You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Assignment Chapter 3Document3 pagesAssignment Chapter 3Beatrice BallabioNo ratings yet

- Training & Developing EmployeesDocument25 pagesTraining & Developing EmployeesPooja MehraNo ratings yet

- Demand Supply EquilibriumDocument53 pagesDemand Supply EquilibriumPooja MehraNo ratings yet

- Session 7-8 Research Questions and HypothesisDocument43 pagesSession 7-8 Research Questions and HypothesisPooja MehraNo ratings yet

- Session 5-6 Formulating Research ProblemDocument26 pagesSession 5-6 Formulating Research ProblemPooja MehraNo ratings yet

- TCS Strategy ProjectDocument5 pagesTCS Strategy ProjectPooja MehraNo ratings yet

- Sampling and Sample SizeDocument32 pagesSampling and Sample SizePooja MehraNo ratings yet

- Iilm Graduate School of Management: PLP Group:9 Managerial Economics Topic:Hospitality IndustryDocument16 pagesIilm Graduate School of Management: PLP Group:9 Managerial Economics Topic:Hospitality IndustryPooja MehraNo ratings yet

- Session 10,11,12 Financial Analysis - Performance EvaluationDocument12 pagesSession 10,11,12 Financial Analysis - Performance EvaluationPooja MehraNo ratings yet

- Session 14 & 15 Financial Analysis - The Determinents of PerformanceDocument15 pagesSession 14 & 15 Financial Analysis - The Determinents of PerformancePooja MehraNo ratings yet

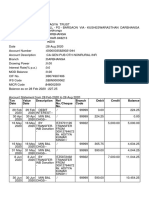

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceAditya KumarNo ratings yet

- Act AssignmentDocument33 pagesAct AssignmentLabib KhanNo ratings yet

- CER - Propeller Overhaul - CAAP Memo AdditionalDocument7 pagesCER - Propeller Overhaul - CAAP Memo Additionalbilly ray bationNo ratings yet

- Chapter 8 Alternative Costing SystemsDocument21 pagesChapter 8 Alternative Costing SystemsSaad KhanNo ratings yet

- A) B) C) D) E) A) B) C) D) E) A) B) C) D) E) A) B) C) D) E)Document3 pagesA) B) C) D) E) A) B) C) D) E) A) B) C) D) E) A) B) C) D) E)Mharvie LorayaNo ratings yet

- Audit Working Papers ReceivablesDocument3 pagesAudit Working Papers ReceivablesKeith Joshua GabiasonNo ratings yet

- Pinnacle Online Undergrad Tutorials ProgramDocument28 pagesPinnacle Online Undergrad Tutorials ProgramDISEREE AMOR ATIENZANo ratings yet

- SMU MBA104 FINANCIAL AND MANAGEMENT ACCOUNTING Free Solved AssignmentDocument10 pagesSMU MBA104 FINANCIAL AND MANAGEMENT ACCOUNTING Free Solved Assignmentrahulverma251233% (3)

- Clover Park Technical College Fall 2013 Class ScheduleDocument57 pagesClover Park Technical College Fall 2013 Class ScheduleCloverParkTechNo ratings yet

- Solutions To Introduction To Electric CiDocument14 pagesSolutions To Introduction To Electric CiSiva KumarNo ratings yet

- Types of Accounting ErrorsDocument8 pagesTypes of Accounting ErrorsHassleBustNo ratings yet

- Chapter 15 Audit Reports OnDocument45 pagesChapter 15 Audit Reports OnfanchasticommsNo ratings yet

- Accounting 1 Study Guide-Review ActivityDocument15 pagesAccounting 1 Study Guide-Review ActivityKenver RegisNo ratings yet

- The Accounting Equation & Double EntryDocument13 pagesThe Accounting Equation & Double EntryJukunda Shikongo100% (1)

- AP.m 1401 Correction of ErrorsDocument12 pagesAP.m 1401 Correction of ErrorsMark Lord Morales Bumagat75% (4)

- 28 Cas 13 Cost Accounting Standard On Cost of Service Cost CentreDocument7 pages28 Cas 13 Cost Accounting Standard On Cost of Service Cost CentrekoshaleshwarNo ratings yet

- Amend IAS 12 May 2021 Deferred Tax ESDocument18 pagesAmend IAS 12 May 2021 Deferred Tax ESVillalva ChoqueNo ratings yet

- Concurrent Audit PDFDocument98 pagesConcurrent Audit PDFDekrouf SysNo ratings yet

- Cost 531 2021 AssignmentDocument10 pagesCost 531 2021 AssignmentWaylee CheroNo ratings yet

- QUIZDocument6 pagesQUIZHuỳnh Trúc PhươngNo ratings yet

- Knowledge Acquisition For Expert Systems in Accounting and Financial Problem DomainsDocument9 pagesKnowledge Acquisition For Expert Systems in Accounting and Financial Problem DomainsNajmi AimanNo ratings yet

- Job Analysis Report of An Engineering FirmDocument35 pagesJob Analysis Report of An Engineering FirmTarun Sharma0% (1)

- Creating and Understanding Financial StatementsDocument11 pagesCreating and Understanding Financial StatementseleNo ratings yet

- Chapter On CVP 2015 - Acc 2Document16 pagesChapter On CVP 2015 - Acc 2nur aqilah ridzuanNo ratings yet

- Reversing EntriesDocument4 pagesReversing EntriesCatherine GonzalesNo ratings yet

- STD 11 Book Keeping and Accountancy SolutionsDocument18 pagesSTD 11 Book Keeping and Accountancy SolutionsAnonymous DuNDBdNo ratings yet

- Construction Accounting and Financial ManagementDocument3 pagesConstruction Accounting and Financial ManagementSon Go HanNo ratings yet

- Module 1 5 AnswersDocument111 pagesModule 1 5 AnswersryanNo ratings yet

- Friendly Reminder e Mail TemplateDocument1 pageFriendly Reminder e Mail TemplateRoliNo ratings yet