You might also like

- Chapter 5 COST ACCTG AND CNTRLDocument14 pagesChapter 5 COST ACCTG AND CNTRLRomano Cruz100% (6)

- SRS 201 209 210 217Document9 pagesSRS 201 209 210 217kkrish910050% (2)

- MS 5.0 (3) Assessment Paper 1Document10 pagesMS 5.0 (3) Assessment Paper 1Omer KhazalNo ratings yet

- General Electric CaseDocument8 pagesGeneral Electric CaseTruong Le quang0% (1)

- Bus 5110 Unit 2 AssignmentDocument5 pagesBus 5110 Unit 2 Assignmentwonnetta nicholson0% (1)

- Oracle Inventory Management - Performing Cycle Counting Using ABC Assignment Groups and Item CategoriesDocument33 pagesOracle Inventory Management - Performing Cycle Counting Using ABC Assignment Groups and Item CategoriesSantOsh100% (1)

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Presentation 04 (1slide-Pg)Document33 pagesPresentation 04 (1slide-Pg)araika.maksutNo ratings yet

- Datar 17e Accessible Fullppt 02Document35 pagesDatar 17e Accessible Fullppt 02shubitidzesaba09No ratings yet

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- 3 Classification of Cost CMA Inter Costing Fast Track ClassDocument18 pages3 Classification of Cost CMA Inter Costing Fast Track ClassLeviNo ratings yet

- ACCT 2102: Principles of Management AccountingDocument61 pagesACCT 2102: Principles of Management AccountingSihua ChengNo ratings yet

- L1-Manufacturer's CostDocument19 pagesL1-Manufacturer's CostomarNo ratings yet

- Accouting Lecture7Document61 pagesAccouting Lecture7Jingxuan LuoNo ratings yet

- Chapter 2Document30 pagesChapter 2Manuel TadicNo ratings yet

- 2 - Cost Concepts and BehaviorsDocument4 pages2 - Cost Concepts and BehaviorsKaryl FailmaNo ratings yet

- Chapter 2Document5 pagesChapter 2Hania M. CalandadaNo ratings yet

- PGP-CMA-Cost Fundamentals PDFDocument53 pagesPGP-CMA-Cost Fundamentals PDFRiturajPaulNo ratings yet

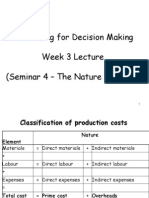

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- ABC Analysis HandoutsDocument11 pagesABC Analysis HandoutsTushar DuaNo ratings yet

- A Typical Costing System Accounts For Cost by Doing Two Main TasksDocument19 pagesA Typical Costing System Accounts For Cost by Doing Two Main TasksvdhienNo ratings yet

- MI Chapter 2Document19 pagesMI Chapter 2patrickdaniel2322No ratings yet

- Lecture 2 Cost Terms, Concepts and ClassificationDocument34 pagesLecture 2 Cost Terms, Concepts and ClassificationTgrh TgrhNo ratings yet

- Chapter 2 - Apply A Range of Management Accounting TechniquesDocument34 pagesChapter 2 - Apply A Range of Management Accounting TechniquesHING SIEW LIANNo ratings yet

- Chapter 02 - Cost Term and Concepts FinalDocument60 pagesChapter 02 - Cost Term and Concepts FinalAminaMatinNo ratings yet

- Unit 2Document8 pagesUnit 2Shikara DumayagNo ratings yet

- CH 4Document16 pagesCH 4Euis Muliawaty NNo ratings yet

- Chapter 2 + 3 3Document76 pagesChapter 2 + 3 3tfyrkys9gvNo ratings yet

- Cost Management Systems and Activity-Based Costing: Learning ObjectivesDocument15 pagesCost Management Systems and Activity-Based Costing: Learning ObjectivesIsaac Samy IsaacNo ratings yet

- Cost AccountingDocument2 pagesCost AccountingKNo ratings yet

- ACCT 403 Cost Accounting: Absorption and Variable Costing TechniquesDocument26 pagesACCT 403 Cost Accounting: Absorption and Variable Costing TechniquesOFORINo ratings yet

- Chapter 2Document25 pagesChapter 2JOSEPH LEE ZE LOONG MoeNo ratings yet

- Factory Overhead Costing and ControlDocument20 pagesFactory Overhead Costing and ControlAyesha JavedNo ratings yet

- Week 6 Lecture SlidesDocument51 pagesWeek 6 Lecture Slidessaba bastiNo ratings yet

- Summary Chapter 4Document3 pagesSummary Chapter 4ninarizkitaNo ratings yet

- Activity-Based Costing: Chapter ReviewDocument29 pagesActivity-Based Costing: Chapter ReviewRommel RoyceNo ratings yet

- Cost Terms and ConceptsDocument13 pagesCost Terms and ConceptsPASCUA RENALYN M.No ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsAmer Wagdy GergesNo ratings yet

- Activity Based Costing: DR Meena BhatiaDocument23 pagesActivity Based Costing: DR Meena BhatiaAkashbaldwinNo ratings yet

- Topic 2 IDocument16 pagesTopic 2 Iami zawaniNo ratings yet

- Supplementary 1 - Cost ClassificationDocument26 pagesSupplementary 1 - Cost ClassificationNguyen Tuan Anh (BTEC HN)No ratings yet

- 2, Cost Terms and PurposesDocument24 pages2, Cost Terms and PurposesclairecstrattonNo ratings yet

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Cost ConceptDocument25 pagesCost ConceptMadli SiregarNo ratings yet

- Activity Based Costing - UNAMDocument32 pagesActivity Based Costing - UNAMWilhelmina KandjekeNo ratings yet

- ME403 (Sem1) Lecture 7. Cost EstimationDocument42 pagesME403 (Sem1) Lecture 7. Cost EstimationJoxe EsnaolaNo ratings yet

- Including: Chapter 8 (Appendix)Document48 pagesIncluding: Chapter 8 (Appendix)Tiến DũngNo ratings yet

- Chapter - 2 - Managerial Accounting and Cost ConceptDocument61 pagesChapter - 2 - Managerial Accounting and Cost ConceptSoka PokaNo ratings yet

- Classification of CostDocument23 pagesClassification of CostShohidul Islam SaykatNo ratings yet

- Cost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan HakroDocument35 pagesCost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan Hakrokashif aliNo ratings yet

- Managerial Accounting and Cost ConceptsDocument6 pagesManagerial Accounting and Cost ConceptsJUST KINGNo ratings yet

- Chapter 4 OverheadDocument21 pagesChapter 4 OverheadMUHAMMAD ZAIM HAMZI MUHAMMAD ZINNo ratings yet

- PD DocumentsDocument6 pagesPD DocumentsMicheal LyobaNo ratings yet

- Cost Classification or Cost Flow in An OrgaizationDocument8 pagesCost Classification or Cost Flow in An OrgaizationvaloruroNo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- Cost Classifications: Learning ObjectivesDocument32 pagesCost Classifications: Learning ObjectivesKhánh Đoan NgôNo ratings yet

- PDFenDocument68 pagesPDFenby ScribdNo ratings yet

- Managerial Accounting Module 2Document14 pagesManagerial Accounting Module 2Charlyn LapeñaNo ratings yet

- P1 1d.0a14eb8 NotesDocument140 pagesP1 1d.0a14eb8 Notesyahoo2008No ratings yet

- CHAPTER 2 Cost Classification-2Document9 pagesCHAPTER 2 Cost Classification-2sarahayeesha1No ratings yet

- Cost ClassificationDocument19 pagesCost ClassificationAli AshhabNo ratings yet

- Bab 2 - Perilaku BiayaDocument40 pagesBab 2 - Perilaku BiayaAndy ReynaldyyNo ratings yet

- Bab 2 - Perilaku BiayaDocument40 pagesBab 2 - Perilaku BiayaAndy ReynaldyyNo ratings yet

- Presenting Information: Acca - Applied KnowledgeDocument9 pagesPresenting Information: Acca - Applied KnowledgeTrà My ĐoànNo ratings yet

- Accounting For Materials: Acca - Applied KnowledgeDocument15 pagesAccounting For Materials: Acca - Applied KnowledgeTrà My ĐoànNo ratings yet

- Accounting For Management: Acca - Applied KnowledgeDocument9 pagesAccounting For Management: Acca - Applied KnowledgeTrà My ĐoànNo ratings yet

- Sources of Data: Acca - Applied KnowledgeDocument8 pagesSources of Data: Acca - Applied KnowledgeTrà My ĐoànNo ratings yet

- Chapter 5 - Tayler Et Al (2020)Document44 pagesChapter 5 - Tayler Et Al (2020)Mai TuấnNo ratings yet

- Hyperion Lite PaperDocument13 pagesHyperion Lite PaperajdCruiseNo ratings yet

- Consumer Beahviour and Perception of Women Towards LakmeDocument72 pagesConsumer Beahviour and Perception of Women Towards LakmeDeepak ParidaNo ratings yet

- Ga Capsule Sbi Po Mains 2021 by Ambitious BabaDocument221 pagesGa Capsule Sbi Po Mains 2021 by Ambitious BabaLalesh Sharma100% (1)

- Wto Dispute Settlement Understanding: An OverviewDocument8 pagesWto Dispute Settlement Understanding: An OverviewAkshat GuptaNo ratings yet

- Deepak Kumar: SkillsDocument4 pagesDeepak Kumar: SkillsdeepakNo ratings yet

- BPC Training CatalogueTemplate V2.2Document28 pagesBPC Training CatalogueTemplate V2.2trongnvtNo ratings yet

- Qdoc - Tips Venkat Apdss ReadDocument181 pagesQdoc - Tips Venkat Apdss Readzoya siddiqhiNo ratings yet

- RBH Engineering and Contractor Servicesrevised2020Document18 pagesRBH Engineering and Contractor Servicesrevised2020May Ann DuronNo ratings yet

- Safe Systems of Work: Health and Safety Guidance NoteDocument5 pagesSafe Systems of Work: Health and Safety Guidance NotewawaasderNo ratings yet

- Roles of Advertising in Manufacturing Organizations (A Case Study of Nigeria Bottling Company)Document57 pagesRoles of Advertising in Manufacturing Organizations (A Case Study of Nigeria Bottling Company)Charles RomeoNo ratings yet

- Nissan Automobile: Case Study AssignmentDocument39 pagesNissan Automobile: Case Study Assignmentpulith udaveenNo ratings yet

- Marketing Management Chapter 11Document23 pagesMarketing Management Chapter 11Soumya Jyoti BhattacharyaNo ratings yet

- SOCIETAL CONCERN AND NGO Operation PDFDocument31 pagesSOCIETAL CONCERN AND NGO Operation PDFSANTOSH JHANo ratings yet

- Union Budget 2021 - 22: Anuj JindalDocument20 pagesUnion Budget 2021 - 22: Anuj JindalamritNo ratings yet

- Sbi Po Ratio - English - 1578405778Document10 pagesSbi Po Ratio - English - 1578405778వన మాలిNo ratings yet

- Worksheet 5Document14 pagesWorksheet 5HiraiNo ratings yet

- For Goats CertificateDocument6 pagesFor Goats CertificateBeximco Denim LabNo ratings yet

- Electronics vs. Non-Electronic Voucher Card Systems in Ethio-Telecom: Implication To Service Accessibility and Customer SatisfactionDocument110 pagesElectronics vs. Non-Electronic Voucher Card Systems in Ethio-Telecom: Implication To Service Accessibility and Customer SatisfactionBK ICTNo ratings yet

- Accounting Fraud: A Study On Sonali Bank Limited (Hallmark) ScamDocument42 pagesAccounting Fraud: A Study On Sonali Bank Limited (Hallmark) Scammunatasneem94% (17)

- Corporate Finance (FINA0050) 2018 - Exercises Session 3 SolutionsDocument7 pagesCorporate Finance (FINA0050) 2018 - Exercises Session 3 SolutionsLouisRemNo ratings yet

- Problems: SolutionDocument4 pagesProblems: SolutionHdjsns khooNo ratings yet

- Inventory Basics StimulationDocument2 pagesInventory Basics Stimulationswarnima biswariNo ratings yet

- Mcm301 Final Term Imp MCQDocument32 pagesMcm301 Final Term Imp MCQUnity of GamersNo ratings yet

- Contracts Memo New 1Document15 pagesContracts Memo New 1mahuaNo ratings yet

- Air Waybill Sky Lease Cargo: Frymaster C.ODocument1 pageAir Waybill Sky Lease Cargo: Frymaster C.OAlexa ContrerasNo ratings yet