You might also like

- Appeal Procedures For Tax DISPUTES in Tanzania: 1. Tanzania Revenue Authority (TRA)Document4 pagesAppeal Procedures For Tax DISPUTES in Tanzania: 1. Tanzania Revenue Authority (TRA)Nasra KarenNo ratings yet

- Gulf Oil LubricantsDocument3 pagesGulf Oil Lubricantsmdfaizan.alamNo ratings yet

- 65 Luxurty Tax Rule 2009Document10 pages65 Luxurty Tax Rule 2009shanuNo ratings yet

- Recovery of Taxes Under MRA ActDocument8 pagesRecovery of Taxes Under MRA ActVidoushiNo ratings yet

- PART IV Income TaxDocument9 pagesPART IV Income TaxRahil SattarNo ratings yet

- Chapter - Composition Rules 1. Intimation For Composition LevyDocument4 pagesChapter - Composition Rules 1. Intimation For Composition LevyGuru SankarNo ratings yet

- VAT Refund ProcessDocument2 pagesVAT Refund Processamfipolitis100% (1)

- Cabinet Decision No 37 of 2017 On Executive Regulation On Excise TaxDocument16 pagesCabinet Decision No 37 of 2017 On Executive Regulation On Excise Taxtanveer369No ratings yet

- Examination Proper:: Tax Law Review Mid-Term ExaminationDocument9 pagesExamination Proper:: Tax Law Review Mid-Term ExaminationGRACENo ratings yet

- Commercial Tax Regulations EnglishDocument25 pagesCommercial Tax Regulations EnglishYeyint099No ratings yet

- Excise Tax Proclamation: Section OneDocument14 pagesExcise Tax Proclamation: Section OneTewfic SeidNo ratings yet

- Assessment Objection and AppealsDocument13 pagesAssessment Objection and AppealsisackoelleNo ratings yet

- Week 10Document8 pagesWeek 10Victor LimNo ratings yet

- PP 80 2007Document22 pagesPP 80 2007davidwijaya1986No ratings yet

- Central Excise ActDocument8 pagesCentral Excise ActSamartha Raj SinghNo ratings yet

- Return of Income - S 114 To 119Document4 pagesReturn of Income - S 114 To 119khanNo ratings yet

- Section 137 To 146aDocument11 pagesSection 137 To 146aSher DilNo ratings yet

- Kuwait IncomeTax Decree PDFDocument8 pagesKuwait IncomeTax Decree PDFChristian D. Orbe100% (1)

- Summary Law No. 7 - 2021 - Harmonize Regulations of TaxationDocument8 pagesSummary Law No. 7 - 2021 - Harmonize Regulations of Taxationtina SibagariangNo ratings yet

- Penalty & Appeal (Chapter 19)Document13 pagesPenalty & Appeal (Chapter 19)Fahim Shahriar MozumderNo ratings yet

- Excise Tax Proclamation No 307 2002Document22 pagesExcise Tax Proclamation No 307 2002Temesgen EndalewNo ratings yet

- TaxationBarQ26A TaxRemediesDocument32 pagesTaxationBarQ26A TaxRemediesCire Gee100% (1)

- Is Criminal Violations Under Tax Laws Subject To Compromised Penalty Be Extinguished Upon Payment ThereofDocument3 pagesIs Criminal Violations Under Tax Laws Subject To Compromised Penalty Be Extinguished Upon Payment ThereofAnonymous MmvnEs5No ratings yet

- Andhra Pradesh Labour Welfare Fund Rules, 1988 PDFDocument5 pagesAndhra Pradesh Labour Welfare Fund Rules, 1988 PDFneohorizonsNo ratings yet

- TaxationBarQ26A TaxRemediesDocument32 pagesTaxationBarQ26A TaxRemediesjuneson agustinNo ratings yet

- ITAT Appeal Procedure FunctionsDocument4 pagesITAT Appeal Procedure FunctionsRuhul AminNo ratings yet

- Taxguru - In-Considerable Points For Staying of Income Tax DemandDocument9 pagesTaxguru - In-Considerable Points For Staying of Income Tax DemandAmit TyagiNo ratings yet

- City Corp TaxDocument13 pagesCity Corp TaxMuktar Hossain Chowdhury100% (1)

- Grounds of AppealDocument12 pagesGrounds of AppealIRTribunalNo ratings yet

- Notes in Taxation IIDocument6 pagesNotes in Taxation IIJoe BuenoNo ratings yet

- Q.18.Write Down The Procedure of Making An Appeal To Commissioner Appeal and Appeal To Appellate TribunalDocument5 pagesQ.18.Write Down The Procedure of Making An Appeal To Commissioner Appeal and Appeal To Appellate Tribunalatia khanNo ratings yet

- 0 Interpretation Note 15Document6 pages0 Interpretation Note 15pb41No ratings yet

- IncomeTaxLaw PDFDocument85 pagesIncomeTaxLaw PDFaccountNo ratings yet

- VAT and SD Rules 2016 EnglishDocument59 pagesVAT and SD Rules 2016 EnglishSadia Yasmin100% (3)

- The Value Added Tax and Supplementary Duty Rules, 2016Document61 pagesThe Value Added Tax and Supplementary Duty Rules, 2016Naimul KaderNo ratings yet

- Advance Ruling CustomDocument3 pagesAdvance Ruling Customrahulkapur87No ratings yet

- 132Document3 pages132Manoj KumarNo ratings yet

- 23 of 2011Document9 pages23 of 2011FelicianFernandopulleNo ratings yet

- Answer To Assignment A&bDocument3 pagesAnswer To Assignment A&bAmbe YanickNo ratings yet

- All About Appeal Before Commissioner of Income-Tax (Appeals)Document14 pagesAll About Appeal Before Commissioner of Income-Tax (Appeals)Jating JamkhandiNo ratings yet

- The New Income Tax Chapter 13: COLLECTION of Tax: PrintDocument4 pagesThe New Income Tax Chapter 13: COLLECTION of Tax: PrintzeeshanshahbazNo ratings yet

- Lascona Land Co., Inc. v. CIRDocument2 pagesLascona Land Co., Inc. v. CIRAron Lobo100% (1)

- Lascona vs. CIR (TAX)Document4 pagesLascona vs. CIR (TAX)Teff QuibodNo ratings yet

- Lascona Land Vs CIRDocument2 pagesLascona Land Vs CIRJOHN SPARKSNo ratings yet

- Finals Personal Study Guide Tax2Document116 pagesFinals Personal Study Guide Tax2TeacherEliNo ratings yet

- Appeals: © The Institute of Chartered Accountants of IndiaDocument16 pagesAppeals: © The Institute of Chartered Accountants of IndiaJitendra VernekarNo ratings yet

- Sub-Clause (Iii), (Iv), (V) and (Vi) of Clause (B) of Sub-Section (1) of Section 114Document4 pagesSub-Clause (Iii), (Iv), (V) and (Vi) of Clause (B) of Sub-Section (1) of Section 114Umair IftikharNo ratings yet

- Caltex Vs Commissioner 208 SCRA 755Document2 pagesCaltex Vs Commissioner 208 SCRA 755aldinNo ratings yet

- Cabinet Resolution No 40 of 2017 On Administrative Penalties For ViolationDocument7 pagesCabinet Resolution No 40 of 2017 On Administrative Penalties For ViolationSQNo ratings yet

- Bpo AgreementDocument19 pagesBpo AgreementAnkur NigamNo ratings yet

- FILE 20200812 175916 Annex B en PDFDocument19 pagesFILE 20200812 175916 Annex B en PDFThu Tuyen ThaiNo ratings yet

- Advance Rulings: AnswerDocument4 pagesAdvance Rulings: AnswervaibhavNo ratings yet

- Stay ApplicationsDocument8 pagesStay ApplicationsSHIVJEE yadavNo ratings yet

- Ampongan SolmanDocument25 pagesAmpongan SolmanNikolina100% (2)

- Lascona Land CoDocument2 pagesLascona Land CoTheodore0176No ratings yet

- Judgment MUHAMMAD MUNIR PERACHA, J. - The Petitioners Were Served With Show-Cause NoticeDocument6 pagesJudgment MUHAMMAD MUNIR PERACHA, J. - The Petitioners Were Served With Show-Cause NoticeMohammad AhmadNo ratings yet

- Duty Free Philippines V BIRDocument3 pagesDuty Free Philippines V BIRFra Santos100% (1)

- 21 of 2011Document7 pages21 of 2011FelicianFernandopulleNo ratings yet

- Duty Free Philippines V BIRDocument4 pagesDuty Free Philippines V BIRTheodore0176No ratings yet

- JijjiirraDocument27 pagesJijjiirratatekNo ratings yet

- Maqaa Ogeesota Digrii 1ffaa Yunversiitii Wallaggaa 2015Document18 pagesMaqaa Ogeesota Digrii 1ffaa Yunversiitii Wallaggaa 2015tatekNo ratings yet

- Implementation Guidelines For Lateral Flow Urine LipoarabinomannanDocument71 pagesImplementation Guidelines For Lateral Flow Urine LipoarabinomannantatekNo ratings yet

- Chapter 02Document36 pagesChapter 02tatekNo ratings yet

- Chapter 06Document37 pagesChapter 06tatekNo ratings yet

- Xalayaa Waamicha Hospitaala HirnaaDocument4 pagesXalayaa Waamicha Hospitaala HirnaatatekNo ratings yet

- Chapter 05Document52 pagesChapter 05tatekNo ratings yet

- PP ACF AssignmentDocument22 pagesPP ACF AssignmenttatekNo ratings yet

- Chapter 04Document36 pagesChapter 04tatekNo ratings yet

- Hosp Fedh 1pdfDocument18 pagesHosp Fedh 1pdftatekNo ratings yet

- Ethiopian Hospital Alliance For Quality 4 Cycle Evidence Based Care (EBC) Project Document and Change PackageDocument50 pagesEthiopian Hospital Alliance For Quality 4 Cycle Evidence Based Care (EBC) Project Document and Change Packagetatek100% (18)

- Feedhii Qabeenya Namaa Godinaalee Kan Bara 2014Document15 pagesFeedhii Qabeenya Namaa Godinaalee Kan Bara 2014tatekNo ratings yet

- Chapter 03Document31 pagesChapter 03tatekNo ratings yet

- Strategic Implementation, Evaluation and ControllingDocument14 pagesStrategic Implementation, Evaluation and ControllingtatekNo ratings yet

- Capital Budgeting Processesfor Public Sector Development Projects Master ThesisDocument65 pagesCapital Budgeting Processesfor Public Sector Development Projects Master ThesistatekNo ratings yet

- Futures Valuation and Hedging: by Cheng Few Lee Joseph Finnerty John Lee Alice C Lee Donald WortDocument54 pagesFutures Valuation and Hedging: by Cheng Few Lee Joseph Finnerty John Lee Alice C Lee Donald WorttatekNo ratings yet

- A-01 Article ReviewDocument1 pageA-01 Article ReviewtatekNo ratings yet

- ADV. Cost24 MarchDocument63 pagesADV. Cost24 MarchtatekNo ratings yet

- Proclamation No 99 2005 Rural Land Use Payment and Agricultural Activities Income Tax AmendmentDocument10 pagesProclamation No 99 2005 Rural Land Use Payment and Agricultural Activities Income Tax AmendmenttatekNo ratings yet

- 8 MST Vol 7 No 13 Jan Jun 2017 Ayele Final Thesis For PublicationDocument21 pages8 MST Vol 7 No 13 Jan Jun 2017 Ayele Final Thesis For PublicationtatekNo ratings yet

- Aa Aa Aa AaDocument10 pagesAa Aa Aa AatatekNo ratings yet

- Proclamation NoDocument10 pagesProclamation NotatekNo ratings yet

- Crb84a5dddid2474989 BorrowerDocument13 pagesCrb84a5dddid2474989 BorrowerKaran SharmaNo ratings yet

- Neelam Dadasaheb JudgementDocument10 pagesNeelam Dadasaheb JudgementRajaram Vamanrao KamatNo ratings yet

- BayadogDocument1 pageBayadogStarlene PortilloNo ratings yet

- Samyu AgreementDocument16 pagesSamyu AgreementMEENA VEERIAHNo ratings yet

- D'Alembert's Solution of The Wave Equation. Characteristics: Advanced Engineering Mathematics, 10/e by Edwin KreyszigDocument43 pagesD'Alembert's Solution of The Wave Equation. Characteristics: Advanced Engineering Mathematics, 10/e by Edwin KreyszigElias Abou FakhrNo ratings yet

- Media Ethics NotesDocument2 pagesMedia Ethics NotesFreedom Doctama100% (1)

- Annual Income Tax ReturnDocument2 pagesAnnual Income Tax ReturnRAS ConsultancyNo ratings yet

- Sample of Notarial WillDocument3 pagesSample of Notarial WillJF Dan100% (1)

- The Performance of The Legazpi City Police Station in Rendering Police Services Calendar Year 2014-2016Document13 pagesThe Performance of The Legazpi City Police Station in Rendering Police Services Calendar Year 2014-2016Kiel Riñon EtcobanezNo ratings yet

- System Control Switch Board, ReplacementDocument23 pagesSystem Control Switch Board, ReplacementjoramiandrisoaNo ratings yet

- Na Fianna Tune BookDocument41 pagesNa Fianna Tune BookDavid LairsonNo ratings yet

- Chinese OCW Conversational Chinese WorkbookDocument283 pagesChinese OCW Conversational Chinese Workbookhnikol3945No ratings yet

- International Bond and Equity Market ExerciseDocument5 pagesInternational Bond and Equity Market ExerciseSylvia GynNo ratings yet

- Opentext Extended Ecm For Sap Successfactors Ce - HR ProcessesDocument69 pagesOpentext Extended Ecm For Sap Successfactors Ce - HR ProcessesflasancaNo ratings yet

- Sample Org ConstitutionDocument15 pagesSample Org ConstitutionBrianCarpioNo ratings yet

- Scope of Inspection For Ammonia TankDocument3 pagesScope of Inspection For Ammonia TankHamid MansouriNo ratings yet

- Shay Eshel - The Concept of The Elect Nation in Byzantium (2018, Brill) PDFDocument234 pagesShay Eshel - The Concept of The Elect Nation in Byzantium (2018, Brill) PDFMarko DabicNo ratings yet

- Aurora Pump VT (FM) PDFDocument30 pagesAurora Pump VT (FM) PDFRizalNo ratings yet

- Ais Fraud-Case StudyDocument3 pagesAis Fraud-Case StudyErica AlimpolosNo ratings yet

- Class Action Lawsuit Against Johnson & JohnsonDocument49 pagesClass Action Lawsuit Against Johnson & JohnsonAnonymous GF8PPILW575% (4)

- Suraya Binti Hussin: Kota Kinabalu - T1 (BKI)Document2 pagesSuraya Binti Hussin: Kota Kinabalu - T1 (BKI)Sulaiman SyarifuddinNo ratings yet

- Oracle SOA 11.1.1.5.0 Admin GuideDocument698 pagesOracle SOA 11.1.1.5.0 Admin GuideConnie WallNo ratings yet

- POCSODocument12 pagesPOCSOPragya RaniNo ratings yet

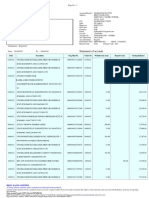

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHiten AhirNo ratings yet

- 10 Can The Little Horn Change God's LawDocument79 pages10 Can The Little Horn Change God's LawJayhia Malaga JarlegaNo ratings yet

- Commercial Banking Operations:: Types of Commercial BanksDocument6 pagesCommercial Banking Operations:: Types of Commercial BanksKhyell PayasNo ratings yet

- Newton 2nd and 3rd Laws Chapter 4-3Document20 pagesNewton 2nd and 3rd Laws Chapter 4-3Jams FlorendoNo ratings yet

- Ise II Writing A Formal Letter OfaDocument1 pageIse II Writing A Formal Letter OfaCristina ParraNo ratings yet

- Economy of VeitnamDocument17 pagesEconomy of VeitnamPriyanshi LohaniNo ratings yet

- United States of America Ex Rel. Maria Horta v. John Deyoung, Warden Passaic County Jail, 523 F.2d 807, 3rd Cir. (1975)Document5 pagesUnited States of America Ex Rel. Maria Horta v. John Deyoung, Warden Passaic County Jail, 523 F.2d 807, 3rd Cir. (1975)Scribd Government DocsNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- The Payroll Book: A Guide for Small Businesses and StartupsFrom EverandThe Payroll Book: A Guide for Small Businesses and StartupsRating: 5 out of 5 stars5/5 (1)

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionRating: 5 out of 5 stars5/5 (27)

- Bookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesFrom EverandBookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesNo ratings yet

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- Tax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthFrom EverandTax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthNo ratings yet

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012From EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012No ratings yet

- Make Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionFrom EverandMake Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionNo ratings yet

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- S Corporation ESOP Traps for the UnwaryFrom EverandS Corporation ESOP Traps for the UnwaryNo ratings yet

- Taxes Have Consequences: An Income Tax History of the United StatesFrom EverandTaxes Have Consequences: An Income Tax History of the United StatesNo ratings yet