You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Activation Plan For TransportersDocument29 pagesActivation Plan For Transportershimanshu BHATT100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2022 03 02 v1 EAF J-004987 - Corporate Profile Feb 2022 UpdateDocument38 pages2022 03 02 v1 EAF J-004987 - Corporate Profile Feb 2022 UpdateEduardo FilgueirasNo ratings yet

- Part IV: A Behavioral Perspective Chapter 7: Markets and ProfitDocument29 pagesPart IV: A Behavioral Perspective Chapter 7: Markets and ProfitJesslyn WongNo ratings yet

- McDonalds Franchise Disclosure DocumentDocument2 pagesMcDonalds Franchise Disclosure DocumentPrabjot Singh0% (1)

- Business Model Canvas - StrykerDocument9 pagesBusiness Model Canvas - StrykerVinudeep MalalurNo ratings yet

- Details Mode LawiDocument2 pagesDetails Mode LawiRasheed LawalNo ratings yet

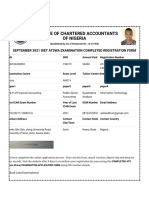

- The Institute of Chartered Accountants of Nigeria: Student's Examination StatusDocument1 pageThe Institute of Chartered Accountants of Nigeria: Student's Examination StatusRasheed LawalNo ratings yet

- Adesina Islamiyah Mojirade: 21, Ojurayo Street, Osogun, Alapere-Ketu Lagos 08064803170Document2 pagesAdesina Islamiyah Mojirade: 21, Ojurayo Street, Osogun, Alapere-Ketu Lagos 08064803170Rasheed LawalNo ratings yet

- Should Educational Institutions Pay Tax (Tax Seminar)Document20 pagesShould Educational Institutions Pay Tax (Tax Seminar)Rasheed LawalNo ratings yet

- Citn Presentation DR Olusegun Omisakin 2021Document12 pagesCitn Presentation DR Olusegun Omisakin 2021Rasheed LawalNo ratings yet

- Mental Health Awareness For Tax ProfessionalsDocument33 pagesMental Health Awareness For Tax ProfessionalsRasheed LawalNo ratings yet

- Tax Quiz FormDocument2 pagesTax Quiz FormRasheed LawalNo ratings yet

- Challenges and Prospects of Tax DigitisationDocument2 pagesChallenges and Prospects of Tax DigitisationRasheed LawalNo ratings yet

- Tax Appeal Tribunal 2Document3 pagesTax Appeal Tribunal 2Rasheed LawalNo ratings yet

- 2019-2020 MakeupDocument4 pages2019-2020 MakeupRasheed LawalNo ratings yet

- Towards The Digitisation of The Nigerian Tax Administration Challenges and Prospects-1Document7 pagesTowards The Digitisation of The Nigerian Tax Administration Challenges and Prospects-1Rasheed LawalNo ratings yet

- Ayinde Wasiu: Students' Professional Bureau of Accountancy O.A.UDocument1 pageAyinde Wasiu: Students' Professional Bureau of Accountancy O.A.URasheed LawalNo ratings yet

- ACC 214 (Management Accounting)Document31 pagesACC 214 (Management Accounting)Rasheed LawalNo ratings yet

- Expected Value Questions Example 1: RequiredDocument5 pagesExpected Value Questions Example 1: RequiredRasheed LawalNo ratings yet

- TIS Existing Members DatabaseDocument2 pagesTIS Existing Members DatabaseRasheed LawalNo ratings yet

- Solution Documentation - AI FOR ENERGYDocument54 pagesSolution Documentation - AI FOR ENERGYRasheed LawalNo ratings yet

- Partnership 9Document27 pagesPartnership 9Rasheed LawalNo ratings yet

- Intro To Stat Acc 233Document3 pagesIntro To Stat Acc 233Rasheed LawalNo ratings yet

- Tax Appeal TribunalDocument4 pagesTax Appeal TribunalRasheed LawalNo ratings yet

- Sources of Capital: Term Structure of FundsDocument5 pagesSources of Capital: Term Structure of FundsRasheed LawalNo ratings yet

- A Marketing Research of Vindosa CorporationDocument38 pagesA Marketing Research of Vindosa CorporationRodysa Ann Salvador CaburatanNo ratings yet

- A Study of Prefrences of The Investors For Investment in Mutual FundDocument28 pagesA Study of Prefrences of The Investors For Investment in Mutual Fundyogesh DivechaNo ratings yet

- Computer Consulting Business PlanDocument25 pagesComputer Consulting Business Planvirgo_17riteshNo ratings yet

- Ganesh Project OriginalDocument31 pagesGanesh Project OriginalAshutosh JadhavNo ratings yet

- Test Bank For Consumer Behaviour Buying Having and Being Sixth Canadian Edition 6 e 6th Edition Michael R Solomon Katherine White Darren DahlDocument14 pagesTest Bank For Consumer Behaviour Buying Having and Being Sixth Canadian Edition 6 e 6th Edition Michael R Solomon Katherine White Darren DahlJoel Slama100% (30)

- AfricArena 2019 Start-Ups PortfolioDocument89 pagesAfricArena 2019 Start-Ups PortfolioAdamNo ratings yet

- SkibidiDocument30 pagesSkibidispaghettisaucerersNo ratings yet

- Final Report Submission by Agung M.B. SiagianDocument27 pagesFinal Report Submission by Agung M.B. SiagianagungNo ratings yet

- Lirio de AguaDocument32 pagesLirio de AguaDarlianne Klyne BayerNo ratings yet

- Areas and Location Exposed To HazardsDocument16 pagesAreas and Location Exposed To HazardsGLADYS OLIVEROSNo ratings yet

- Week 1Document3 pagesWeek 1khaiNo ratings yet

- Millennials SegmentationDocument26 pagesMillennials SegmentationHarold Q. GardonNo ratings yet

- T J Nyambishi 47491 Week 4Document11 pagesT J Nyambishi 47491 Week 4takuejoshNo ratings yet

- Chitrangini S - OstDocument37 pagesChitrangini S - OstHarish VamananNo ratings yet

- 6.1 Market Failure and The Role of Government - Socially Efficient and Inefficient Market Outcomes PDFDocument5 pages6.1 Market Failure and The Role of Government - Socially Efficient and Inefficient Market Outcomes PDFfbbr gehe100% (1)

- Research 1 3Document14 pagesResearch 1 3Joel ManioNo ratings yet

- Product and Brand ManagementDocument328 pagesProduct and Brand ManagementfitsumNo ratings yet

- Introduction To Business Plan PreparationDocument4 pagesIntroduction To Business Plan Preparationvernadell2109No ratings yet

- Principles - of - Sustainable - Finance - (Part - II - Sustainability S - Challenges - To - Corporates)Document33 pagesPrinciples - of - Sustainable - Finance - (Part - II - Sustainability S - Challenges - To - Corporates)SebastianCasanovaCastañedaNo ratings yet

- J.D Women'S College Patna: Export Procedure and DocumentationDocument45 pagesJ.D Women'S College Patna: Export Procedure and Documentationpriyanshu sinhaNo ratings yet

- Grow A Thriving Coaching BusinessDocument27 pagesGrow A Thriving Coaching BusinessGabriel SantanaNo ratings yet

- Unit - 1 Basic Concepts - Forms of Business Organization PDFDocument29 pagesUnit - 1 Basic Concepts - Forms of Business Organization PDFShreyash PardeshiNo ratings yet

- Target Market DropboxDocument2 pagesTarget Market Dropboxapi-534081687No ratings yet

- Chapter 17 Personal Selling and Direct Marketing StrategiesDocument12 pagesChapter 17 Personal Selling and Direct Marketing StrategiesMeconNo ratings yet

- Unit 4 MK01Document4 pagesUnit 4 MK01ankitankithumptyNo ratings yet