You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

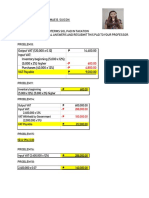

- Investment ExerciseDocument3 pagesInvestment ExerciseChristine Mae SuiconNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- (SEATWORK) PDFDocument1 page(SEATWORK) PDFChristine Mae SuiconNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Exercise Workbook For Student 36: SAP B1 On Cloud - AISDocument40 pagesExercise Workbook For Student 36: SAP B1 On Cloud - AISChristine Mae SuiconNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Auditing Securities Held by Third PartiesDocument3 pagesAuditing Securities Held by Third PartiesChristine Mae SuiconNo ratings yet

- Name: Suicon, Christine Mae Sbac 3BDocument2 pagesName: Suicon, Christine Mae Sbac 3BChristine Mae SuiconNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- AIS AnswersDocument3 pagesAIS AnswersChristine Mae SuiconNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Chapter-1 AisDocument9 pagesChapter-1 AisChristine Mae SuiconNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Opt-Assignment Suicon Sbac3bDocument12 pagesOpt-Assignment Suicon Sbac3bChristine Mae SuiconNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Sales (De Leon)Document737 pagesSales (De Leon)Bj Carido100% (7)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- IA-ACTIVITY1Document3 pagesIA-ACTIVITY1Christine Mae SuiconNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- (, October 02, 2009) : G.R. No. 155716Document15 pages(, October 02, 2009) : G.R. No. 155716Christine Mae SuiconNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Midterms Tax SuiconDocument5 pagesMidterms Tax SuiconChristine Mae SuiconNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Contract of Sale Review QuestionsDocument22 pagesContract of Sale Review QuestionsMaricris100% (7)

- TAXATION General PrinciplesDocument26 pagesTAXATION General PrinciplesMarie Mendoza100% (1)

- General Principles Part IIDocument21 pagesGeneral Principles Part IIMarie MendozaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Luljeta Pellumbi v. Atty Gen USA, 3rd Cir. (2012)Document8 pagesLuljeta Pellumbi v. Atty Gen USA, 3rd Cir. (2012)Scribd Government DocsNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Corruption and Indonesian CultureDocument2 pagesCorruption and Indonesian CultureBang RioNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Ouano Case DigestDocument1 pageOuano Case DigestCMLNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 8 Ysidoro V PeopleDocument2 pages8 Ysidoro V PeopleAlexandraSoledad100% (1)

- Religion and Politics in IndiaDocument10 pagesReligion and Politics in IndiassssNo ratings yet

- Oblicon 1106 - 1134Document14 pagesOblicon 1106 - 1134Hannah HazelNo ratings yet

- Supreme Student Government Parental ConsentDocument2 pagesSupreme Student Government Parental ConsentNinaNo ratings yet

- Non Corrigé UncorrectedDocument76 pagesNon Corrigé UncorrectedOmarNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- CASES2Document2 pagesCASES2Alma Aly Abedin RahimNo ratings yet

- Authorization Letters for Senior Citizens Financial AssistanceDocument4 pagesAuthorization Letters for Senior Citizens Financial AssistanceMichael MabiniNo ratings yet

- Day 4Document8 pagesDay 4Aw LapuzNo ratings yet

- Acc QuesDocument2 pagesAcc QuesComedy Ka BaapNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Manual, Aa - Mci Course ListDocument46 pagesManual, Aa - Mci Course ListEric ChristophersonNo ratings yet

- Judaism Discovered Michael HoffmanDocument8 pagesJudaism Discovered Michael HoffmanCarlos D100% (1)

- History of Land Tenure in EnglandDocument3 pagesHistory of Land Tenure in EnglandissaNo ratings yet

- Surah Anam Ayat 124 ExplainedDocument5 pagesSurah Anam Ayat 124 ExplainedMohd Idris MohiuddinNo ratings yet

- Demand Letter (Discussion)Document3 pagesDemand Letter (Discussion)Irish AnnNo ratings yet

- Copyright Infringement Case Over Vietnamese Music VideosDocument99 pagesCopyright Infringement Case Over Vietnamese Music VideosRai NguyễnNo ratings yet

- Marc PlattDocument13 pagesMarc Plattapi-566381187No ratings yet

- Office & Branches: Head Office PT Indosat Mega Media (IM2)Document4 pagesOffice & Branches: Head Office PT Indosat Mega Media (IM2)satriamesumNo ratings yet

- PTI Overseas IPE - Final Panels For Intra-Party Election 2018Document1 pagePTI Overseas IPE - Final Panels For Intra-Party Election 2018Insaf.PKNo ratings yet

- Muhammad Shaban - Islamic History - A.D. 600 To 750, New Interpretation Volume I (1971)Document203 pagesMuhammad Shaban - Islamic History - A.D. 600 To 750, New Interpretation Volume I (1971)Kaibamir SetoNo ratings yet

- Process Labor BirthDocument4 pagesProcess Labor Birthapi-318891098No ratings yet

- Actividad Integradora 2 Modulo 7Document2 pagesActividad Integradora 2 Modulo 7ghostcity180405No ratings yet

- Policy Evaluation (Anti-Hazing Law)Document3 pagesPolicy Evaluation (Anti-Hazing Law)Patrick LasalaNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Moot Case - Aurangabad ActivityDocument2 pagesMoot Case - Aurangabad ActivityBodhisatya DeyNo ratings yet

- Quantum Meruit Claims Explained in ContractsDocument13 pagesQuantum Meruit Claims Explained in ContractsPhillip KitulaNo ratings yet

- Supreme Court Rules on Jurisdiction Over Administrative Cases Against State University PresidentDocument2 pagesSupreme Court Rules on Jurisdiction Over Administrative Cases Against State University PresidentJanet FabiNo ratings yet

- BullyingDocument49 pagesBullyingClarisse Alcazar-PeridoNo ratings yet

- What Is Interpleader Suit - IpleadersDocument20 pagesWhat Is Interpleader Suit - IpleadersEnoch RNo ratings yet