You might also like

- Special ProceedingsDocument21 pagesSpecial Proceedingsstargazer0732No ratings yet

- Estate and Gift Tax OutlineDocument26 pagesEstate and Gift Tax OutlineDaniela Pretus100% (2)

- Quit Claim DeedDocument3 pagesQuit Claim DeedRocketLawyer86% (14)

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument13 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledHib Atty TalaNo ratings yet

- Pointers:: Oct 28, 1977, Roxas v. Court of Appeals, GR No. 138660, February 5, 2004)Document3 pagesPointers:: Oct 28, 1977, Roxas v. Court of Appeals, GR No. 138660, February 5, 2004)Nowell SimNo ratings yet

- Authority To Sell Blank TemplateDocument1 pageAuthority To Sell Blank TemplateJaimee Ruth LiganNo ratings yet

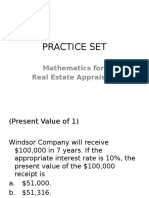

- Practice SetDocument39 pagesPractice SetDionico O. Payo Jr.No ratings yet

- Residential Subdivisions GuideDocument104 pagesResidential Subdivisions Guidethanh_nguyen760No ratings yet

- Documentation and Registration-ExamDocument11 pagesDocumentation and Registration-ExamLina Michelle Matheson Brual100% (1)

- Other Realty Holdings Real Estate Investment TrustDocument13 pagesOther Realty Holdings Real Estate Investment TrustAriel MartinezNo ratings yet

- Fundamental of Property OwnershipDocument5 pagesFundamental of Property OwnershipJosue Sandigan Biolon SecorinNo ratings yet

- Part II. Chapter 4 Appraisal Assessment of Real Property TaxDocument69 pagesPart II. Chapter 4 Appraisal Assessment of Real Property TaxRuiz, Cherryjane100% (1)

- RR No. 7-2003Document9 pagesRR No. 7-2003Lorenzo BalmoriNo ratings yet

- REM ProcessDocument11 pagesREM ProcessAAPHBRSNo ratings yet

- LBP AppraisalDocument24 pagesLBP Appraisaldonaldhax01No ratings yet

- Fundamentals of Real PropertyDocument74 pagesFundamentals of Real PropertyFrancis L100% (1)

- Criminal Investigation ManualDocument500 pagesCriminal Investigation Manuallegalatwork100% (1)

- O.S.-RADHA - Site 172Document17 pagesO.S.-RADHA - Site 172Kumara Swamy100% (1)

- Book 1Document2 pagesBook 1UrmiNo ratings yet

- Taxation QuestionsDocument63 pagesTaxation QuestionsPrince EG DltgNo ratings yet

- Sux 2017 TSN Exam 1Document49 pagesSux 2017 TSN Exam 1SofiaNo ratings yet

- Land Titles PreBar 2015 - Atty. AbanoDocument13 pagesLand Titles PreBar 2015 - Atty. AbanoMaribeth ArandiaNo ratings yet

- R-890 S. 2012Document8 pagesR-890 S. 2012mabzicleNo ratings yet

- REAL PROPERTY TAXATION - PresentationDocument71 pagesREAL PROPERTY TAXATION - PresentationMarcial Militante100% (1)

- Real Estate Taxation - Transfer of PropertyDocument9 pagesReal Estate Taxation - Transfer of PropertyJuan FrivaldoNo ratings yet

- As Amended by DO No. 22, S. of 1987, DAO No. 2, S. of 1988 and DAO No. 6, S. of 1994Document12 pagesAs Amended by DO No. 22, S. of 1987, DAO No. 2, S. of 1988 and DAO No. 6, S. of 1994Richard Villaverde100% (1)

- Extrajudicial Settlement of Estate Template 2Document4 pagesExtrajudicial Settlement of Estate Template 2bro smartNo ratings yet

- CRES2015 Module1 Mocknov302015Document29 pagesCRES2015 Module1 Mocknov302015Law_PortalNo ratings yet

- Real Estate Brokerage & PracticeDocument3 pagesReal Estate Brokerage & PracticeMarisseAnne Coquilla100% (1)

- Amended Guidelines Abot-Kamay Pabahay Program'Document30 pagesAmended Guidelines Abot-Kamay Pabahay Program'Ge-An Moiseah Salud AlmueteNo ratings yet

- Investment PropertyDocument3 pagesInvestment PropertyacyNo ratings yet

- Appraisal & Assessment in The Government SectorDocument33 pagesAppraisal & Assessment in The Government SectorRonald MojadoNo ratings yet

- Land Ownership and Property Acquisition in The PhilippinesDocument4 pagesLand Ownership and Property Acquisition in The PhilippinesNathaniel RasosNo ratings yet

- Resa and Irr - Cres 2014Document23 pagesResa and Irr - Cres 2014Ariel MartinezNo ratings yet

- Real Propert Y: TaxationDocument41 pagesReal Propert Y: TaxationFreeza Masculino FabrigasNo ratings yet

- Deed of Absolute SaleDocument3 pagesDeed of Absolute SaleKim Roque-AquinoNo ratings yet

- Real Estate Service Act of The Philippines PDFDocument15 pagesReal Estate Service Act of The Philippines PDFVener Angelo MargalloNo ratings yet

- Real Estate Service Act (Resa Law) Republic Act 9646Document18 pagesReal Estate Service Act (Resa Law) Republic Act 9646Mike Angelow EsperaNo ratings yet

- BSREM Business and Real Etate TaxationDocument6 pagesBSREM Business and Real Etate TaxationRheneir MoraNo ratings yet

- Real Estate PracticeDocument5 pagesReal Estate PracticeDa Yani ChristeeneNo ratings yet

- Timeline of Land and Agrarian Reform in The PhilippinesDocument1 pageTimeline of Land and Agrarian Reform in The PhilippinesYsai GeverNo ratings yet

- PRBRES ResolutionsDocument1 pagePRBRES ResolutionsDexterNo ratings yet

- Fundamentals of Property Ownership, Real Estate Practice & TaxesDocument6 pagesFundamentals of Property Ownership, Real Estate Practice & TaxesNor Lits100% (1)

- Exam Program Real Estate Brokers April 2024Document4 pagesExam Program Real Estate Brokers April 2024geraldinelacambra34No ratings yet

- Arias vs. SandiganbayanDocument17 pagesArias vs. SandiganbayanFlorz Gelarz0% (1)

- Unnotarized Deed of Sale Vis A Vis Land RegistrationDocument1 pageUnnotarized Deed of Sale Vis A Vis Land RegistrationAlyk CalionNo ratings yet

- LRA Land Acquisition and OwnershipDocument6 pagesLRA Land Acquisition and OwnershipRandolph AlvarezNo ratings yet

- Accomplishment Report 2021Document9 pagesAccomplishment Report 2021Chacha CawiliNo ratings yet

- Valuation of Expropriated PropertiesDocument10 pagesValuation of Expropriated PropertiesLuningning CariosNo ratings yet

- R"DL"D : Housingand Boari)Document7 pagesR"DL"D : Housingand Boari)Rina Fajardo - NacinNo ratings yet

- PD 1812 - Amended Provision of PD 464 (Real Prop Tax Code)Document2 pagesPD 1812 - Amended Provision of PD 464 (Real Prop Tax Code)Rocky MarcianoNo ratings yet

- LTD Lecture 07192023Document9 pagesLTD Lecture 07192023Emmanuel FernandezNo ratings yet

- CH 01Document64 pagesCH 01Kh H100% (1)

- Fundamentals of Property OwnershipDocument2 pagesFundamentals of Property OwnershipJasielle Leigh UlangkayaNo ratings yet

- When To Reject Loan Collateral OffersDocument6 pagesWhen To Reject Loan Collateral OffersLuningning CariosNo ratings yet

- Regalian DoctrineDocument4 pagesRegalian DoctrineJacinto HyacinthNo ratings yet

- License To SellDocument24 pagesLicense To SellMay YellowNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- BIR Ruling No. 340-11 - E-BooksDocument5 pagesBIR Ruling No. 340-11 - E-BooksCkey ArNo ratings yet

- Broker Reviewer 2022Document8 pagesBroker Reviewer 2022Janzel SantillanNo ratings yet

- Guidelines and Instructions For BIR FORM No. 2118-EA Estate Tax Amnesty ReturnDocument1 pageGuidelines and Instructions For BIR FORM No. 2118-EA Estate Tax Amnesty ReturnChaNo ratings yet

- Cost Benefit AnalysisDocument2 pagesCost Benefit AnalysisAriel Peralta AdvientoNo ratings yet

- PD 464Document36 pagesPD 464Nath VillenaNo ratings yet

- CD - 36. CIR v. Aquafresh SeafoodsDocument3 pagesCD - 36. CIR v. Aquafresh SeafoodsCzarina CidNo ratings yet

- Evat Law Leased of Real PropertyDocument5 pagesEvat Law Leased of Real Propertyenal92No ratings yet

- Bir RR 16-2011Document4 pagesBir RR 16-2011ATTY. R.A.L.C.100% (1)

- Sec Memo 11, s2008Document5 pagesSec Memo 11, s2008aian josephNo ratings yet

- RA 3844 - Land Reform Act ExcerptDocument1 pageRA 3844 - Land Reform Act Excerptleena corpuzNo ratings yet

- Estate TaxDocument22 pagesEstate TaxCat ValentineNo ratings yet

- Guides in Buying Portion of LandDocument8 pagesGuides in Buying Portion of LandDindo CabudbudNo ratings yet

- Law of AgencyDocument11 pagesLaw of Agencyprabharun18No ratings yet

- BIR IssuancesDocument47 pagesBIR IssuancesJill De Dumo-CornistaNo ratings yet

- RR 07-03Document3 pagesRR 07-03saintkarriNo ratings yet

- rr7 2003Document6 pagesrr7 2003James Estrada CastroNo ratings yet

- Unfair Labor PracticeDocument21 pagesUnfair Labor PracticeBrian BaldwinNo ratings yet

- Allied Banking Corporation Vs Cir (GR 175097 February 5 2010)Document8 pagesAllied Banking Corporation Vs Cir (GR 175097 February 5 2010)Brian BaldwinNo ratings yet

- SEnA Rules of Procedure PDFDocument12 pagesSEnA Rules of Procedure PDFBrian BaldwinNo ratings yet

- OFW Permanent Disability 4Document17 pagesOFW Permanent Disability 4Brian BaldwinNo ratings yet

- Cir Vs Sony Philippines Inc (GR 178697 November 17 2010)Document11 pagesCir Vs Sony Philippines Inc (GR 178697 November 17 2010)Brian BaldwinNo ratings yet

- Cir Vs SC Johnson (GR 127105 June 25 1999)Document11 pagesCir Vs SC Johnson (GR 127105 June 25 1999)Brian BaldwinNo ratings yet

- Fishwealth Canning Corp Vs Cir (GR 179343 January 21 2010)Document2 pagesFishwealth Canning Corp Vs Cir (GR 179343 January 21 2010)Brian BaldwinNo ratings yet

- Oriental Shipping Vs Nazal (Gr177103 June 3 2013) Not Entitled To Benefits If Seafarer Obtains Subsequent EmploymentDocument10 pagesOriental Shipping Vs Nazal (Gr177103 June 3 2013) Not Entitled To Benefits If Seafarer Obtains Subsequent EmploymentBrian BaldwinNo ratings yet

- Fels Energy Vs Province of Batangas (GR 168557 February 16 2007)Document15 pagesFels Energy Vs Province of Batangas (GR 168557 February 16 2007)Brian BaldwinNo ratings yet

- Magsaysay Maritime Vs NLRC (Gr191903 June 19 2013) Abandonment of Treatment Cannot Claim For BenefitsDocument14 pagesMagsaysay Maritime Vs NLRC (Gr191903 June 19 2013) Abandonment of Treatment Cannot Claim For BenefitsBrian BaldwinNo ratings yet

- Phil Transmarine Carriers Vs Leandro Legaspi (Gr202791 June 19 2013) Return of Excess Payment During Execution ProceedingsDocument12 pagesPhil Transmarine Carriers Vs Leandro Legaspi (Gr202791 June 19 2013) Return of Excess Payment During Execution ProceedingsBrian BaldwinNo ratings yet

- Lorenzo Tanga-An Vs Phil Transmarine Carriers (Gr180636 March 13 2013) Extent of Awards in Illegal DismissalDocument12 pagesLorenzo Tanga-An Vs Phil Transmarine Carriers (Gr180636 March 13 2013) Extent of Awards in Illegal DismissalBrian BaldwinNo ratings yet

- Maersk Crewing Vs Mesina (Gr200837 June 5 2013) Psoriasis Is Work RelatedDocument13 pagesMaersk Crewing Vs Mesina (Gr200837 June 5 2013) Psoriasis Is Work RelatedBrian BaldwinNo ratings yet

- Transocean Ship Management Vs Inocencio Vedad (Gr194490-91 March 20 2013) Cancer of Tonsil Not Work RelatedDocument11 pagesTransocean Ship Management Vs Inocencio Vedad (Gr194490-91 March 20 2013) Cancer of Tonsil Not Work RelatedBrian BaldwinNo ratings yet

- Contract of Lease Know All Men by These PresentsDocument3 pagesContract of Lease Know All Men by These PresentsToby RogersNo ratings yet

- 01 - Lorenzo V PosadasDocument21 pages01 - Lorenzo V PosadasRaymond ChengNo ratings yet

- Marcelo Soriano v. Sps. Ricardo and Rosalina GalitDocument15 pagesMarcelo Soriano v. Sps. Ricardo and Rosalina GalitEmma Ruby Aguilar-ApradoNo ratings yet

- Rio y Olabarrieta and MolinaDocument2 pagesRio y Olabarrieta and MolinaGela Bea BarriosNo ratings yet

- Rental Bonds Online - NSW Fair TradingDocument3 pagesRental Bonds Online - NSW Fair TradingmuslimnswNo ratings yet

- Real EstateDocument9 pagesReal EstateDivyansh NegiNo ratings yet

- List of IxpsDocument17 pagesList of IxpsBonaan Malkaa GibeeNo ratings yet

- Daclag Vs MacahiligDocument1 pageDaclag Vs MacahiligShane FulguerasNo ratings yet

- Property Information Pack - 15C Ngatiawa StreetDocument82 pagesProperty Information Pack - 15C Ngatiawa StreetYanci LNo ratings yet

- Suffolk Times Classifieds and Service Directory: June 8, 2017Document15 pagesSuffolk Times Classifieds and Service Directory: June 8, 2017Timesreview100% (1)

- Building Research & InformationDocument24 pagesBuilding Research & InformationAjeng LidyaNo ratings yet

- Math Lesson2 - 7 PDFDocument3 pagesMath Lesson2 - 7 PDFcermatikaNo ratings yet

- Presentation The New Condominium Rules 9 1 2018 PDFDocument35 pagesPresentation The New Condominium Rules 9 1 2018 PDFYe AungNo ratings yet

- What Do You Need To Know About Real Estate Taxes in The Philippines?Document6 pagesWhat Do You Need To Know About Real Estate Taxes in The Philippines?jenefer solamilloNo ratings yet

- Cebu Winland Development Corporation vs. Ong Siao Hua, G.R. No. 173215, May 21, 2009Document10 pagesCebu Winland Development Corporation vs. Ong Siao Hua, G.R. No. 173215, May 21, 2009strgrlNo ratings yet

- King's Tower - Public Notice SBCADocument2 pagesKing's Tower - Public Notice SBCASyed Muhammad KamranNo ratings yet

- Residential Sales Contract (Virginia) (07/2016) - K1321Document16 pagesResidential Sales Contract (Virginia) (07/2016) - K1321Jacky BoungNo ratings yet