You might also like

- UAE Salary Guide 2020 Cooper FitchDocument34 pagesUAE Salary Guide 2020 Cooper FitchEr Jyotirmaya DalaiNo ratings yet

- Cost of Goods Sold WorksheetDocument4 pagesCost of Goods Sold Worksheetbutch listangco100% (1)

- ISO14327 2004resistanceweldingDocument20 pagesISO14327 2004resistanceweldingEdNo ratings yet

- Activity 3Document5 pagesActivity 3Keith Joshua GabiasonNo ratings yet

- Strategic ManagementDocument45 pagesStrategic Managementsureh_mite_nitkyahoo100% (4)

- Solutions To Chapters 7 and 8 Problem SetsDocument21 pagesSolutions To Chapters 7 and 8 Problem SetsMuhammad Hasnain100% (1)

- Production Possibilities Frontier - WorksheetDocument2 pagesProduction Possibilities Frontier - WorksheetMr. Powers100% (2)

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaNo ratings yet

- Marketing of Pesticides and Its Effect on Agriculture in Nagpur DistrictDocument15 pagesMarketing of Pesticides and Its Effect on Agriculture in Nagpur DistrictAnil GowdaNo ratings yet

- Valuation Report of BPCLDocument35 pagesValuation Report of BPCLJobin JohnNo ratings yet

- Business Valuation Report of Bharat Petroleum Corporation Ltd by Anu M Lawrence and othersDocument24 pagesBusiness Valuation Report of Bharat Petroleum Corporation Ltd by Anu M Lawrence and othersJobin JohnNo ratings yet

- Blemishing GDP Quarterly ResultsDocument4 pagesBlemishing GDP Quarterly ResultsCritiNo ratings yet

- Employment Insurance Sytem (Eis) : VOLUME 4/2020 The Impact of Covid-19 On LoeDocument26 pagesEmployment Insurance Sytem (Eis) : VOLUME 4/2020 The Impact of Covid-19 On LoeunicornmfkNo ratings yet

- Budget 2020 21 Highlights Comments Deloittepk NoexpDocument98 pagesBudget 2020 21 Highlights Comments Deloittepk NoexpOwais WahidNo ratings yet

- Day 1 Room 2 Session 2 Health and TaxationDocument25 pagesDay 1 Room 2 Session 2 Health and TaxationJorge De VelazcoNo ratings yet

- Economic Report 5Document19 pagesEconomic Report 5Khoirunisa WulandariNo ratings yet

- Frb 8 Acctg for Fwl Waiver Rebate (Final)Document19 pagesFrb 8 Acctg for Fwl Waiver Rebate (Final)cheezhen5047No ratings yet

- Reading - Organización Mundial Del ComercioDocument11 pagesReading - Organización Mundial Del ComercioNúriaNo ratings yet

- Covid-19 Advent and Impact Assessment: Annex-IIIDocument8 pagesCovid-19 Advent and Impact Assessment: Annex-IIIAsaad AreebNo ratings yet

- BB Monetary Policy Outlook for Bangladesh GrowthDocument24 pagesBB Monetary Policy Outlook for Bangladesh GrowthPovon Chandra SutradarNo ratings yet

- UK Outlook 2020 FinalDocument38 pagesUK Outlook 2020 FinalMILENKA YSABEL UCEDA PUICONNo ratings yet

- Marred by Regulatory Scrutiny: Qiwi PLCDocument4 pagesMarred by Regulatory Scrutiny: Qiwi PLCRalph SuarezNo ratings yet

- HDFC Bank Research Presentation April 2020Document41 pagesHDFC Bank Research Presentation April 2020MohitNo ratings yet

- Linesight Middle East Handbook 2020 Sept. Update - DigitalDocument77 pagesLinesight Middle East Handbook 2020 Sept. Update - Digital黄磊No ratings yet

- DB Invonluntary SavingDocument13 pagesDB Invonluntary SavingpadullaNo ratings yet

- Problem 1-A Bank Reconciliation: Add/less: Book Errors P 900.00Document4 pagesProblem 1-A Bank Reconciliation: Add/less: Book Errors P 900.00Merry Kriss RiveraNo ratings yet

- X Compliance MergedDocument46 pagesX Compliance MergedAnnah Caponpon GalorNo ratings yet

- A Modern Mining Company: Michelle PoleDocument35 pagesA Modern Mining Company: Michelle PoleTimBarrowsNo ratings yet

- 2020 Budget PreviewDocument11 pages2020 Budget PreviewClaudium ClaudiusNo ratings yet

- VinaCapital 2021 Outlook PublicDocument13 pagesVinaCapital 2021 Outlook PublicTùng HoàngNo ratings yet

- SOK 2020 Annual ReportDocument158 pagesSOK 2020 Annual Reporttarikerkut44No ratings yet

- 4Q 2020 - Analyst Meeting (LONG FORM)Document80 pages4Q 2020 - Analyst Meeting (LONG FORM)Giang NguyenNo ratings yet

- Nishat Chunian Financial Ratios Analysis (2020 vs 2019Document6 pagesNishat Chunian Financial Ratios Analysis (2020 vs 2019maryamNo ratings yet

- Bukopin Rating Affirmed at "idADocument2 pagesBukopin Rating Affirmed at "idAAz CheNo ratings yet

- RAK Ceramics PJSC CFS Q2 2020 EnglishDocument34 pagesRAK Ceramics PJSC CFS Q2 2020 Englishahme farNo ratings yet

- COVID-19 Impact on Malaysian Banking IndustryDocument15 pagesCOVID-19 Impact on Malaysian Banking IndustryPei Qi ErNo ratings yet

- PH ECO OUTLOOK 2020 - Rev1.0Document15 pagesPH ECO OUTLOOK 2020 - Rev1.0Jonathan AguilarNo ratings yet

- Group F FIN201 Section 3Document27 pagesGroup F FIN201 Section 3Nayeem MahmudNo ratings yet

- Macroecon Micaspect of National Budget 2020Document15 pagesMacroecon Micaspect of National Budget 2020Md Joinal AbedinNo ratings yet

- Ira Shalini M. YbañezDocument5 pagesIra Shalini M. YbañezIra YbanezNo ratings yet

- Industrial Report: Our Professional Your SuccessDocument12 pagesIndustrial Report: Our Professional Your SuccessPhương Linh NguyễnNo ratings yet

- Downgrading Estimates On Higher Provisions Maintain BUY: Bank of The Philippine IslandsDocument8 pagesDowngrading Estimates On Higher Provisions Maintain BUY: Bank of The Philippine IslandsJNo ratings yet

- V G PLC C R: A Transforming IndustryDocument53 pagesV G PLC C R: A Transforming Industryamar jotNo ratings yet

- 15 Annual Report: ONGC Petro Additions LimitedDocument121 pages15 Annual Report: ONGC Petro Additions Limitedarjun SinghNo ratings yet

- Chap 3Document19 pagesChap 3Nagina MemonNo ratings yet

- How COVID-19 Affects Corporate Financial Performance and Corporate Valuation in Bangladesh: An Empirical StudyDocument8 pagesHow COVID-19 Affects Corporate Financial Performance and Corporate Valuation in Bangladesh: An Empirical StudyInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- TSX Sherf 2020Document140 pagesTSX Sherf 2020popoNo ratings yet

- CII BWR ReportDocument27 pagesCII BWR ReportBalakrishna DammatiNo ratings yet

- A Critical Review of Budget For The Fiscal Year 2017Document21 pagesA Critical Review of Budget For The Fiscal Year 2017Tanjil HossainNo ratings yet

- Financial Management Report on Alan Scott Industries and Polo Queen IndustrialDocument14 pagesFinancial Management Report on Alan Scott Industries and Polo Queen IndustrialApoorva Pattnaik0% (1)

- Management Discussion and Analysis: Statutory ReportsDocument2 pagesManagement Discussion and Analysis: Statutory ReportsBlueHexNo ratings yet

- Dealtracker-Q1 2020: Providing M&A and Private Equity Deal InsightsDocument15 pagesDealtracker-Q1 2020: Providing M&A and Private Equity Deal Insightsvikas@davimNo ratings yet

- Appendix 4D and Condensed Consolidated Interim Financial Statements 9 Spokes International Limited 30 September 2020Document33 pagesAppendix 4D and Condensed Consolidated Interim Financial Statements 9 Spokes International Limited 30 September 2020jenny smithNo ratings yet

- Rush of Expenditure in The Last Quarter of Financial Year 2019-20 - Central Government Employees NewsDocument2 pagesRush of Expenditure in The Last Quarter of Financial Year 2019-20 - Central Government Employees NewsbimlapalNo ratings yet

- Credit Analysis of Premier Foods PLC - Sample 1Document14 pagesCredit Analysis of Premier Foods PLC - Sample 1BethelNo ratings yet

- Annual Report FY2020Document424 pagesAnnual Report FY2020SAGAR KASERANo ratings yet

- MM Is A Wholly-Owned Subsidiary of Injap Investments Inc., Which Also Owns 35% of Doubledragon Properties CorpDocument4 pagesMM Is A Wholly-Owned Subsidiary of Injap Investments Inc., Which Also Owns 35% of Doubledragon Properties CorpTrisha Mae Mendoza MacalinoNo ratings yet

- IndiaEconomicsOverheating090207 MF PDFDocument4 pagesIndiaEconomicsOverheating090207 MF PDFdidwaniasNo ratings yet

- Global Industries Outlook 2021 - 2020-12-18Document101 pagesGlobal Industries Outlook 2021 - 2020-12-18trungtruc999No ratings yet

- The Saudi Economy in 2021: February 2021Document24 pagesThe Saudi Economy in 2021: February 2021KidoltiNo ratings yet

- File 6530ce398b6c4 2024 2026 MTEF&FSP Transmittal Draft FinalDocument85 pagesFile 6530ce398b6c4 2024 2026 MTEF&FSP Transmittal Draft FinalMayowa DurosinmiNo ratings yet

- frb-6-acctg-for-jss-grantDocument12 pagesfrb-6-acctg-for-jss-grantcheezhen5047No ratings yet

- Economic Forecast ColombiaDocument3 pagesEconomic Forecast Colombiasuper_sumoNo ratings yet

- Economic Forecast Summary South Africa Oecd Economic OutlookDocument3 pagesEconomic Forecast Summary South Africa Oecd Economic OutlookVirali JadejaNo ratings yet

- Namibias-National-Budget-2023_24.pdf-webDocument12 pagesNamibias-National-Budget-2023_24.pdf-webAmogh KothariNo ratings yet

- 2021 Budget Highlights v1Document30 pages2021 Budget Highlights v1alexander amoakoNo ratings yet

- Questions RiskDocument6 pagesQuestions RiskShahid Ur RehmanNo ratings yet

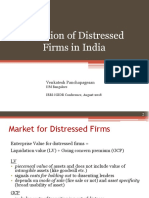

- Valuation of Distressed Firms in India: Venkatesh PanchapagesanDocument15 pagesValuation of Distressed Firms in India: Venkatesh PanchapagesanJobin JohnNo ratings yet

- State Governance Beyond The Shadow of Hierarchy': A Social Mechanisms Perspective On Governmental CSR PoliciesDocument23 pagesState Governance Beyond The Shadow of Hierarchy': A Social Mechanisms Perspective On Governmental CSR PoliciesJobin JohnNo ratings yet

- Questions RiskDocument6 pagesQuestions RiskShahid Ur RehmanNo ratings yet

- Valuation of A StartupDocument9 pagesValuation of A StartupJobin JohnNo ratings yet

- Business ValuationDocument9 pagesBusiness ValuationJobin JohnNo ratings yet

- The Impact of Tourism On Solid Waste Generation and Management Cost in Madeira Island For The Period 1996-2018Document16 pagesThe Impact of Tourism On Solid Waste Generation and Management Cost in Madeira Island For The Period 1996-2018Jobin JohnNo ratings yet

- HR Policy ExcelDocument40 pagesHR Policy ExcelJyotirmoy DasNo ratings yet

- Mba 2017 Core Course Strategic ManagemenDocument8 pagesMba 2017 Core Course Strategic ManagemenJobin JohnNo ratings yet

- Impact of HR Practices On Employee PerformanceDocument19 pagesImpact of HR Practices On Employee Performancelast islandNo ratings yet

- 05870f43cd4e6ba25fc970df48f8a449Document1 page05870f43cd4e6ba25fc970df48f8a449Jobin JohnNo ratings yet

- Chapter 9 Supermarket Checkout TrainingDocument27 pagesChapter 9 Supermarket Checkout TrainingJobin JohnNo ratings yet

- Chapter 6 Individual TurnoverDocument31 pagesChapter 6 Individual TurnoverJobin JohnNo ratings yet

- Vdocument - in History Optional Topic Wise Question Bank of Modern India Ias Modern IndianDocument48 pagesVdocument - in History Optional Topic Wise Question Bank of Modern India Ias Modern IndianJobin JohnNo ratings yet

- HR Employee Attrition 2Document128 pagesHR Employee Attrition 2Jobin JohnNo ratings yet

- CEO PayDocument1 pageCEO PayJobin JohnNo ratings yet

- The Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996Document22 pagesThe Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996srirama raoNo ratings yet

- Garch Vol ForecastDocument10 pagesGarch Vol ForecastJobin JohnNo ratings yet

- Economic and Financial Modelling With Eviews: November 2018Document2 pagesEconomic and Financial Modelling With Eviews: November 2018Jobin JohnNo ratings yet

- Sustainability 11 02263 v2Document19 pagesSustainability 11 02263 v2Abeer AbdullahNo ratings yet

- HR Policy ExcelDocument40 pagesHR Policy ExcelJyotirmoy DasNo ratings yet

- Sustainability 11 02263 v2Document19 pagesSustainability 11 02263 v2Abeer AbdullahNo ratings yet

- An Examination of Sustainable HRM Practices On Job Performance: An Application of Training As A ModeratorDocument19 pagesAn Examination of Sustainable HRM Practices On Job Performance: An Application of Training As A ModeratorJobin JohnNo ratings yet

- BV Cia 3Document27 pagesBV Cia 3Jobin JohnNo ratings yet

- The Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996Document22 pagesThe Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996srirama raoNo ratings yet

- HS 151 2021 - Cities Syllabus For CiruclaitonDocument3 pagesHS 151 2021 - Cities Syllabus For CiruclaitonAdvaith Krishna ANo ratings yet

- Ducast UAE Manhole Cover Product InformationDocument1 pageDucast UAE Manhole Cover Product InformationSohail YounisNo ratings yet

- Energypac 11kV Lightning Arrestor OfferDocument1 pageEnergypac 11kV Lightning Arrestor OfferRahul GhoshNo ratings yet

- 01 Pojmy Filmove Teorie 3Document10 pages01 Pojmy Filmove Teorie 3Maki DefaceNo ratings yet

- English - Kotak Bluechip Fund LeafletDocument2 pagesEnglish - Kotak Bluechip Fund LeafletAMAN SHARMANo ratings yet

- UJIAN AKHIR SEMESTER INVESTASI & PASAR MODALDocument17 pagesUJIAN AKHIR SEMESTER INVESTASI & PASAR MODALAthayaSekarNovianaNo ratings yet

- Chapter - 8 Foreign Exchange Forwards and Futures: Example 8.1Document40 pagesChapter - 8 Foreign Exchange Forwards and Futures: Example 8.1debojyotiNo ratings yet

- The Factors Influencing Bank Credit Risk: The Case of TunisiaDocument9 pagesThe Factors Influencing Bank Credit Risk: The Case of TunisiaAhanafNo ratings yet

- Forex Exchange and Risk Management 1Document18 pagesForex Exchange and Risk Management 1gel.silvestre23No ratings yet

- ECO162Document13 pagesECO162norfitrahmNo ratings yet

- Causes and Types of Poverty ExplainedDocument13 pagesCauses and Types of Poverty ExplainedShruti SinghNo ratings yet

- Binder 3Document279 pagesBinder 3jose bustilloNo ratings yet

- Growth of TourismDocument35 pagesGrowth of TourismEddie BrockNo ratings yet

- TAM The Effect of Perceived Usefulness and Perceived Ease of Use on Interest in Using Digital Payment ServicesDocument13 pagesTAM The Effect of Perceived Usefulness and Perceived Ease of Use on Interest in Using Digital Payment ServicesAcha LaideNo ratings yet

- 2827-Article Text-16261-1-10-20230323Document23 pages2827-Article Text-16261-1-10-20230323nurul aisahNo ratings yet

- MAHINDRA AND MAHINDRA FINANCIAL SERVICES LTD. Financial Results July 2021Document20 pagesMAHINDRA AND MAHINDRA FINANCIAL SERVICES LTD. Financial Results July 2021mukesh bhattNo ratings yet

- Measuring Exposure To Exchange Rate FluctuationsDocument36 pagesMeasuring Exposure To Exchange Rate FluctuationsTawhid Ahmed ChowdhuryNo ratings yet

- LEGOLAND Michigan Discovery CenterDocument3 pagesLEGOLAND Michigan Discovery CenterMark RussellNo ratings yet

- Design Sheet: Industry in The CountrysideDocument2 pagesDesign Sheet: Industry in The Countrysidelouis botheNo ratings yet

- ECO201 - SP23 - IB1702 - Group Assignment - Group 4Document15 pagesECO201 - SP23 - IB1702 - Group Assignment - Group 4JinyNo ratings yet

- Abp On RiceDocument65 pagesAbp On RiceImoter TyovendaNo ratings yet

- Goods & Services Tax Invoice Insurance Invoice (Labour)Document1 pageGoods & Services Tax Invoice Insurance Invoice (Labour)Deepak SharmaNo ratings yet

- Unemployment, Inflation and Impact of GDP in India: Xinhe XiaDocument7 pagesUnemployment, Inflation and Impact of GDP in India: Xinhe XiaSudam KarankeNo ratings yet

- Geography PDFDocument4 pagesGeography PDFworksatyajeetNo ratings yet

- Generic-Microeconomic EssentialsDocument126 pagesGeneric-Microeconomic EssentialsMualusi Mexzo Neluonde100% (1)

- Lesson 3 The Firm and Its EnvironmentDocument105 pagesLesson 3 The Firm and Its EnvironmentShunuan HuangNo ratings yet