You might also like

- Economic Indicators for South and Central Asia: Input–Output TablesFrom EverandEconomic Indicators for South and Central Asia: Input–Output TablesNo ratings yet

- Stove Kraft LimitedDocument7 pagesStove Kraft LimitedSiddharth Rai SuranaNo ratings yet

- Tube Investments of India LimitedDocument8 pagesTube Investments of India Limitedpraveen kumarNo ratings yet

- KEI Industries LimitedDocument8 pagesKEI Industries Limitedpraveen kumarNo ratings yet

- Genus Electrotech - R - 17052019Document7 pagesGenus Electrotech - R - 17052019Puneet367No ratings yet

- Bikanervala Foods Private Limited: Summary of Rated InstrumentsDocument7 pagesBikanervala Foods Private Limited: Summary of Rated InstrumentsDarshan ShahNo ratings yet

- Godrej Properties LimitedDocument11 pagesGodrej Properties Limitedkitono5817No ratings yet

- V-Guard Industries - R - 10052019Document8 pagesV-Guard Industries - R - 10052019Yogi173No ratings yet

- Deepak Nitrite R 22082019Document7 pagesDeepak Nitrite R 22082019SalmanNo ratings yet

- Barbeque Nation Hospitality LimitedDocument7 pagesBarbeque Nation Hospitality Limitednayabrasul208No ratings yet

- Sahyadri Industries LimitedDocument7 pagesSahyadri Industries LimitedficiveNo ratings yet

- Gokak Textiles Limited: Ratings Reaffirmed Long-Term Rating Withdrawn Summary of Rating ActionDocument6 pagesGokak Textiles Limited: Ratings Reaffirmed Long-Term Rating Withdrawn Summary of Rating Actionabhi MestriNo ratings yet

- Godrej Industries LimitedDocument8 pagesGodrej Industries LimitedJigarNo ratings yet

- VE Commercial Vehicles LimitedDocument8 pagesVE Commercial Vehicles LimitedRajNo ratings yet

- Home First Finance Company India LimitedDocument8 pagesHome First Finance Company India LimitedRAROLINKSNo ratings yet

- A One Steel Alloys 10may2021Document7 pagesA One Steel Alloys 10may2021L KNo ratings yet

- MPlastics Toys and Engineering Private LimitedDocument9 pagesMPlastics Toys and Engineering Private Limitedshihabshibu105No ratings yet

- KrazyBee Services Private LimitedDocument9 pagesKrazyBee Services Private LimitedBalakrishnan IyerNo ratings yet

- Zetwerk Manufacturing Businesses PVT LTDDocument8 pagesZetwerk Manufacturing Businesses PVT LTDrahulappikatlaNo ratings yet

- Padget Electronics Pvt. LTDDocument9 pagesPadget Electronics Pvt. LTDvenkyniyerNo ratings yet

- Big Bags International PVT LTDDocument7 pagesBig Bags International PVT LTDnayabrasul208No ratings yet

- Vivriti Capital Private Limited PDFDocument9 pagesVivriti Capital Private Limited PDFIb SulochanaNo ratings yet

- L.G. Balakrishnan & Bros Limited: Summary of Rating ActionDocument7 pagesL.G. Balakrishnan & Bros Limited: Summary of Rating ActionChromoNo ratings yet

- Subros LimitedDocument8 pagesSubros LimitedrajpersonalNo ratings yet

- Zinka Logistics Solutions - R-25092020Document8 pagesZinka Logistics Solutions - R-25092020Atiqur Rahman BarbhuiyaNo ratings yet

- Gold Plus ICRA April 2019Document8 pagesGold Plus ICRA April 2019Puneet367No ratings yet

- CTR Manufacturing Industries Private LimitedDocument7 pagesCTR Manufacturing Industries Private Limitedkrushna.maneNo ratings yet

- Triveni ICRA March 2024Document9 pagesTriveni ICRA March 2024Puneet367No ratings yet

- Alkali Metals Limited - R - 26112020Document7 pagesAlkali Metals Limited - R - 26112020Yogi173No ratings yet

- Olectra Greentech Limited - R - 27082020Document8 pagesOlectra Greentech Limited - R - 27082020eichermguptaNo ratings yet

- Shilchar_Technologies_LimitedDocument5 pagesShilchar_Technologies_Limitedjaikumar608jainNo ratings yet

- DCW Limited - June 2021Document8 pagesDCW Limited - June 2021SaranNo ratings yet

- MSL Driveline Systems - R - 16102020Document8 pagesMSL Driveline Systems - R - 16102020DarshanNo ratings yet

- SJS Enterprises LimitedDocument7 pagesSJS Enterprises LimitedCA Ankur BariaNo ratings yet

- Shaily Engineering Plastics Limited-09-25-2019Document4 pagesShaily Engineering Plastics Limited-09-25-2019Ashutosh Gupta100% (1)

- Khadim India Limited - ICRA Feb 2020 PDFDocument7 pagesKhadim India Limited - ICRA Feb 2020 PDFPuneet367No ratings yet

- Hikal Limited - R - 21122020Document8 pagesHikal Limited - R - 21122020CA.Chandra SekharNo ratings yet

- Bharat Forge LimitedDocument7 pagesBharat Forge LimitedjagadeeshNo ratings yet

- Varsha Industries-R-19072018 PDFDocument7 pagesVarsha Industries-R-19072018 PDFKunal DamaniNo ratings yet

- Champion Commercial Company LimitedDocument7 pagesChampion Commercial Company LimitedCedric KerkettaNo ratings yet

- Ganga Rasayanie Private Limited-R-10102019Document7 pagesGanga Rasayanie Private Limited-R-10102019DarshanNo ratings yet

- Stove Kraft Initiating CoverageDocument30 pagesStove Kraft Initiating Coverageprat wNo ratings yet

- Y-Wildcraft-India-18Oct 2022Document8 pagesY-Wildcraft-India-18Oct 2022PratyushNo ratings yet

- Kitex Garments LimitedDocument8 pagesKitex Garments LimitedSamsuzzoha ZohaNo ratings yet

- Udaipur Cement Works receives rating reaffirmationDocument6 pagesUdaipur Cement Works receives rating reaffirmationflying400No ratings yet

- EKI Energy Services LimitedDocument8 pagesEKI Energy Services LimitedTarun 199No ratings yet

- STEER Engineering Private Limited: Summary of Rated InstrumentsDocument7 pagesSTEER Engineering Private Limited: Summary of Rated InstrumentsNarendranNo ratings yet

- United Breweries Limited: Summary of Rated InstrumentsDocument8 pagesUnited Breweries Limited: Summary of Rated InstrumentsKaushikDasguptaNo ratings yet

- Rockman Industries Jan 2020 ICRADocument9 pagesRockman Industries Jan 2020 ICRAPuneet367No ratings yet

- Som Distilleries & Breweries LimitedDocument7 pagesSom Distilleries & Breweries LimitedhamsNo ratings yet

- Muthoot Finance LimitedDocument11 pagesMuthoot Finance LimitedKhasimvali ShaikNo ratings yet

- Sahyadri Farmers Producer Company LimitedDocument9 pagesSahyadri Farmers Producer Company LimitedKamlakar AvhadNo ratings yet

- Saakha Steel Industries Private Limited Bank Facilities Rating ReaffirmedDocument4 pagesSaakha Steel Industries Private Limited Bank Facilities Rating ReaffirmedRanib SainjuNo ratings yet

- 06 - Aditi Jhanwar MFS Presentation PDFDocument21 pages06 - Aditi Jhanwar MFS Presentation PDFAditi JhanwarNo ratings yet

- Kalyan Jewellers India LimitedDocument8 pagesKalyan Jewellers India LimitedArunachalamNo ratings yet

- Luxor Writing Instruments Pvt. LtdDocument7 pagesLuxor Writing Instruments Pvt. Ltdbookdekho.ytNo ratings yet

- Y-Wildcraft-India-18Oct 2022Document8 pagesY-Wildcraft-India-18Oct 2022PratyushNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Jupiter International LimitedDocument6 pagesJupiter International LimitedRahul syalNo ratings yet

- Ajanta Soya 13may2021Document7 pagesAjanta Soya 13may2021praveen kumarNo ratings yet

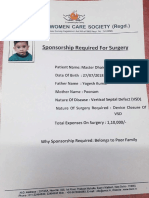

- Sponsorship Required For SurgeryDocument3 pagesSponsorship Required For Surgeryflying400No ratings yet

- Panama Petrochem LTDDocument7 pagesPanama Petrochem LTDflying400No ratings yet

- Udaipur Cement Works receives rating reaffirmationDocument6 pagesUdaipur Cement Works receives rating reaffirmationflying400No ratings yet

- Morning Cuppa 02-Sep - 202109020833360357037Document2 pagesMorning Cuppa 02-Sep - 202109020833360357037flying400No ratings yet

- Notice of Shareholders Part2Document49 pagesNotice of Shareholders Part2flying400No ratings yet

- PAR/CS/NSE/2020-21/41 Investor PresentationDocument28 pagesPAR/CS/NSE/2020-21/41 Investor Presentationflying400No ratings yet

- Par Drugs Investor Presentation June 2021Document27 pagesPar Drugs Investor Presentation June 2021flying400No ratings yet

- Chaman Lal Setia Exports Ltd Coverage InitiationDocument14 pagesChaman Lal Setia Exports Ltd Coverage Initiationflying400No ratings yet

- BUC Signature Price Update 2&3 Price List-1Document1 pageBUC Signature Price Update 2&3 Price List-1flying400No ratings yet

- Press Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1flying400No ratings yet

- Conversion of Unit - BTR - Yogini DasaDocument7 pagesConversion of Unit - BTR - Yogini Dasaflying4000% (1)

- Morning Cuppa 02-Sep - 202109020833360357037Document2 pagesMorning Cuppa 02-Sep - 202109020833360357037flying400No ratings yet

- HSIL LTD - Initiating Coverage - 19.07.2021Document20 pagesHSIL LTD - Initiating Coverage - 19.07.2021flying400No ratings yet

- Morning Cuppa 02-Sep - 202109020833360357037Document2 pagesMorning Cuppa 02-Sep - 202109020833360357037flying400No ratings yet

- Sector Momentum Cement-202104120837409214783Document4 pagesSector Momentum Cement-202104120837409214783flying400No ratings yet

- Morning Cuppa 08-Oct-202110080838430715214Document2 pagesMorning Cuppa 08-Oct-202110080838430715214flying400No ratings yet

- Good Food Is A Foundation of Genuine HappinessDocument1 pageGood Food Is A Foundation of Genuine Happinessflying400No ratings yet

- Pidilite Industries LTD Q3FY21 Results Comment-202102091351131334013Document5 pagesPidilite Industries LTD Q3FY21 Results Comment-202102091351131334013flying400No ratings yet

- Minda Industries - Q2FY21 - Result Update-202011180844080344898Document3 pagesMinda Industries - Q2FY21 - Result Update-202011180844080344898flying400No ratings yet

- Circular-Covid Guidelines SingaporeDocument1 pageCircular-Covid Guidelines Singaporeflying400No ratings yet

- Initiating Coverage - Minda Industries - 31032021-202104010924403625674Document20 pagesInitiating Coverage - Minda Industries - 31032021-202104010924403625674flying400No ratings yet

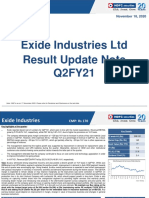

- Exide Industries - Q2FY21 - Result Update-202011180843475979442Document3 pagesExide Industries - Q2FY21 - Result Update-202011180843475979442flying400No ratings yet

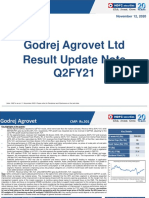

- Godrej Agrovet - Q2FY21 - Result Update-202011121115478067231Document3 pagesGodrej Agrovet - Q2FY21 - Result Update-202011121115478067231flying400No ratings yet

- Sectoral Index Report Banking 07042020 202004070809432449396 PDFDocument4 pagesSectoral Index Report Banking 07042020 202004070809432449396 PDFflying400No ratings yet

- ENIL - Q2FY21 - Result Update-202011121115240362085Document3 pagesENIL - Q2FY21 - Result Update-202011121115240362085flying400No ratings yet

- Sectoral Index Report Banking 07042020 202004070809432449396 PDFDocument4 pagesSectoral Index Report Banking 07042020 202004070809432449396 PDFflying400No ratings yet

- Mahindra & Mahindra LTD Result Update Note Q2FY21: November 18, 2020Document3 pagesMahindra & Mahindra LTD Result Update Note Q2FY21: November 18, 2020flying400No ratings yet

- Strategy For Investors in Turbulent COVID 19 Times and Stockpicks For Staggered Investment-202003310858403601796 PDFDocument9 pagesStrategy For Investors in Turbulent COVID 19 Times and Stockpicks For Staggered Investment-202003310858403601796 PDFflying400No ratings yet

- Stock To Trade On Bounces 202003300855158325372Document6 pagesStock To Trade On Bounces 202003300855158325372flying400No ratings yet

- Exercise 1. Choose the correct alternative to complete each sentence: Money TermsDocument8 pagesExercise 1. Choose the correct alternative to complete each sentence: Money TermsGliqeria PlasariNo ratings yet

- Understanding the Maceda Law in the PhilippinesDocument3 pagesUnderstanding the Maceda Law in the PhilippinesERZZAHC SETERNo ratings yet

- Chap 005-Interest Rates and Bond ValuationDocument43 pagesChap 005-Interest Rates and Bond Valuationsarvenaz kamali matin100% (1)

- Special journals optimize recording transactionsDocument25 pagesSpecial journals optimize recording transactionsYuu100% (1)

- Additional Notes For Adjustments To The Financial StatementsDocument2 pagesAdditional Notes For Adjustments To The Financial StatementsDebbie DebzNo ratings yet

- Fin 464 Final TSA PDF PDFDocument67 pagesFin 464 Final TSA PDF PDFArahf KashemiNo ratings yet

- CSEC June 2008 Mathematics P1Document11 pagesCSEC June 2008 Mathematics P1Tamera GreenNo ratings yet

- Macalinao vs. Bank of The Philippine Islands, 600 SCRA 67 (2009)Document12 pagesMacalinao vs. Bank of The Philippine Islands, 600 SCRA 67 (2009)Jennifer ArcadioNo ratings yet

- Wassim Zhani Income Taxation of Corporations (Chapter 10)Document24 pagesWassim Zhani Income Taxation of Corporations (Chapter 10)wassim zhaniNo ratings yet

- Intermediate Accounting IFRS Edition: Kieso, Weygandt, WarfieldDocument76 pagesIntermediate Accounting IFRS Edition: Kieso, Weygandt, WarfieldĐức Huy100% (1)

- Financial Ratios and AnalysisDocument3 pagesFinancial Ratios and AnalysisMariane Centino BoholNo ratings yet

- Group 14 FI CaseStudy ReportGuidelineDocument19 pagesGroup 14 FI CaseStudy ReportGuidelinenkminh19082003No ratings yet

- Public Auction: Will Sell The Property Described Below byDocument10 pagesPublic Auction: Will Sell The Property Described Below byDS ChongNo ratings yet

- Chap-16-Lending Policies and ProceduresDocument28 pagesChap-16-Lending Policies and ProceduresShahin RahmanNo ratings yet

- Vinod SharmaDocument4 pagesVinod Sharmav9d.vsharmaNo ratings yet

- Khan Singh Vs Tek Chand 1968Document6 pagesKhan Singh Vs Tek Chand 1968Anurag guptaNo ratings yet

- Money N Banking 2Document6 pagesMoney N Banking 2Shreya PushkarnaNo ratings yet

- SC upholds CA ruling that transaction between Vives and Doronilla was commodatum loanDocument10 pagesSC upholds CA ruling that transaction between Vives and Doronilla was commodatum loanAbbygaleOmbaoNo ratings yet

- OT CobobliDocument77 pagesOT CobobliJohn Jet TanNo ratings yet

- Types of Business Structure: Group 4Document16 pagesTypes of Business Structure: Group 4DENGDENG HUANGNo ratings yet

- ACC2054 Tutorial 3Document3 pagesACC2054 Tutorial 3Euvan KumarNo ratings yet

- Acct 3Document12 pagesAcct 3Annie RapanutNo ratings yet

- Accounting Cycle: From Filipino Accounting Tutorial (YT)Document10 pagesAccounting Cycle: From Filipino Accounting Tutorial (YT)Gesther Djeane M. SorianoNo ratings yet

- Financial FAQs on URUS ProgrammeDocument12 pagesFinancial FAQs on URUS ProgrammeKhalis Munzir KhazinNo ratings yet

- Dwnload Full Accounting Volume 1 Canadian 9th Edition Horngren Solutions Manual PDFDocument36 pagesDwnload Full Accounting Volume 1 Canadian 9th Edition Horngren Solutions Manual PDFsynomocyeducable6pyb8k100% (16)

- Financial Literacy: Reporters: Cerado, Fredisvenda Allyssa M. Josol, Kum Hyeon S. Venus, Jennifer G. Yambao, MaribethDocument17 pagesFinancial Literacy: Reporters: Cerado, Fredisvenda Allyssa M. Josol, Kum Hyeon S. Venus, Jennifer G. Yambao, MaribethAbby Yambao100% (1)

- JN Development vs. Philippine Export and Foreign Loan Guarantee CorpDocument11 pagesJN Development vs. Philippine Export and Foreign Loan Guarantee CorpspNo ratings yet

- Treasury Management Policy SummaryDocument23 pagesTreasury Management Policy Summary李森No ratings yet

- AUD 323 Auditing & Assurance: Concepts & ApplicationsDocument33 pagesAUD 323 Auditing & Assurance: Concepts & ApplicationsYvone Claire Fernandez SalmorinNo ratings yet

- Rural Bank Mortgage Dispute ResolvedDocument18 pagesRural Bank Mortgage Dispute ResolvedAtty. R. PerezNo ratings yet