You might also like

- Tri Merge-Instructions 2Document11 pagesTri Merge-Instructions 2Samson Fortune92% (12)

- Record Label Business Plan ExampleDocument25 pagesRecord Label Business Plan ExampleAtemNo ratings yet

- 60 Second Binary Options Strategy: The Complete GuideDocument15 pages60 Second Binary Options Strategy: The Complete GuideTrade Opus70% (10)

- Week 1 ITM 410Document76 pagesWeek 1 ITM 410Awesom QuenzNo ratings yet

- CDC 2015 Annual ReportDocument69 pagesCDC 2015 Annual ReportPipoy ReglosNo ratings yet

- AALendingAdvancedPart4 PDFDocument102 pagesAALendingAdvancedPart4 PDFlolitaferoz100% (2)

- Overview If Railway AccountsDocument40 pagesOverview If Railway AccountsKannan ChakrapaniNo ratings yet

- Employer Reference Letter FormatDocument2 pagesEmployer Reference Letter FormatSiddharthNo ratings yet

- Republic vs. National Labor Relations CommissionsDocument2 pagesRepublic vs. National Labor Relations CommissionsBryan MolinaNo ratings yet

- Economic Survey 2019 - 20201125024153Document342 pagesEconomic Survey 2019 - 20201125024153Himani100% (1)

- Economic Impact of Covid-19 in The Philippines: Fact File 2020Document26 pagesEconomic Impact of Covid-19 in The Philippines: Fact File 2020Girlee Jhene CadeliñaNo ratings yet

- Economics General Degree Program Faculty of Applied Sciences University of Sri JayewardenepuraDocument19 pagesEconomics General Degree Program Faculty of Applied Sciences University of Sri JayewardenepuraUmesha SavindiNo ratings yet

- 160811ID Tax Revenues SlippingDocument3 pages160811ID Tax Revenues SlippingDaniel Pandapotan MarpaungNo ratings yet

- Evaluation of Digital Realty Trust IncDocument18 pagesEvaluation of Digital Realty Trust Incwafula stanNo ratings yet

- Investor Digest: Equity Research - 22 December 2020Document11 pagesInvestor Digest: Equity Research - 22 December 2020Ian RizkiNo ratings yet

- Q3 2021 PFE Earnings ReleaseDocument37 pagesQ3 2021 PFE Earnings ReleaseBruno EnriqueNo ratings yet

- Financial Statement Analysis-2Document12 pagesFinancial Statement Analysis-2Glaidel Rodenas PeñaNo ratings yet

- Economic Survey IndiaDocument16 pagesEconomic Survey IndiaAtanu MukherjeeNo ratings yet

- Group F FIN201 Section 3Document27 pagesGroup F FIN201 Section 3Nayeem MahmudNo ratings yet

- Villaviciosa Abra ES2014Document7 pagesVillaviciosa Abra ES2014J JaNo ratings yet

- AnalysisDocument7 pagesAnalysisrajibzzamanibcsNo ratings yet

- Understanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu AnthonyDocument10 pagesUnderstanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu Anthonyabdulbasitabdulazeez30No ratings yet

- Evidence Based Revenue Forecasting FY 2021 22Document15 pagesEvidence Based Revenue Forecasting FY 2021 22siddique akbarNo ratings yet

- 2011 Prelim City Budget FinalDocument53 pages2011 Prelim City Budget FinalEarlynoftenNo ratings yet

- LBRMO 0913 Budget FactsDocument22 pagesLBRMO 0913 Budget FactsDave LabianoNo ratings yet

- Id 22072020 PDFDocument11 pagesId 22072020 PDFbala gamerNo ratings yet

- Compiled Economic Survey English 2019/20Document256 pagesCompiled Economic Survey English 2019/20Hanu ManNo ratings yet

- Interim Budget FY20Document7 pagesInterim Budget FY20InvesTrekkNo ratings yet

- The Examiner's Answers - F3 - Financial Strategy: Section ADocument20 pagesThe Examiner's Answers - F3 - Financial Strategy: Section AMinhas Bin BadurdeenNo ratings yet

- Restated Earnings Largely Driven by Non-Cash Expenses: 2GO Group, IncDocument4 pagesRestated Earnings Largely Driven by Non-Cash Expenses: 2GO Group, IncJNo ratings yet

- MODULE 3 UNIT 2 TRAIN SUPPLEMENTAL READING 1 Aki - Policy - Brief - Volume - Xii - No. - 4 - 2019Document6 pagesMODULE 3 UNIT 2 TRAIN SUPPLEMENTAL READING 1 Aki - Policy - Brief - Volume - Xii - No. - 4 - 2019Isabella AlfonsoNo ratings yet

- FY2010 Analysis of The National Budget For FY2009 10Document39 pagesFY2010 Analysis of The National Budget For FY2009 1099amee99No ratings yet

- Chapter-06 Eng Eng-21Document16 pagesChapter-06 Eng Eng-21Riyad HossainNo ratings yet

- Section 2Document14 pagesSection 2Hafiz TajuddinNo ratings yet

- The Philippine Economy: Prospects and Outlook For 2015-2016Document13 pagesThe Philippine Economy: Prospects and Outlook For 2015-2016ristNo ratings yet

- Economy Budget 2020 PreviewDocument9 pagesEconomy Budget 2020 PreviewAnonymous gMgeQl1SndNo ratings yet

- q2 Investor Forum 2017 2Document15 pagesq2 Investor Forum 2017 2Nisal Nuwan SenarathnaNo ratings yet

- Philippine Economic Updates May 2023Document2 pagesPhilippine Economic Updates May 2023regina.bumatayNo ratings yet

- Results For Announcement To The MarketDocument63 pagesResults For Announcement To The MarketTimBarrowsNo ratings yet

- Covid19 The Impact On Healthcare ExpenditureDocument9 pagesCovid19 The Impact On Healthcare ExpenditureDavid ChueNo ratings yet

- Budget 2011-12 - FinalDocument62 pagesBudget 2011-12 - FinalNavneet BaliNo ratings yet

- BHP Results For The Year Ended 30 June 2020Document62 pagesBHP Results For The Year Ended 30 June 2020Renan Dantas SantosNo ratings yet

- Consensus EstimatesDocument4 pagesConsensus EstimatesClickon DetroitNo ratings yet

- Bangladesh National Budget Review FY24Document27 pagesBangladesh National Budget Review FY24Asif MahmudNo ratings yet

- Mu Budget 2021 NoexpDocument64 pagesMu Budget 2021 NoexpSweet JasNo ratings yet

- Sustained Leadership in Life Insurance: October 2010Document39 pagesSustained Leadership in Life Insurance: October 2010VarunSoodNo ratings yet

- Economic Prospects and Challenges 2020 - 15sept2020Document26 pagesEconomic Prospects and Challenges 2020 - 15sept2020Quartantyo WijanarkoNo ratings yet

- Humanica Company Ipo ReportDocument15 pagesHumanica Company Ipo ReportVk VirataNo ratings yet

- 3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina CorporationDocument8 pages3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina Corporationherrewt rewterwNo ratings yet

- Revenue Statistics Asia and Pacific PhilippinesDocument2 pagesRevenue Statistics Asia and Pacific Philippinesbry christianNo ratings yet

- Brazil 2019 Boom Bust and The Road To Recovery Book Launch Presentation 6634754 v1 DMSDR1S 1Document29 pagesBrazil 2019 Boom Bust and The Road To Recovery Book Launch Presentation 6634754 v1 DMSDR1S 1João SimasNo ratings yet

- Edel India Strategy 5 Pathways To EfficiencyDocument40 pagesEdel India Strategy 5 Pathways To EfficiencyarhagarNo ratings yet

- Year 2014 2015 2016 2017 Net Revenue Net Revenue GrowthDocument7 pagesYear 2014 2015 2016 2017 Net Revenue Net Revenue GrowthNgoc DuongNo ratings yet

- The California Budget: The Top Ten Budget Myths... and The TruthDocument34 pagesThe California Budget: The Top Ten Budget Myths... and The TruthceruleandazeNo ratings yet

- ICICI Securities Power Finance Corporation Initiating CoverageDocument27 pagesICICI Securities Power Finance Corporation Initiating CoverageSudharsanNo ratings yet

- The Parliamentary Budget Office's Fiscal Sustainability Report 2017Document125 pagesThe Parliamentary Budget Office's Fiscal Sustainability Report 2017caleyramsayNo ratings yet

- 2021 Fiscal PerformanceDocument5 pages2021 Fiscal PerformanceFuaad DodooNo ratings yet

- MPS FY2021-22:: CPD's Reaction OnDocument49 pagesMPS FY2021-22:: CPD's Reaction OnAdnan AsifNo ratings yet

- 2020 Q 3 ReleaseDocument4 pages2020 Q 3 ReleasentNo ratings yet

- Guinea: Inflation (Annual %)Document2 pagesGuinea: Inflation (Annual %)Sayni DasNo ratings yet

- City of Fort St. John - 2022 Operating and Capital BudgetsDocument52 pagesCity of Fort St. John - 2022 Operating and Capital BudgetsAlaskaHighwayNewsNo ratings yet

- AsadUmarseminarbudget2012 3Document18 pagesAsadUmarseminarbudget2012 3Ahsan AliNo ratings yet

- Revenue Mobilization and Current Tax Issues: The Case of The PhilippinesDocument22 pagesRevenue Mobilization and Current Tax Issues: The Case of The PhilippinesAdrian PanganibanNo ratings yet

- Continues To Book Net Losses Flattish Q/Q Performance: Fruitas Holdings, IncDocument4 pagesContinues To Book Net Losses Flattish Q/Q Performance: Fruitas Holdings, IncJajahinaNo ratings yet

- Citizens Budget in Somalia (2018)Document7 pagesCitizens Budget in Somalia (2018)Apdalle AhmetNo ratings yet

- CalculationsDocument5 pagesCalculationsKhawaja HamzaNo ratings yet

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismFrom EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismNo ratings yet

- Cambridge O Level: Business Studies 7115/24 May/June 2021Document19 pagesCambridge O Level: Business Studies 7115/24 May/June 2021nayna sharminNo ratings yet

- Market StructureDocument8 pagesMarket Structureapi-545204930No ratings yet

- Transaction Profile PDFDocument1 pageTransaction Profile PDFTanzir HasanNo ratings yet

- 141 14 513Document53 pages141 14 513Pik PokNo ratings yet

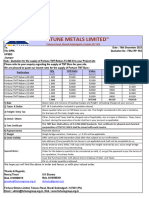

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Document1 page"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaNo ratings yet

- San Mateo Municipal College: Accounting Information System Midterms Activity Understanding A Relational DatabaseDocument2 pagesSan Mateo Municipal College: Accounting Information System Midterms Activity Understanding A Relational Database버니 모지코No ratings yet

- Crop and Water Productivity, Energy Auditing, Carbon Footprints and Soil Health Indicators of Bt-Cotton Transplanting Led System IntensificationDocument3 pagesCrop and Water Productivity, Energy Auditing, Carbon Footprints and Soil Health Indicators of Bt-Cotton Transplanting Led System IntensificationAmanNo ratings yet

- A Study of Bachat Gat & Women Empowerment in Nagpur City: October 2019Document5 pagesA Study of Bachat Gat & Women Empowerment in Nagpur City: October 2019Chaitali VartheNo ratings yet

- Uniform Manufacturer in QatarDocument5 pagesUniform Manufacturer in QatarHouse of UniformsNo ratings yet

- Surya SAP SD 4yr ResumeDocument3 pagesSurya SAP SD 4yr Resumeharish bolisettyNo ratings yet

- 1) Week 2 - Statement of Financial Position v3 - TaggedDocument51 pages1) Week 2 - Statement of Financial Position v3 - TaggedNabilNo ratings yet

- Chapter 3 The Marketing EnvironmentDocument6 pagesChapter 3 The Marketing EnvironmentMUHAMMAD AZHARUDDIN BIN AZNI MoeNo ratings yet

- Consumer Behaviour Case StudyDocument6 pagesConsumer Behaviour Case Studyhiralpatel3085100% (1)

- Intuition DiscountingDocument56 pagesIntuition DiscountingklklNo ratings yet

- Impulse Technical, Nifty Algo Performance Sheet 50000Document17 pagesImpulse Technical, Nifty Algo Performance Sheet 50000Video JunctionNo ratings yet

- Transactions List: Ciprian-Nicolae Frigioi RO27BRDE180SV70010251800 RON Ciprian-Nicolae FrigioiDocument3 pagesTransactions List: Ciprian-Nicolae Frigioi RO27BRDE180SV70010251800 RON Ciprian-Nicolae FrigioiCiprian FrigioiNo ratings yet

- Material Management and PlanningDocument6 pagesMaterial Management and PlanningDr.Rachanaa DateyNo ratings yet

- New RHFL Schemes & Forms - May 2022Document36 pagesNew RHFL Schemes & Forms - May 2022Surya PmlNo ratings yet

- HLF161 CTSFinancingAffordableHousingProgram V04Document6 pagesHLF161 CTSFinancingAffordableHousingProgram V04Ron HenleyNo ratings yet

- Growth and Trade: Multiple Choice QuestionsDocument20 pagesGrowth and Trade: Multiple Choice QuestionsMian NomiNo ratings yet

- In-Company Training BrochureDocument1 pageIn-Company Training BrochureRabia JamilNo ratings yet

- (I) Price/ Earning Ratio MethodDocument6 pages(I) Price/ Earning Ratio MethodCHIA MIN LIEWNo ratings yet

- 1.1. Definition of Economics: Oikonomia Which MeansDocument52 pages1.1. Definition of Economics: Oikonomia Which MeansSã MïNo ratings yet