You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Part Ii March 2021 InsightDocument140 pagesPart Ii March 2021 Insightrowan betNo ratings yet

- 11 Accountancy SP 1Document12 pages11 Accountancy SP 1Ujjwal Agrawal100% (1)

- ATS march-2020-insight-part-IIDocument104 pagesATS march-2020-insight-part-IIAromasodun Omobolanle IswatNo ratings yet

- ABM1 FinalsDocument3 pagesABM1 Finalsje-ann montejoNo ratings yet

- Acctg 12 Premid Exam QuestionnaireDocument11 pagesAcctg 12 Premid Exam QuestionnaireJanet AnotdeNo ratings yet

- CAT L1 Assessment Exam (Batch May 2022) - 1Document9 pagesCAT L1 Assessment Exam (Batch May 2022) - 1Sofia Mae AlbercaNo ratings yet

- AccountsDocument100 pagesAccountskaran kNo ratings yet

- 11 Accountancy SP 1Document13 pages11 Accountancy SP 1Ansh YadavNo ratings yet

- Bcom I Fa 103 MCQSDocument11 pagesBcom I Fa 103 MCQSTushar GuptaNo ratings yet

- Quiz 1 Sample 4 SolvedDocument4 pagesQuiz 1 Sample 4 SolvedFami FamzNo ratings yet

- Model Exam of Accounting DegreeDocument27 pagesModel Exam of Accounting DegreeJizy JizyNo ratings yet

- Salale UniversityDocument10 pagesSalale UniversityRegasa GutemaNo ratings yet

- Book Keeping Mdr1Document5 pagesBook Keeping Mdr1Nassrah JumaNo ratings yet

- 2020 BHSEC Accountancy (New Curriculum) MA FinalDocument22 pages2020 BHSEC Accountancy (New Curriculum) MA FinalSoNam ZaNgmoNo ratings yet

- FIN ACCOUNT YEAR 12 MID TERM TEST ConfirmDocument8 pagesFIN ACCOUNT YEAR 12 MID TERM TEST ConfirmJanet HarryNo ratings yet

- Preodic Class TestDocument5 pagesPreodic Class TestMOHAMMAD SYED AEJAZNo ratings yet

- Accounting Technicians Scheme Paper for March 2021 Diet Questions and Marking SchemeDocument34 pagesAccounting Technicians Scheme Paper for March 2021 Diet Questions and Marking SchemeAdjin LomoteyNo ratings yet

- PAR COR ACCOUNTING CUP_AVERAGE QUESTIONS SOLVEDDocument6 pagesPAR COR ACCOUNTING CUP_AVERAGE QUESTIONS SOLVEDShin YaeNo ratings yet

- Principles of Accounting Objective and Essay Type QuestionsDocument5 pagesPrinciples of Accounting Objective and Essay Type QuestionsMaryam TanveerNo ratings yet

- 2022 Sem 1 ACC10007 Practice MCQs - Topic 4Document6 pages2022 Sem 1 ACC10007 Practice MCQs - Topic 4JordanNo ratings yet

- Novemebr 2017 Pathfinder FoundationDocument143 pagesNovemebr 2017 Pathfinder FoundationOgahNo ratings yet

- Final Exam Review: Fundamentals of Accounting Part 2Document12 pagesFinal Exam Review: Fundamentals of Accounting Part 2잔잔No ratings yet

- Accounting: Sāmoa School Certificate ExaminationDocument28 pagesAccounting: Sāmoa School Certificate ExaminationmonyNo ratings yet

- Sample Paper Accountancy-IIDocument7 pagesSample Paper Accountancy-IIpranav21519No ratings yet

- Worksheet-Adavnce-Distance EducationDocument5 pagesWorksheet-Adavnce-Distance EducationtamirubeletenNo ratings yet

- Accounting PaperDocument4 pagesAccounting PaperMaryam TanveerNo ratings yet

- ABM 2 Exam 2 v1 2023 StudentDocument10 pagesABM 2 Exam 2 v1 2023 StudentdwacindyfjNo ratings yet

- Prefinal Review AcfarDocument8 pagesPrefinal Review AcfarBugoy CabasanNo ratings yet

- Practice Paper of XI-Term-1 (2021-22)Document15 pagesPractice Paper of XI-Term-1 (2021-22)Allwin GanaduraiNo ratings yet

- QUIEZON NATIONAL HIGH SCHOOL 1ST QUARTER EXAM REVIEWDocument7 pagesQUIEZON NATIONAL HIGH SCHOOL 1ST QUARTER EXAM REVIEWMAYCAROL TUMALIUANNo ratings yet

- Accounting Information Systems Final ExamDocument16 pagesAccounting Information Systems Final Examrikansha100% (1)

- Mycbseguide: Class 12 - Accountancy Sample Paper 07Document15 pagesMycbseguide: Class 12 - Accountancy Sample Paper 07sneha muralidharanNo ratings yet

- Answer Key Is Available Only On Grewal Conceptual Learning App' (Available On Playstore and Appstore)Document19 pagesAnswer Key Is Available Only On Grewal Conceptual Learning App' (Available On Playstore and Appstore)Madhumithaa SvNo ratings yet

- Business, Accounting and Financial Studies Mock Examination Paper 1Document24 pagesBusiness, Accounting and Financial Studies Mock Examination Paper 1CM LeungNo ratings yet

- Passing Package AccDocument93 pagesPassing Package AccOM VNo ratings yet

- IGCSE Accounting Complete Exam Paper3Document9 pagesIGCSE Accounting Complete Exam Paper3Jayaprakash MehtaNo ratings yet

- Amoni Edome Coc Sample Exam-Level LLLDocument13 pagesAmoni Edome Coc Sample Exam-Level LLLAmoni EdomeNo ratings yet

- Model ExamDocument25 pagesModel ExambinaNo ratings yet

- Model Exam 1Document25 pagesModel Exam 1rahelsewunet0r37203510No ratings yet

- 9706 w04 QP 1Document12 pages9706 w04 QP 1gibbamanjexNo ratings yet

- Master Minds CA CPT Question Paper Memory BasedDocument28 pagesMaster Minds CA CPT Question Paper Memory BasedRakesh BhatiNo ratings yet

- 22-23 X2 S4 BAFS P2A MC ExplanationsDocument6 pages22-23 X2 S4 BAFS P2A MC Explanationss191056No ratings yet

- March 2019 Part Ii InsightDocument120 pagesMarch 2019 Part Ii InsightIslamiat PopoolaNo ratings yet

- HKUGA CollegeDocument8 pagesHKUGA Colleges191056No ratings yet

- Question For Manager Test in Ksfe PDFDocument11 pagesQuestion For Manager Test in Ksfe PDFRajimol RNo ratings yet

- Auditing.: A. B. C. DDocument12 pagesAuditing.: A. B. C. DbiniamNo ratings yet

- SEO-Optimized Multiple Choice Exam QuestionsDocument3 pagesSEO-Optimized Multiple Choice Exam QuestionsChristian Joy ReyesNo ratings yet

- 5 Question - FinanceDocument19 pages5 Question - FinanceMuhammad IrfanNo ratings yet

- Module 7 QuestionDocument21 pagesModule 7 QuestionWarren MakNo ratings yet

- Updated 2002 - 2009Document172 pagesUpdated 2002 - 2009Laila SarhanNo ratings yet

- Financial Accounting AssignmentDocument11 pagesFinancial Accounting AssignmentAnish Agarwal0% (1)

- 0452 s06 QP 1Document12 pages0452 s06 QP 1Omar BilalNo ratings yet

- 12 Accountancy Sp02Document15 pages12 Accountancy Sp02Rahul PareekNo ratings yet

- 35 Basic Accounting Test QuestionsDocument9 pages35 Basic Accounting Test QuestionsDenny OctavianoNo ratings yet

- Financial Accounting and Reporting A Global Perspective 5th Edition Stolowy Test BankDocument6 pagesFinancial Accounting and Reporting A Global Perspective 5th Edition Stolowy Test Bankjessicapatelojgsfyqmbt100% (13)

- FORM FOUR EJE BOOKKEEPING EXAM REVIEWDocument7 pagesFORM FOUR EJE BOOKKEEPING EXAM REVIEWNassrah JumaNo ratings yet

- HKABE 2014-15 Paper 1 QuestionDocument14 pagesHKABE 2014-15 Paper 1 QuestionChan Wai KuenNo ratings yet

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- Soal Latihan Chapter 16Document8 pagesSoal Latihan Chapter 16Alifia Aprizila0% (2)

- Acctg7 - CH 8Document22 pagesAcctg7 - CH 8Jao FloresNo ratings yet

- Balance Sheet Analysis:: Financial Accounting AssignmentDocument2 pagesBalance Sheet Analysis:: Financial Accounting AssignmentadirisinNo ratings yet

- Business Math Module 5 Mortgage and AmortizationDocument7 pagesBusiness Math Module 5 Mortgage and AmortizationMishka AlascaNo ratings yet

- FAC Accounting CycleDocument14 pagesFAC Accounting Cycleshubh jainNo ratings yet

- JIM Lucknow Group Project on Tuni Anakapalli Annuity Road ProjectDocument12 pagesJIM Lucknow Group Project on Tuni Anakapalli Annuity Road ProjectNitanshi SinghNo ratings yet

- Manila Metal Container Corp. v. PNBDocument2 pagesManila Metal Container Corp. v. PNBAbigail Tolabing100% (2)

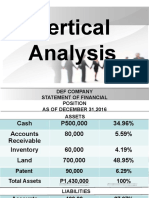

- Vertical analysis of DEF Company's financial statementsDocument8 pagesVertical analysis of DEF Company's financial statementsHannah Mae BautistaNo ratings yet

- Cred Trans NotesDocument26 pagesCred Trans NotesBuen LibetarioNo ratings yet

- Accounting For Management-1 Unit 3 Final Accounts of Sole ProprietorshipDocument33 pagesAccounting For Management-1 Unit 3 Final Accounts of Sole Proprietorshipkuldeeprathore612994No ratings yet

- Personal Monthly Budget1Document3 pagesPersonal Monthly Budget1Olivia OctoficeNo ratings yet

- Solved Alpine Corporation Is A Qualified Small Business Corporation Eligible To PDFDocument1 pageSolved Alpine Corporation Is A Qualified Small Business Corporation Eligible To PDFAnbu jaromiaNo ratings yet

- 01 - Financial StatementsDocument6 pages01 - Financial Statementsjoubert andresNo ratings yet

- Double-Entry Bookkeeping ExplainedDocument5 pagesDouble-Entry Bookkeeping ExplainedSarah Santos100% (5)

- Balance Sheet of State Bank of IndiaDocument9 pagesBalance Sheet of State Bank of IndiaSnehal TanksaleNo ratings yet

- Assignment 3Document3 pagesAssignment 3Nate LoNo ratings yet

- Takaful Myclick Term PDSDocument3 pagesTakaful Myclick Term PDSLan MazlanNo ratings yet

- The Accounting EquationDocument2 pagesThe Accounting Equation7a4374 hisNo ratings yet

- INGLES II Pag. 148 and 149Document3 pagesINGLES II Pag. 148 and 149Paola Pinedo Garcia100% (1)

- The Millionaire FastlaneDocument5 pagesThe Millionaire FastlaneRares Apastasoaiei0% (1)

- 5 - Capital Investment Appraisal (Part-2)Document10 pages5 - Capital Investment Appraisal (Part-2)Fahim HussainNo ratings yet

- Solutiondone 2-234Document1 pageSolutiondone 2-234trilocksp SinghNo ratings yet

- Time Value of Money-2Document33 pagesTime Value of Money-2Moe HanNo ratings yet

- Question 1061345Document11 pagesQuestion 1061345rocking guys yoNo ratings yet

- Chapter 2: Analysis of CAMELS On Eastern Bank Limited: 2.1 Capital AdequacyDocument11 pagesChapter 2: Analysis of CAMELS On Eastern Bank Limited: 2.1 Capital AdequacyShaikh Saifullah KhalidNo ratings yet

- Chapter 14 - Long Term Liabilities (Bonds & Notes)Document90 pagesChapter 14 - Long Term Liabilities (Bonds & Notes)agnesanantasyaNo ratings yet

- CT1 2017Document1 pageCT1 2017Emai TetsNo ratings yet

- Lesson 5 (Semis)Document10 pagesLesson 5 (Semis)Joesil Dianne SempronNo ratings yet

- A Study On Recent Trend in Home Loan: ISSN 2651-4451 - e-ISSN 2651-446XDocument7 pagesA Study On Recent Trend in Home Loan: ISSN 2651-4451 - e-ISSN 2651-446XGajanan PadamgirwarNo ratings yet

- Exercises of Cash Liquidity ManagementDocument8 pagesExercises of Cash Liquidity ManagementTâm ThuNo ratings yet