You might also like

- Chapter 15Document8 pagesChapter 15Mychie Lynne MayugaNo ratings yet

- Intermediate Accounting 3 - SolutionsDocument3 pagesIntermediate Accounting 3 - Solutionssammie helsonNo ratings yet

- Calvo, Jhoanne C.-BSA 2-1-Chapter 4-Problem 11-20Document12 pagesCalvo, Jhoanne C.-BSA 2-1-Chapter 4-Problem 11-20Jhoanne CalvoNo ratings yet

- Chapter 14 (Ia3)Document13 pagesChapter 14 (Ia3)richmond naragNo ratings yet

- P6Document3 pagesP6Jessica HutabaratNo ratings yet

- Best Friends Co. Statement of Profit or Loss and Other Comprehensive Income For The Year Ended December 31, 20x1Document3 pagesBest Friends Co. Statement of Profit or Loss and Other Comprehensive Income For The Year Ended December 31, 20x1Luis AlcalaNo ratings yet

- ACCT103 Supplementary Notes Cash and Cash EquivalentsDocument1 pageACCT103 Supplementary Notes Cash and Cash EquivalentsChrislyn Janna BeljeraNo ratings yet

- Batch 18 1st Preboard (P1)Document14 pagesBatch 18 1st Preboard (P1)Jericho PedragosaNo ratings yet

- FAR Problem Quiz 1 SolDocument3 pagesFAR Problem Quiz 1 SolEdnalyn CruzNo ratings yet

- Chow2019 SIM AC2091 MockExamA StudentDocument23 pagesChow2019 SIM AC2091 MockExamA StudentPadamchand PokharnaNo ratings yet

- Ujian 1 AdvDocument33 pagesUjian 1 AdvaraNo ratings yet

- P4-10 and P4-16 Cash Flow and Financial Statement AnalysisDocument12 pagesP4-10 and P4-16 Cash Flow and Financial Statement AnalysisElif TuncaNo ratings yet

- Sample Problems Cash Flow AnalysisDocument2 pagesSample Problems Cash Flow AnalysisTeresa AlbertoNo ratings yet

- Finman 108 (Quiz 4) ...Document6 pagesFinman 108 (Quiz 4) ...CHARRYSAH TABAOSARESNo ratings yet

- 105 - Activity 1 - Cash FlowDocument11 pages105 - Activity 1 - Cash FlowElla DavisNo ratings yet

- Accounts Receivable, Accounts Payable, Sales and Purchases ProblemsDocument30 pagesAccounts Receivable, Accounts Payable, Sales and Purchases ProblemsJem ValmonteNo ratings yet

- Problem 14 - 1Document6 pagesProblem 14 - 1Rouise GagalacNo ratings yet

- Answers To Installment Accounting Previously Uploaded in This ProfileDocument6 pagesAnswers To Installment Accounting Previously Uploaded in This ProfileKate AlvarezNo ratings yet

- The Fine Manufacturing Company Overhead Cost AnalysisDocument4 pagesThe Fine Manufacturing Company Overhead Cost AnalysisexquisiteNo ratings yet

- Revenue and Expense Budgets with Cash Flow AnalysisDocument4 pagesRevenue and Expense Budgets with Cash Flow AnalysisAdrià BurgellNo ratings yet

- Sandy Company Statement of Cash Flows Year Ended 2019Document2 pagesSandy Company Statement of Cash Flows Year Ended 2019Rouise Gagalac100% (1)

- Singapore Institute of Management UOL International Programme AC2091 Financial Reporting Session 6: Associates Practice QuestionsDocument6 pagesSingapore Institute of Management UOL International Programme AC2091 Financial Reporting Session 6: Associates Practice Questionsduong duongNo ratings yet

- Tayaban Lancer Company 1Document4 pagesTayaban Lancer Company 1Tayaban Van GihNo ratings yet

- ACCTG 205A Midterm exam problemsDocument1 pageACCTG 205A Midterm exam problemsYameteKudasaiNo ratings yet

- Balucan InAcc 3 Week2 Part 2Document2 pagesBalucan InAcc 3 Week2 Part 2Luigi Enderez BalucanNo ratings yet

- Answer TranslationDocument1 pageAnswer TranslationJULLIE CARMELLE H. CHATTONo ratings yet

- May 2018 Crammer's Guide Answers: Inventory To Be Removed From Inventory Because of Purchase Cutoff TestDocument14 pagesMay 2018 Crammer's Guide Answers: Inventory To Be Removed From Inventory Because of Purchase Cutoff TestJamieNo ratings yet

- Soal Kuis 2Document6 pagesSoal Kuis 2Rahajeng SantosoNo ratings yet

- Sales, Costs, Inventory TrackingDocument34 pagesSales, Costs, Inventory TrackingGenie MaeNo ratings yet

- ACCCOB1 Module 3Document19 pagesACCCOB1 Module 3Ayanna CameroNo ratings yet

- FR 2018 Paper PrelimDocument12 pagesFR 2018 Paper PrelimshashalalaxiangNo ratings yet

- Mahusay, Bsa 315 - Module 2-CaseletsDocument10 pagesMahusay, Bsa 315 - Module 2-CaseletsJeth MahusayNo ratings yet

- Ia MidtermDocument5 pagesIa MidtermCindy CrausNo ratings yet

- Statement of Profit and LossDocument1 pageStatement of Profit and Lossmatthew amadeusNo ratings yet

- Case 8 2 Palmerstown Company - CompressDocument4 pagesCase 8 2 Palmerstown Company - CompressPhương Nguyễn HàNo ratings yet

- BTNS Services Income Statement for Year Ending Dec 31, 201ADocument2 pagesBTNS Services Income Statement for Year Ending Dec 31, 201AIvan CutiamNo ratings yet

- Lotus Income StatementDocument6 pagesLotus Income StatementJoseph AsisNo ratings yet

- 03 Activity 1Document1 page03 Activity 1bea santiagoNo ratings yet

- Accounts Receivable and AFBDDocument18 pagesAccounts Receivable and AFBDeia aieNo ratings yet

- Total Cash Available (1 + 2) 82,500 124,000 89,275Document6 pagesTotal Cash Available (1 + 2) 82,500 124,000 89,275Nischal LawojuNo ratings yet

- FDNACCT - Mock Exam - Answer Key - 3 - Fill in The Blank Problems PDFDocument5 pagesFDNACCT - Mock Exam - Answer Key - 3 - Fill in The Blank Problems PDFJames de LeonNo ratings yet

- Seatwork Ratio AnalysisDocument2 pagesSeatwork Ratio AnalysisMARIBEL SANTOSNo ratings yet

- Consolidated Net Income P 370,000 P 460,000: Illustrative ProblemsDocument11 pagesConsolidated Net Income P 370,000 P 460,000: Illustrative ProblemsKeir GaspanNo ratings yet

- Income Statement and OCI - Exercises - AnswerDocument3 pagesIncome Statement and OCI - Exercises - AnswerYstefani ValderamaNo ratings yet

- Book 1Document7 pagesBook 1IQVIANo ratings yet

- Quiz in Module 8 Key AnswerDocument6 pagesQuiz in Module 8 Key AnswerfabyunaaaNo ratings yet

- CMPC 131 SolutionsDocument3 pagesCMPC 131 SolutionsNhel AlvaroNo ratings yet

- Elaine WorkDocument8 pagesElaine WorkElaine CasamaNo ratings yet

- Prctice SetDocument9 pagesPrctice SetAdam CuencaNo ratings yet

- Start-Up Capital:: Particulars Taka TakaDocument5 pagesStart-Up Capital:: Particulars Taka TakaSahriar EmonNo ratings yet

- Chapter 9 - Presentation of Fs (Statement of Comprehensive Income)Document2 pagesChapter 9 - Presentation of Fs (Statement of Comprehensive Income)Mark IlanoNo ratings yet

- Equity Method (First Year of Acquisition)Document3 pagesEquity Method (First Year of Acquisition)Angel Chane OstrazNo ratings yet

- Generate Statement of Cash FlowsDocument2 pagesGenerate Statement of Cash FlowsAlyssa AlejandroNo ratings yet

- Profit and Loss Account For The Year Ended 31.03.2016 Particulars Amount Particulars Amount (Rs '000's) (Rs '000's)Document3 pagesProfit and Loss Account For The Year Ended 31.03.2016 Particulars Amount Particulars Amount (Rs '000's) (Rs '000's)Sushant SaxenaNo ratings yet

- Comparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018Document5 pagesComparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018JonellNo ratings yet

- MadindigwaDocument7 pagesMadindigwaRay MondNo ratings yet

- Business Com ActivityDocument2 pagesBusiness Com ActivityAlyssa AnnNo ratings yet

- 8, Problems #7-11Document7 pages8, Problems #7-11jowdpugsNo ratings yet

- Financial Statement - Without AdjustmentDocument29 pagesFinancial Statement - Without AdjustmentAnmol SinghNo ratings yet

- BSDocument2 pagesBSMaria Fe Joanna AbonitaNo ratings yet

- BSDocument2 pagesBSMaria Fe Joanna AbonitaNo ratings yet

- BSDocument2 pagesBSMaria Fe Joanna AbonitaNo ratings yet

- BSDocument2 pagesBSMaria Fe Joanna AbonitaNo ratings yet

- ProblemDocument3 pagesProblemMaria Fe Joanna AbonitaNo ratings yet

- Selling Price 780Document2 pagesSelling Price 780Maria Fe Joanna AbonitaNo ratings yet

- I I ManpowerDocument5 pagesI I ManpowerMaria Fe Joanna AbonitaNo ratings yet

- Philips Electronics CorporationDocument2 pagesPhilips Electronics CorporationMaria Fe Joanna AbonitaNo ratings yet

- I I ManpowerDocument5 pagesI I ManpowerMaria Fe Joanna AbonitaNo ratings yet

- Selling Price 780Document2 pagesSelling Price 780Maria Fe Joanna AbonitaNo ratings yet

- Nedai, Abbas (562-388-900) and Hosseini Ssayadnavard, MaryamDocument122 pagesNedai, Abbas (562-388-900) and Hosseini Ssayadnavard, Maryamirajiraj77No ratings yet

- May 2022 PayslipDocument1 pageMay 2022 PayslipJustice Agbeko100% (1)

- Tutorial 4 - QuestionsDocument2 pagesTutorial 4 - QuestionsHuang ZhanyiNo ratings yet

- Taxation Powers and Principles ExplainedDocument19 pagesTaxation Powers and Principles ExplainedRia GayleNo ratings yet

- Sunil Sangwan Report On Capital BudgetDocument28 pagesSunil Sangwan Report On Capital BudgetRahul ShishodiaNo ratings yet

- Account Statement From 12 Jan 2023 To 12 Jul 2023Document10 pagesAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyNo ratings yet

- X Macey Slonaker Crystal L Slonaker 292-84-7018: U.S. Individual Income Tax ReturnDocument12 pagesX Macey Slonaker Crystal L Slonaker 292-84-7018: U.S. Individual Income Tax ReturnjonathanNo ratings yet

- Corp Account - Liquidators StatementDocument3 pagesCorp Account - Liquidators StatementAnanth RohithNo ratings yet

- FS to RECEIVABLE - Petty Cash, Accounts Receivable, Shareholders' EquityDocument31 pagesFS to RECEIVABLE - Petty Cash, Accounts Receivable, Shareholders' EquityWillen Christia M. MadulidNo ratings yet

- No Dues CertificateDocument2 pagesNo Dues CertificateSatyajit BanerjeeNo ratings yet

- Banking Regulations: Reasons For The Regulation of BanksDocument6 pagesBanking Regulations: Reasons For The Regulation of BanksMarwa HassanNo ratings yet

- A Project Report On: "Research On Capital Market With Indiainfoline LTDDocument94 pagesA Project Report On: "Research On Capital Market With Indiainfoline LTDgauravNo ratings yet

- Valuing Companies by Cash Flow Discounting Ten Methods and Nine TheoriesDocument16 pagesValuing Companies by Cash Flow Discounting Ten Methods and Nine TheoriesparthkosadaNo ratings yet

- Understanding Keynesian Cross Model and Fiscal Policy MultipliersDocument30 pagesUnderstanding Keynesian Cross Model and Fiscal Policy MultiplierswaysNo ratings yet

- Power Sector OutlookDocument5 pagesPower Sector OutlookJade EspirituNo ratings yet

- Submitted To: Ms Sukhwinder Kaur Submitted By: Megha Tah (T1901B46)Document34 pagesSubmitted To: Ms Sukhwinder Kaur Submitted By: Megha Tah (T1901B46)vijaybaliyanNo ratings yet

- The Micro Credit Sector in South Africa - An Overview of The History, Financial Access, Challenges and Key PlayersDocument9 pagesThe Micro Credit Sector in South Africa - An Overview of The History, Financial Access, Challenges and Key PlayerstodzaikNo ratings yet

- Ivey MSc Classes Employment Report 2014-2015Document7 pagesIvey MSc Classes Employment Report 2014-2015Ryan 黄俊杰 WongNo ratings yet

- Charged ExpenditureDocument7 pagesCharged ExpendituremanojhunkNo ratings yet

- Sara Dhuri: CertificateDocument7 pagesSara Dhuri: CertificateHALOLLOLNo ratings yet

- Presentation 4: Credit Rating To Customers in Commercial Banks: Rationality and IssuesDocument10 pagesPresentation 4: Credit Rating To Customers in Commercial Banks: Rationality and IssuesNguyễn Thế LongNo ratings yet

- Black BookDocument41 pagesBlack BookMoazza QureshiNo ratings yet

- Bellone 11 Day Pre GeneralDocument17 pagesBellone 11 Day Pre GeneralRiverheadLOCALNo ratings yet

- Tax Invoice: M/S. Panakala & Co., Chartered Accountants Prop.: C.A K Panakala Rao Indian Bank-Bill ToDocument1 pageTax Invoice: M/S. Panakala & Co., Chartered Accountants Prop.: C.A K Panakala Rao Indian Bank-Bill Tomanoj mohanNo ratings yet

- Simon Property Group - Quick ReportDocument1 pageSimon Property Group - Quick Reporttkang79No ratings yet

- Wisma Perkasa SDN BHD V Weatherford (M) SDN BHD & AnorDocument38 pagesWisma Perkasa SDN BHD V Weatherford (M) SDN BHD & AnorSellamal ServaiNo ratings yet

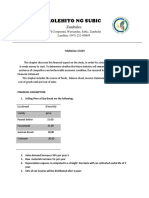

- Kolehiyo NG Subic: ZambalesDocument3 pagesKolehiyo NG Subic: ZambalesRodeliza DuncanNo ratings yet

- Acronyms Important Abbreviations in Banking: AffairsDocument10 pagesAcronyms Important Abbreviations in Banking: AffairsAbhijeet PatilNo ratings yet

- DuPont analysis assignmentDocument5 pagesDuPont analysis assignmentআশিকুর রহমান100% (1)

- BCom 3rd and 4th Sem SyllabusDocument26 pagesBCom 3rd and 4th Sem Syllabusshurikenjutsu123No ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)