You might also like

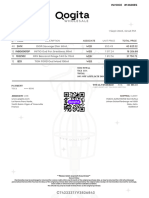

- Qogita INVOICEDocument1 pageQogita INVOICEalmutamidhakimNo ratings yet

- Syllabus Corso Strategia 2020-21Document7 pagesSyllabus Corso Strategia 2020-21Enri GjondrekajNo ratings yet

- Accounting For Leases: Chapter Learning ObjectivesDocument48 pagesAccounting For Leases: Chapter Learning ObjectivesRenabelle CagaNo ratings yet

- Marketing Plan For Glucose BiscuitsDocument17 pagesMarketing Plan For Glucose BiscuitsWoody Kin0% (1)

- Module - 1 Corporate Governance - OverviewDocument42 pagesModule - 1 Corporate Governance - OverviewAbhishekNo ratings yet

- Prelims - Good Governance and Social ResponsibilityDocument4 pagesPrelims - Good Governance and Social ResponsibilityGill AdrienneNo ratings yet

- Private Sector Opinion Issue 17: A Corporate Governance Model: Building Responsible Boards and Sustainable BusinessesDocument16 pagesPrivate Sector Opinion Issue 17: A Corporate Governance Model: Building Responsible Boards and Sustainable BusinesseshinahameedNo ratings yet

- Unit - 3 Auditing and Corporate Governance.Document20 pagesUnit - 3 Auditing and Corporate Governance.laxmisruti123No ratings yet

- Good Corporate Governance An Ideawhose Time Has ComeDocument39 pagesGood Corporate Governance An Ideawhose Time Has ComeRuchita Nathani BhagatNo ratings yet

- The Pillars of Good Corporate GovernanceDocument14 pagesThe Pillars of Good Corporate GovernancetafadzwachinazNo ratings yet

- Corporate Social ResponsibilityDocument7 pagesCorporate Social ResponsibilitydhafNo ratings yet

- And Ethical Issues: Assignment of SocialDocument17 pagesAnd Ethical Issues: Assignment of Socialbhumika nagiNo ratings yet

- Overview of Corporate GovernanceDocument22 pagesOverview of Corporate GovernanceAnonymous nTxB1EPvNo ratings yet

- IntroductionDocument48 pagesIntroductionlindaNo ratings yet

- Corporate Governance - Is A Myth or RealityDocument15 pagesCorporate Governance - Is A Myth or Realitymehta_vikram19868766100% (1)

- MBA 402 ReportDocument6 pagesMBA 402 ReportawasthisailesNo ratings yet

- Student Name: Christian Steele STUDENT ID: 816020005Document4 pagesStudent Name: Christian Steele STUDENT ID: 816020005Christian SteeleNo ratings yet

- Auditing It Governance ControlsDocument29 pagesAuditing It Governance ControlsJaira MoradaNo ratings yet

- Mba FinalDocument6 pagesMba FinalMarie LacapNo ratings yet

- What Is Corporate Governance & ExampleDocument8 pagesWhat Is Corporate Governance & ExampleeliasNo ratings yet

- mgt209 Chapter 1Document34 pagesmgt209 Chapter 1Nat NatNo ratings yet

- Corporate Governance: Gayatri Iyer MBADocument18 pagesCorporate Governance: Gayatri Iyer MBARajiv LamichhaneNo ratings yet

- What Is Corporate GovernanceDocument13 pagesWhat Is Corporate GovernanceReniva KhingNo ratings yet

- mgmt3035 FinalsDocument4 pagesmgmt3035 FinalsIsmadth2918388No ratings yet

- Mgmt3035 FinalsDocument4 pagesMgmt3035 FinalsIsmadth2918388No ratings yet

- GBRIDocument4 pagesGBRIWildrian MacasinagNo ratings yet

- CG Topic 1.2Document7 pagesCG Topic 1.2Fong Shi MinNo ratings yet

- 1 2 3 Corporate Goverance NOTESDocument51 pages1 2 3 Corporate Goverance NOTESomkargaikwad0077No ratings yet

- Corporate GovernanceDocument20 pagesCorporate GovernanceKrizha WatanabeNo ratings yet

- Unit 1: Why Corporate Governance?Document100 pagesUnit 1: Why Corporate Governance?Vivek bishtNo ratings yet

- Corp. Governance 1Document11 pagesCorp. Governance 1ridhiNo ratings yet

- GGSR PrelimDocument102 pagesGGSR PrelimTintin Ruiz0% (2)

- Corporate Governance - A Conceptual AnalysisDocument36 pagesCorporate Governance - A Conceptual Analysissameer_kiniNo ratings yet

- Purpose and Benefits of Good GovernanceDocument5 pagesPurpose and Benefits of Good GovernanceDecereen Pineda RodriguezaNo ratings yet

- Corporate Governance Using Balanced ScorecardDocument11 pagesCorporate Governance Using Balanced Scorecardapi-3820836100% (2)

- Unit - 1 INTRODUCTIONDocument10 pagesUnit - 1 INTRODUCTIONYashika GuptaNo ratings yet

- 202004181917242491nlbharti CORPORATE GOVERNANCEDocument26 pages202004181917242491nlbharti CORPORATE GOVERNANCEAnurag SinghNo ratings yet

- Corporate GovernanceDocument9 pagesCorporate Governancepallab jyoti gogoiNo ratings yet

- Group 1the Corporation and Corporate GovernanceDocument12 pagesGroup 1the Corporation and Corporate GovernanceKezNo ratings yet

- GCG Role AccountanDocument23 pagesGCG Role AccountanAgusSafriTanjungNo ratings yet

- Corporate GovernanceDocument8 pagesCorporate GovernanceKrishnateja YarrapatruniNo ratings yet

- Corporate GovernanceDocument7 pagesCorporate Governancemehakrotra256No ratings yet

- Final Exams in GG&CSRDocument4 pagesFinal Exams in GG&CSRDiether ManaloNo ratings yet

- Corporate Governance AssignmentDocument10 pagesCorporate Governance AssignmentJon BradNo ratings yet

- Ba 8 Quiz 3 - Diaz BausteDocument49 pagesBa 8 Quiz 3 - Diaz BausteCarmen Diaz BausteNo ratings yet

- 123 Business Ethics and Corporate Governance Uz 123Document145 pages123 Business Ethics and Corporate Governance Uz 123cctmasekesaNo ratings yet

- Topic:-Corporate Governance: Assignment ofDocument9 pagesTopic:-Corporate Governance: Assignment oftauh_ahmadNo ratings yet

- Project On Corporate GovernanceDocument22 pagesProject On Corporate GovernancePallavi PradhanNo ratings yet

- Dsdasd Sfs Fsadf PDF DF D 2020Document56 pagesDsdasd Sfs Fsadf PDF DF D 2020mihiborceastefanNo ratings yet

- P1 (Corporate Governance, Risks & Ethics)Document34 pagesP1 (Corporate Governance, Risks & Ethics)Šyed FarîsNo ratings yet

- Week 8 Questions For EthicsDocument3 pagesWeek 8 Questions For EthicsjimNo ratings yet

- Module 8Document4 pagesModule 8tabarnerorene17No ratings yet

- Corporate GovernanceDocument30 pagesCorporate GovernanceBaraka ElikanaNo ratings yet

- Corporate Governance FinalDocument31 pagesCorporate Governance FinalNakul MehtaNo ratings yet

- Thesis Good Corporate GovernanceDocument6 pagesThesis Good Corporate Governanceamandahengelfargo100% (2)

- Corporate Governance of WiproDocument34 pagesCorporate Governance of WiproMohammad Imran100% (2)

- Corporate Governance: Acctg 216: Governance, Business Ethics, Risk Management and Internal ControlDocument67 pagesCorporate Governance: Acctg 216: Governance, Business Ethics, Risk Management and Internal ControlGilner PomarNo ratings yet

- Corporate GovernanceDocument25 pagesCorporate GovernanceSameer Patro0% (1)

- BS 410 Notes 2021Document61 pagesBS 410 Notes 2021Naison Shingirai PfavayiNo ratings yet

- Business Ethics: Assignment OnDocument9 pagesBusiness Ethics: Assignment OnSomesh KumarNo ratings yet

- Investing in Transformational Governance Business BriefDocument18 pagesInvesting in Transformational Governance Business Briefras defgNo ratings yet

- Sustainability Reporting Frameworks, Standards, Instruments, and Regulations: A Guide for Sustainable EntrepreneursFrom EverandSustainability Reporting Frameworks, Standards, Instruments, and Regulations: A Guide for Sustainable EntrepreneursNo ratings yet

- Corporate Governance: Ensuring Accountability and TransparencyFrom EverandCorporate Governance: Ensuring Accountability and TransparencyNo ratings yet

- Strategy and Organization: Team 19Document12 pagesStrategy and Organization: Team 19Enri GjondrekajNo ratings yet

- 20 - Capacity StrategyDocument28 pages20 - Capacity StrategyEnri GjondrekajNo ratings yet

- 17 Data AnalysisDocument64 pages17 Data AnalysisEnri GjondrekajNo ratings yet

- Schemi StrategyDocument71 pagesSchemi StrategyEnri GjondrekajNo ratings yet

- 18 Operations StrategyDocument30 pages18 Operations StrategyEnri GjondrekajNo ratings yet

- Analysis and Management of Production SystemDocument50 pagesAnalysis and Management of Production SystemEnri GjondrekajNo ratings yet

- 13 - Line Analysis - With - SolutionsDocument15 pages13 - Line Analysis - With - SolutionsEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 14: Discrete Event SimulationDocument47 pagesAnalysis and Management of Production System: Lesson 14: Discrete Event SimulationEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 19: Operations PerformancesDocument23 pagesAnalysis and Management of Production System: Lesson 19: Operations PerformancesEnri GjondrekajNo ratings yet

- 16 Industry 4.0Document72 pages16 Industry 4.0Enri GjondrekajNo ratings yet

- 15 Information SystemsDocument57 pages15 Information SystemsEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 11: Variability of Processing TimeDocument33 pagesAnalysis and Management of Production System: Lesson 11: Variability of Processing TimeEnri GjondrekajNo ratings yet

- 10 Benchmarking With SolutionsDocument57 pages10 Benchmarking With SolutionsEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 12: Single Workstation AnalysisDocument44 pagesAnalysis and Management of Production System: Lesson 12: Single Workstation AnalysisEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 07: Process Representation - BPMN DiagramDocument48 pagesAnalysis and Management of Production System: Lesson 07: Process Representation - BPMN DiagramEnri GjondrekajNo ratings yet

- 02 Operative Structure Product TreeDocument17 pages02 Operative Structure Product TreeEnri GjondrekajNo ratings yet

- Analysis and Management of Production Systems: Lesson 03: Working SequenceDocument27 pagesAnalysis and Management of Production Systems: Lesson 03: Working SequenceEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 09: Process Representation - IDEF0 DiagramDocument21 pagesAnalysis and Management of Production System: Lesson 09: Process Representation - IDEF0 DiagramEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 06: Process Representation - Flow Chart and UML Activity DiagramDocument32 pagesAnalysis and Management of Production System: Lesson 06: Process Representation - Flow Chart and UML Activity DiagramEnri GjondrekajNo ratings yet

- VW BylawsDocument16 pagesVW BylawsEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 05: Organizational ArrangementDocument21 pagesAnalysis and Management of Production System: Lesson 05: Organizational ArrangementEnri GjondrekajNo ratings yet

- Analysis and Management of Production System: Lesson 01: IntroductionDocument15 pagesAnalysis and Management of Production System: Lesson 01: IntroductionEnri GjondrekajNo ratings yet

- 04 Layout Analysis NewDocument57 pages04 Layout Analysis NewEnri GjondrekajNo ratings yet

- Civil Law and Common Law - SmirneDocument17 pagesCivil Law and Common Law - SmirneEnri GjondrekajNo ratings yet

- 05 - BL - What Is Corporate LawDocument37 pages05 - BL - What Is Corporate LawEnri GjondrekajNo ratings yet

- SUMMARY OF BUSINESS LAW FedeDocument17 pagesSUMMARY OF BUSINESS LAW FedeEnri GjondrekajNo ratings yet

- Adrian Velasco BejaranoDocument8 pagesAdrian Velasco BejaranoMadhu ITNo ratings yet

- B207A Powerpoint - Week 3Document20 pagesB207A Powerpoint - Week 3syed abdalNo ratings yet

- 3 3 3-OHSMS-LAC - Delelgate Activity Manual-20-JULY-2020Document33 pages3 3 3-OHSMS-LAC - Delelgate Activity Manual-20-JULY-2020walidNo ratings yet

- Bab 14. Jawaban Contoh SoalDocument2 pagesBab 14. Jawaban Contoh SoalVanaNo ratings yet

- Business Plan Insurance BrokerDocument17 pagesBusiness Plan Insurance Brokermotsisi.theregoNo ratings yet

- Organizational Study On Jindal Saw LTDDocument32 pagesOrganizational Study On Jindal Saw LTDAlsafar Travels75% (4)

- The Role of An Auditor in The Achievement of Organisational ObjectivesDocument68 pagesThe Role of An Auditor in The Achievement of Organisational ObjectivesShuaib OLAJIRENo ratings yet

- News Digest: Friday, April 30, 2021 Vol. 53, No. 12614Document32 pagesNews Digest: Friday, April 30, 2021 Vol. 53, No. 12614Bobby PoonNo ratings yet

- 2.1 - CV Lucian BuzduganDocument5 pages2.1 - CV Lucian Buzduganno-replyNo ratings yet

- Networking and EntrepreneurshipDocument14 pagesNetworking and EntrepreneurshipKshitishNo ratings yet

- Investment Avenues Available in BangladeshDocument16 pagesInvestment Avenues Available in BangladeshangelNo ratings yet

- FinQuiz - CFA Level 3, June, 2019 - Formula SheetDocument16 pagesFinQuiz - CFA Level 3, June, 2019 - Formula SheetmkNo ratings yet

- Annual Report 2019-20 PDFDocument272 pagesAnnual Report 2019-20 PDFpushpraj rastogiNo ratings yet

- Deveshi Roy - WAC Assessment 1Document3 pagesDeveshi Roy - WAC Assessment 1ajNo ratings yet

- 1200SUBWAYACCOUNTHUBDocument22 pages1200SUBWAYACCOUNTHUBliveyourbestlifehoNo ratings yet

- Assignment Doc Paper P2 Performance Management 17052016044853Document14 pagesAssignment Doc Paper P2 Performance Management 17052016044853hyp siinNo ratings yet

- Advertising FinalsDocument1 pageAdvertising FinalsLeslie Ann Elazegui UntalanNo ratings yet

- Types of Business EntitiesDocument4 pagesTypes of Business EntitiesAini SyafiqahNo ratings yet

- How To Establish Meaningful and Measurable KPIs For Your RPA ImplementationDocument4 pagesHow To Establish Meaningful and Measurable KPIs For Your RPA ImplementationAdnan FarooqNo ratings yet

- Agency Costs of Free Cash FlowDocument3 pagesAgency Costs of Free Cash FlowHarsh MaheshwariNo ratings yet

- Financial DerivativesDocument64 pagesFinancial DerivativesKirabpalNo ratings yet

- Employee Turnover ProjectDocument94 pagesEmployee Turnover ProjectDiddu PerfectNo ratings yet

- Business Practice Analysis PitchingDocument20 pagesBusiness Practice Analysis PitchingAmadea SutandiNo ratings yet

- Kantar Worldpanel Division FMCG Monitor Full Year 2021 enDocument13 pagesKantar Worldpanel Division FMCG Monitor Full Year 2021 enNguyen LinhNo ratings yet

- Principles of Marketing Quarter 1-Week 5 Lesson 1.1: What I Need To KnowDocument8 pagesPrinciples of Marketing Quarter 1-Week 5 Lesson 1.1: What I Need To KnowGlychalyn Abecia 23No ratings yet

- SustainabilityDocument19 pagesSustainabilityZuzunishNo ratings yet

- Thayer Van Thinh Phat Group and AccountabilityDocument2 pagesThayer Van Thinh Phat Group and AccountabilityCarlyle Alan ThayerNo ratings yet