics Reviewerjeon jungkookNo ratings yet

- Chapter 1Document22 pagesChapter 1Farah FarhathunNo ratings yet

- Applied Economics Reviewer 1ST Quarter PDFDocument16 pagesApplied Economics Reviewer 1ST Quarter PDFZack FairNo ratings yet

- The Economic Problem-Assoc Prof SaidatulakmalDocument23 pagesThe Economic Problem-Assoc Prof SaidatulakmalTulasmi, SEINo ratings yet

- Unit 1Document25 pagesUnit 1haniaNo ratings yet

- IB Economics Chapter 1 NotesDocument6 pagesIB Economics Chapter 1 NotesPauline OngchanNo ratings yet

- Intro To EconomicsDocument29 pagesIntro To EconomicsShiloh MillingtonNo ratings yet

- Managerial Econ Notes 1Document7 pagesManagerial Econ Notes 1Angelique CaliNo ratings yet

- Chapter 1 Ten Principles of EconomicsDocument50 pagesChapter 1 Ten Principles of EconomicsLinh ChiNo ratings yet

- 1 - Introduction To EconomicsDocument24 pages1 - Introduction To EconomicsYoshraNo ratings yet

- ECO 162-Introduction To MicroeconomicDocument48 pagesECO 162-Introduction To MicroeconomicNorjiella Binti Mohd NurdinNo ratings yet

- Topic 1 Lecturer Introduction RevisedDocument27 pagesTopic 1 Lecturer Introduction RevisedsskiemNo ratings yet

- Managerial Economics A.Economics As The Science of Scarcity EconomicsDocument10 pagesManagerial Economics A.Economics As The Science of Scarcity EconomicsJulia Isabel LuizonNo ratings yet

- Managerial Economics A.Economics As The Science of Scarcity EconomicsDocument10 pagesManagerial Economics A.Economics As The Science of Scarcity EconomicsJulia Isabel LuizonNo ratings yet

- Eco 101 Chap 1Document8 pagesEco 101 Chap 1rezsxNo ratings yet

- Document 23Document33 pagesDocument 232023856678No ratings yet

- Basic Economic IdeasDocument99 pagesBasic Economic IdeasTaide Giselle Botello VelascoNo ratings yet

- APPLIED ECON - Lesson 2Document4 pagesAPPLIED ECON - Lesson 2Deane TriaNo ratings yet

- Solution Manual For Economics Today The Macro 17th Edition by Roger LeRoy Miller ISBN 0132948893 9780132948890Document36 pagesSolution Manual For Economics Today The Macro 17th Edition by Roger LeRoy Miller ISBN 0132948893 9780132948890jacobdaviswckfzotpma100% (27)

- BUSFF019 Lecture 1 - Basic Economic ProblemDocument35 pagesBUSFF019 Lecture 1 - Basic Economic ProblemTan Hong EeNo ratings yet

- Economics Today 19th Edition Miller Solutions ManualDocument25 pagesEconomics Today 19th Edition Miller Solutions ManualKristinRichardsygci100% (57)

- Unit 1Document5 pagesUnit 1openedwithedgeNo ratings yet

- Topic 1: Introduction To Factors of Production & Consumer & Producer SurplusDocument3 pagesTopic 1: Introduction To Factors of Production & Consumer & Producer SurplusNicz ClueNo ratings yet

- AP Chapter1 Less 2Document2 pagesAP Chapter1 Less 2Hannah Denise BatallangNo ratings yet

- Scarcity: Can Produce More Products.Document3 pagesScarcity: Can Produce More Products.ela kikayNo ratings yet

- Learning Outcome 1 Part 1 Understand Economic Relationships Using GraphsDocument46 pagesLearning Outcome 1 Part 1 Understand Economic Relationships Using GraphsLikamva MgqamqhoNo ratings yet

- Agricultural EconomicsDocument11 pagesAgricultural EconomicsMicah Tanjusay PonsicaNo ratings yet

- Main - Economics Edexcel Notes ChapterwseDocument67 pagesMain - Economics Edexcel Notes Chapterwse7a4374 hisNo ratings yet

- Solution Manual For Economics Today The Micro 17th Edition by Roger LeRoy Miller ISBN 0132948885 9780132948883Document36 pagesSolution Manual For Economics Today The Micro 17th Edition by Roger LeRoy Miller ISBN 0132948885 9780132948883jacobdaviswckfzotpma100% (27)

- Solution Manual For Economics Today The Micro 17Th Edition by Roger Leroy Miller Isbn 0132948885 9780132948883 Full Chapter PDFDocument30 pagesSolution Manual For Economics Today The Micro 17Th Edition by Roger Leroy Miller Isbn 0132948885 9780132948883 Full Chapter PDFjoel.parkman549100% (11)

- Chapter 1 - Ten Principles of EconomicsDocument23 pagesChapter 1 - Ten Principles of EconomicsJellyBeanNo ratings yet

- Ten Principles of EconomicsDocument7 pagesTen Principles of EconomicsPaolo Niel ArenasNo ratings yet

- Dwnload Full Economics Today 19th Edition Miller Solutions Manual PDFDocument35 pagesDwnload Full Economics Today 19th Edition Miller Solutions Manual PDFdavidhughestxxs100% (12)

- Economics Today 19th Edition Miller Solutions ManualDocument22 pagesEconomics Today 19th Edition Miller Solutions Manualtuyetmanuelm5h5100% (23)

- Introduction To Economics: Choices, Choices, Choices, - .Document69 pagesIntroduction To Economics: Choices, Choices, Choices, - .Prasad GharatNo ratings yet

- Introductiontoeconomics 141225043847 Conversion Gate02 1Document31 pagesIntroductiontoeconomics 141225043847 Conversion Gate02 1johnrafaelrentuma27No ratings yet

- Or Chapter 2 Resource UtilizationDocument29 pagesOr Chapter 2 Resource UtilizationKate AlvarezNo ratings yet

- 12EPP Chapter 01Document135 pages12EPP Chapter 01godwill olivaNo ratings yet

- Chapter 1 and 2 NotesDocument8 pagesChapter 1 and 2 NotesScott MaNo ratings yet

- Dwnload Full Economics Today The Micro View 18th Edition Miller Solutions Manual PDFDocument35 pagesDwnload Full Economics Today The Micro View 18th Edition Miller Solutions Manual PDFirisybarrous100% (7)

- Week 2 - Introduction To EconomicsDocument26 pagesWeek 2 - Introduction To EconomicsAaNo ratings yet

- Course I - Section I - DR - Kanyarat NimtrakoolDocument58 pagesCourse I - Section I - DR - Kanyarat NimtrakoolJO JENG CHINNo ratings yet

- What Are The Fundamental Economic Problems?Document11 pagesWhat Are The Fundamental Economic Problems?Anonymous XIDvTPdNNo ratings yet

- Ch2 Microeconomics ECODocument44 pagesCh2 Microeconomics ECOBazil NawazNo ratings yet

- Economics Study Pack PDFDocument158 pagesEconomics Study Pack PDFIsaac PepukayiNo ratings yet

- Monopoly Problems: Problem 2 Problem 3Document2 pagesMonopoly Problems: Problem 2 Problem 3RyanNo ratings yet

- Pure Competition AnswersDocument5 pagesPure Competition AnswersRyanNo ratings yet

- ProductionCost ProblemsDocument3 pagesProductionCost ProblemsRyanNo ratings yet

- Pure Competition ProblemsDocument3 pagesPure Competition ProblemsRyanNo ratings yet

- Micro 6 Perfect CompetitionDocument7 pagesMicro 6 Perfect CompetitionRyanNo ratings yet

- Micro 8 Imperfect CompetitionDocument5 pagesMicro 8 Imperfect CompetitionRyanNo ratings yet

- Monopoly AnswersDocument4 pagesMonopoly AnswersRyanNo ratings yet

- Micro 4 Consumer TheoryDocument8 pagesMicro 4 Consumer TheoryRyanNo ratings yet

- ECO WORKSHEETS (Stats - 8 QS) : Q1) Distinguish BTW Short Run and Long RunDocument8 pagesECO WORKSHEETS (Stats - 8 QS) : Q1) Distinguish BTW Short Run and Long RunmickeyNo ratings yet

- Guia Usa Nataly Largo 772134549015Document7 pagesGuia Usa Nataly Largo 772134549015samadhi sierraNo ratings yet

- Financial and Management Accounting Sample Exam Questions: MBA ProgrammeDocument16 pagesFinancial and Management Accounting Sample Exam Questions: MBA ProgrammeFidoNo ratings yet

- WSP Rapid Transit BrochureDocument18 pagesWSP Rapid Transit BrochurePATEL MIHIKANo ratings yet

- AI Personal Financial AdvisorDocument14 pagesAI Personal Financial AdvisorNaddaa MohamedNo ratings yet

- Crafting A Legacy InvestigatingDocument17 pagesCrafting A Legacy InvestigatingrannuagarwalNo ratings yet

- 2015 BG Catalogue PDFDocument210 pages2015 BG Catalogue PDFCharles RiceNo ratings yet

- Amcham Directory - Public EditedDocument266 pagesAmcham Directory - Public EditedRaymart AauinoNo ratings yet

- SR-1 Leave Application FormDocument1 pageSR-1 Leave Application FormUma Maheswararao0% (1)

- Project Report On Performance AppraisalDocument63 pagesProject Report On Performance AppraisalLalit chauhan0% (1)

- Sa 3 DT NovDocument9 pagesSa 3 DT NovRishabh GargNo ratings yet

- Masterlist - FO-UEF-0.037 Batch Upload Template - Enrollment - Rev.02Document6,568 pagesMasterlist - FO-UEF-0.037 Batch Upload Template - Enrollment - Rev.02gamingpurposes onlyNo ratings yet

- Mecklai Financial: Markets AdvisoryDocument1 pageMecklai Financial: Markets AdvisoryMukesh GuptaNo ratings yet

- Unit Data - 10Document2 pagesUnit Data - 10Homes ElevenNo ratings yet

- Staffing Global OperationsDocument4 pagesStaffing Global OperationsSonia Lawson100% (1)

- Master Thesis Swot AnalysisDocument5 pagesMaster Thesis Swot AnalysisKayla Jones100% (1)

- Sales Contract No. 001/SC-SHP/09/2021Document2 pagesSales Contract No. 001/SC-SHP/09/2021QrenNo ratings yet

- SOP NimaDocument3 pagesSOP NimaMohammad kafshdar jameNo ratings yet

- SGENESIS FINTECH PVT LTD - Required Documents For All Loans - New LogoDocument10 pagesSGENESIS FINTECH PVT LTD - Required Documents For All Loans - New Logodattam venkateswarluNo ratings yet

- Adobe Scan 2 de Jun. de 2023Document2 pagesAdobe Scan 2 de Jun. de 2023Enrique GuevaraNo ratings yet

- Strategic Marketing ManagementDocument365 pagesStrategic Marketing ManagementMary Ann Gabion100% (1)

- Presented By:-: Nitish Garg Gurharpreet RanganathDocument25 pagesPresented By:-: Nitish Garg Gurharpreet Ranganathinvestigation duediligenceNo ratings yet

- Alegarme, Eng 227 Activity 13Document3 pagesAlegarme, Eng 227 Activity 13Gene Kenneth ParagasNo ratings yet

- The Fluidity of Molten MetalDocument14 pagesThe Fluidity of Molten Metalrafiqhariyanto100% (1)

- ERP Sample LeadsDocument3 pagesERP Sample LeadsIvyNo ratings yet

- Pile Cutting / Hacking (Sub-Structure Work)Document2 pagesPile Cutting / Hacking (Sub-Structure Work)Rahmat HariNo ratings yet

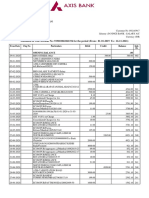

- Statement of Axis Account No:919010061861194 For The Period (From: 01-01-2019 To: 16-11-2021)Document4 pagesStatement of Axis Account No:919010061861194 For The Period (From: 01-01-2019 To: 16-11-2021)udi969No ratings yet

- Diagnostic Exam Accounting 1.1 AKDocument14 pagesDiagnostic Exam Accounting 1.1 AKRobert CastilloNo ratings yet

- Week6 Acomprehensiveillustration CompressDocument86 pagesWeek6 Acomprehensiveillustration CompressTariku0% (1)

- Corruption and Central Vigilance Commission: Made By: David Cyril Babu B.A. LLB (Honours) Viii Semester Roll No. 18Document162 pagesCorruption and Central Vigilance Commission: Made By: David Cyril Babu B.A. LLB (Honours) Viii Semester Roll No. 18T M Santhosh KumarNo ratings yet