You might also like

- Marketable Securities and Deferred Taxes: GendaDocument13 pagesMarketable Securities and Deferred Taxes: Gendabipinyadav31100% (2)

- Investment Securities Classification On Balance SheetDocument2 pagesInvestment Securities Classification On Balance Sheetfawad101No ratings yet

- Understanding Balance SheetsDocument26 pagesUnderstanding Balance SheetsAli AhmedNo ratings yet

- Invest in Debt and Equity SecuritiesDocument38 pagesInvest in Debt and Equity SecuritiesGaluh Boga KuswaraNo ratings yet

- Marketable SecuritiesDocument18 pagesMarketable Securitiesammaramansoor133% (3)

- Intermediate Accounting Chapter 12Document64 pagesIntermediate Accounting Chapter 12Kevin DenNo ratings yet

- CH 12 Powerpoint A334Document62 pagesCH 12 Powerpoint A334ThiNo ratings yet

- Accounting For Marketable SecuritiesDocument13 pagesAccounting For Marketable Securitiessaba gul rehmatNo ratings yet

- FIN 408 - Ch.1Document24 pagesFIN 408 - Ch.1Shohidul Islam SaykatNo ratings yet

- Accounting for Investment SecuritiesDocument9 pagesAccounting for Investment Securitiesxpac_53No ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildStory pizzieNo ratings yet

- Chapter 12Document45 pagesChapter 12gottwins05No ratings yet

- 408 01Document24 pages408 01Anna MahmudNo ratings yet

- CFA Level 1 - Section 8 AssetsDocument29 pagesCFA Level 1 - Section 8 Assetsapi-3763138100% (1)

- Analyzing Investing Activities: Intercorporate InvestmentsDocument34 pagesAnalyzing Investing Activities: Intercorporate InvestmentsVeenesha MuralidharanNo ratings yet

- Second Quarter 2010 Earnings PresentationDocument24 pagesSecond Quarter 2010 Earnings PresentationNeha LoyaNo ratings yet

- Impairment of Assets: Students Name Ameera Al - Shdeifat Mahmood Al - Saad Ahmad RadaydehDocument28 pagesImpairment of Assets: Students Name Ameera Al - Shdeifat Mahmood Al - Saad Ahmad Radaydehahmad RadaidehNo ratings yet

- Investments and International Operations: QuestionsDocument52 pagesInvestments and International Operations: QuestionsCh Radeel MurtazaNo ratings yet

- Mark To Market - AccountingDocument11 pagesMark To Market - Accountinggabby209No ratings yet

- FM (Bringing Together Risk and Return)Document30 pagesFM (Bringing Together Risk and Return)Nicko C. NocejaNo ratings yet

- Ch4 SolutionsDocument23 pagesCh4 SolutionsFahad Batavia100% (1)

- B - Understanding Bank FS Part 2Document31 pagesB - Understanding Bank FS Part 2PROMIT CHAKRABORTYNo ratings yet

- Other Comprehensive IncomeDocument5 pagesOther Comprehensive Incometikki0219No ratings yet

- Cash & Debt Free: Understanding Net Debt, Cash Like Items, Debt Like Items, and MoreDocument30 pagesCash & Debt Free: Understanding Net Debt, Cash Like Items, Debt Like Items, and MoreReza HaryoNo ratings yet

- Marketable Securities AccountingDocument5 pagesMarketable Securities AccountingZAKAYO NJONYNo ratings yet

- Chap 005Document41 pagesChap 005Loser Neet100% (1)

- Financial Statement Analysis: K R Subramanyam John J WildDocument39 pagesFinancial Statement Analysis: K R Subramanyam John J WildGilang W Indrasta0% (1)

- Ch06-Teo AkDocument60 pagesCh06-Teo AkNaadiyah SalsabillahNo ratings yet

- FIN 201 Chapter 02Document27 pagesFIN 201 Chapter 02ImraanHossainAyaanNo ratings yet

- CH 17Document121 pagesCH 17diva4khrist06100% (1)

- Trading CompsDocument8 pagesTrading CompsLeonardoNo ratings yet

- Yield IncomeDocument22 pagesYield IncomejNo ratings yet

- Chapter 11 Capital N SurplusDocument12 pagesChapter 11 Capital N SurplusCiciNo ratings yet

- Bab 9 AkmDocument44 pagesBab 9 Akmcaesara geniza ghildaNo ratings yet

- Analyzing Investing Activities: Intercorporate InvestmentsDocument38 pagesAnalyzing Investing Activities: Intercorporate Investmentsshldhy100% (1)

- Dividend Swaps and Futures - Colin Bennett PDFDocument48 pagesDividend Swaps and Futures - Colin Bennett PDFArnaud AmatoNo ratings yet

- Week 9&10Document83 pagesWeek 9&10antoniusyoma007No ratings yet

- Notes To Consolidated Financial Statements: 34 Wal-Mart 2009 Annual ReportDocument26 pagesNotes To Consolidated Financial Statements: 34 Wal-Mart 2009 Annual ReportPrithivi RajNo ratings yet

- Chris Christina Elissa KlueverDocument22 pagesChris Christina Elissa Kluevervisa_kpNo ratings yet

- Linear Technology Dividend Policy and Shareholder ValueDocument4 pagesLinear Technology Dividend Policy and Shareholder ValueAmrinder SinghNo ratings yet

- Financial Planning and Forecasting Financial StatementsDocument70 pagesFinancial Planning and Forecasting Financial StatementsAziz Hotelwala100% (1)

- Lecture 2Document21 pagesLecture 2Dvea ShippinNo ratings yet

- SS&C GlobeOp - FA ModuleDocument34 pagesSS&C GlobeOp - FA ModuleAnil Dube100% (1)

- Kohler DCF Control Prem and DiscDocument6 pagesKohler DCF Control Prem and Discapi-239586293No ratings yet

- Sources of Finance & Capital StructureDocument66 pagesSources of Finance & Capital StructurejkwabenaNo ratings yet

- Investment On SecuritiesDocument22 pagesInvestment On SecuritiesXiu MinNo ratings yet

- Lesson # 21 Indirect Investing Contd Exchange-Traded Funds (Etfs)Document3 pagesLesson # 21 Indirect Investing Contd Exchange-Traded Funds (Etfs)Rajesh KumarNo ratings yet

- Lesson-2 - Compatibility ModeDocument26 pagesLesson-2 - Compatibility Modesanjaya de silvaNo ratings yet

- Assignment 1: Accounting Policies For Reporting IncomeDocument9 pagesAssignment 1: Accounting Policies For Reporting IncomesrystalNo ratings yet

- Pert 9. Equity 9.5 Equity Components in The Financial Statement and Its Underlying ConceptsDocument5 pagesPert 9. Equity 9.5 Equity Components in The Financial Statement and Its Underlying Conceptssoul sistNo ratings yet

- Solution Manual For Financial Statement Analysis and Valuation 2nd Edition by EastonDocument32 pagesSolution Manual For Financial Statement Analysis and Valuation 2nd Edition by EastonJenniferPalmerdqwf98% (43)

- Presented by Amir KhanDocument66 pagesPresented by Amir KhanHassaan BillahNo ratings yet

- SPDR Barclays Capital Aggregate Bond ETF (LAG)Document2 pagesSPDR Barclays Capital Aggregate Bond ETF (LAG)Roberto PerezNo ratings yet

- Deck How To Trade SlidesDocument39 pagesDeck How To Trade SlidesN.a. M. TandayagNo ratings yet

- LO4 - Ratios Notes and ExercisesDocument23 pagesLO4 - Ratios Notes and ExercisesLudmila DorojanNo ratings yet

- InvestmentDocument16 pagesInvestmentYakini entertainmentNo ratings yet

- Chapter 8 PDFDocument62 pagesChapter 8 PDFgetasewNo ratings yet

- Active Investing Notes PDFDocument45 pagesActive Investing Notes PDFSunanda KeerNo ratings yet

- 1 IFRS 9 - Financial InstrumentsDocument31 pages1 IFRS 9 - Financial InstrumentsSharmaineMirandaNo ratings yet

- Zagada Vs Civil Service Commission, 216 SCRA 114, G.R. No. 99302, Nov. 27, 1992Document12 pagesZagada Vs Civil Service Commission, 216 SCRA 114, G.R. No. 99302, Nov. 27, 1992Gi NoNo ratings yet

- Zamora Vs CaballeroDocument30 pagesZamora Vs CaballeroLu CasNo ratings yet

- Villanueva Vs Judicial & Bar Council, 755 SCRA 182, G.R. No. 211833, April 7, 2015Document63 pagesVillanueva Vs Judicial & Bar Council, 755 SCRA 182, G.R. No. 211833, April 7, 2015Gi NoNo ratings yet

- Valencia Vs Peralta, JR., 118 Phil 691, G.R. No. L-20864, August 23, 1963Document2 pagesValencia Vs Peralta, JR., 118 Phil 691, G.R. No. L-20864, August 23, 1963Gi NoNo ratings yet

- World Health Org. Vs Aquino, 48 SCRA 242, G.R. No. L-35131, Nov. 29, 1972Document17 pagesWorld Health Org. Vs Aquino, 48 SCRA 242, G.R. No. L-35131, Nov. 29, 1972Gi NoNo ratings yet

- Vasco vs. Court of AppealsDocument7 pagesVasco vs. Court of AppealsKayla Marie PaclibarNo ratings yet

- Ygay Vs Escareal, 135 SCRA 78, G.R. No. 44189, Feb. 8, 1985Document8 pagesYgay Vs Escareal, 135 SCRA 78, G.R. No. 44189, Feb. 8, 1985Gi NoNo ratings yet

- Ynot Vs Intermediate Appellate Court, 148 SCRA 659, G.R. No. L-74457, March 20, 1987Document19 pagesYnot Vs Intermediate Appellate Court, 148 SCRA 659, G.R. No. L-74457, March 20, 1987Gi NoNo ratings yet

- Valencia Vs Locquiao, 412 SCRA 600, G.R. No. 122134, October 3, 2003Document16 pagesValencia Vs Locquiao, 412 SCRA 600, G.R. No. 122134, October 3, 2003Gi NoNo ratings yet

- Villena Vs Secretary of Interior, 67 Phil 451, G.R. No. L-46570, April 21, 1939Document9 pagesVillena Vs Secretary of Interior, 67 Phil 451, G.R. No. L-46570, April 21, 1939Gi NoNo ratings yet

- 03 - Ynot vs. Intermediate Appellate CourtDocument20 pages03 - Ynot vs. Intermediate Appellate CourtMaria Bernadette PedroNo ratings yet

- Reyes Vs ChiongDocument2 pagesReyes Vs ChiongLu CasNo ratings yet

- Valmores Vs Achacoso and Cabildo, 831 SCRA 442, G.R. No. 217453, July 19, 2017Document28 pagesValmores Vs Achacoso and Cabildo, 831 SCRA 442, G.R. No. 217453, July 19, 2017Lu CasNo ratings yet

- Wright Vs Tinio, 91 Phil 919, G.R. No. L-4004, May 29, 1952Document2 pagesWright Vs Tinio, 91 Phil 919, G.R. No. L-4004, May 29, 1952Lu CasNo ratings yet

- US Vs Ney and BosqueDocument2 pagesUS Vs Ney and BosqueLu CasNo ratings yet

- Re 1989 ElectionsDocument3 pagesRe 1989 ElectionsLu CasNo ratings yet

- 019GMA Network Vs Commission On Elections, 734 SCRA 88, G.R. No. 205357, September 2, 2014Document165 pages019GMA Network Vs Commission On Elections, 734 SCRA 88, G.R. No. 205357, September 2, 2014Lu CasNo ratings yet

- In Re Felipe Del Rosario FactsDocument1 pageIn Re Felipe Del Rosario FactsLu CasNo ratings yet

- Requesting Exemption From PaymentDocument2 pagesRequesting Exemption From PaymentLu CasNo ratings yet

- Garcia Vs LopezDocument2 pagesGarcia Vs LopezLu CasNo ratings yet

- Petition For Disbarment of Telesforo A. DiaoDocument2 pagesPetition For Disbarment of Telesforo A. DiaoLu CasNo ratings yet

- Zaguirre Vs CastilloDocument2 pagesZaguirre Vs CastilloLu CasNo ratings yet

- Barandon Jr. Vs Ferrer Sr.Document3 pagesBarandon Jr. Vs Ferrer Sr.Lu Cas100% (1)

- Laput Vs RemotigueDocument2 pagesLaput Vs RemotigueLu CasNo ratings yet

- In The Matter of The Integration of The Bar of The PhilippinesDocument1 pageIn The Matter of The Integration of The Bar of The Philippines11 : 28No ratings yet

- Santos Jr. Vs LlamasDocument2 pagesSantos Jr. Vs LlamasLu CasNo ratings yet

- Saburnido Vs MadronoDocument2 pagesSaburnido Vs MadronoLu CasNo ratings yet

- Atty Suspended for Misusing Client Funds, Registering Client's Car Under ChildrenDocument2 pagesAtty Suspended for Misusing Client Funds, Registering Client's Car Under ChildrenGi NoNo ratings yet

- In Re Investigation of Angel Parazo For Alleged Leakage of Questions in Some Subjects in The 1948 Bar Examinations FactsDocument2 pagesIn Re Investigation of Angel Parazo For Alleged Leakage of Questions in Some Subjects in The 1948 Bar Examinations FactsLu CasNo ratings yet

- Leda Vs TabangDocument2 pagesLeda Vs TabangLu Cas0% (1)

- The Case of Enron: A Scandal of Accounting Fraud and Unethical PracticesDocument4 pagesThe Case of Enron: A Scandal of Accounting Fraud and Unethical PracticesKhadija AkterNo ratings yet

- Review of Corporate Hedging PolicyDocument10 pagesReview of Corporate Hedging PolicyIngrid Levana GunawanNo ratings yet

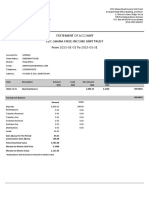

- Edc Ghana Fixed Income Unit Trust Statement of Account: Redemptions Shall Be Based On Marked-to-Market ValueDocument2 pagesEdc Ghana Fixed Income Unit Trust Statement of Account: Redemptions Shall Be Based On Marked-to-Market ValueAdepa IdasonNo ratings yet

- Understanding Financial InstrumentsDocument11 pagesUnderstanding Financial InstrumentsMaria G. BernardinoNo ratings yet

- The Rise and Fall of Enron PDFDocument8 pagesThe Rise and Fall of Enron PDFsuriya vasanth bNo ratings yet

- Enron Assignment - Dharit Gajjar (SSB10A07)Document13 pagesEnron Assignment - Dharit Gajjar (SSB10A07)manishpunjabiNo ratings yet

- Statement 05312019Document6 pagesStatement 05312019Marcus GreenNo ratings yet

- Barth, M.E., Landsman, W.R. & Wahlen, J.M. (1995). Fair value accounting: Effects on banks’ earnings volatility, regulatory capital and value of contractual cash flows. Journal of Banking and Finance, 19, 577-605.Document29 pagesBarth, M.E., Landsman, W.R. & Wahlen, J.M. (1995). Fair value accounting: Effects on banks’ earnings volatility, regulatory capital and value of contractual cash flows. Journal of Banking and Finance, 19, 577-605.Marchelyn PongsapanNo ratings yet

- Enron Poste RaDocument16 pagesEnron Poste RaAndreea VioletaNo ratings yet

- Derivatives Analysis & Valuation ChapterDocument39 pagesDerivatives Analysis & Valuation ChapterDeepika JhaNo ratings yet

- Ifrs 9 - Financial Instruments Review QuestionsDocument9 pagesIfrs 9 - Financial Instruments Review QuestionsHamad Sadiq100% (1)

- IFFEM Lesson I (Prof. Schlitzer)Document59 pagesIFFEM Lesson I (Prof. Schlitzer)Mau EmbateNo ratings yet

- Derivatives and Risk Management JP Morgan ReportDocument24 pagesDerivatives and Risk Management JP Morgan Reportanirbanccim8493No ratings yet

- Term Paper: Prepared byDocument12 pagesTerm Paper: Prepared byEshfaque Alam DastagirNo ratings yet

- Ia1 5a Investments 15 FVDocument55 pagesIa1 5a Investments 15 FVJm SevallaNo ratings yet

- Role Played by Sebi in Restricting Insider TradingDocument42 pagesRole Played by Sebi in Restricting Insider TradingAbhay Singh ParmarNo ratings yet

- Recognition & Derecognition 5Document27 pagesRecognition & Derecognition 5sajedulNo ratings yet

- Investments at a GlanceDocument55 pagesInvestments at a GlanceJm SevallaNo ratings yet

- ACTG 431 QUIZ Week 2 Theory of Accounts Part 2 - FINANCIAL ASSETS QUIZDocument6 pagesACTG 431 QUIZ Week 2 Theory of Accounts Part 2 - FINANCIAL ASSETS QUIZMarilou Arcillas PanisalesNo ratings yet

- Financial Statement Analysis Case Study 1-1, 1-2Document5 pagesFinancial Statement Analysis Case Study 1-1, 1-2Vikram VaidyanathanNo ratings yet

- Annexure - Financial AccountingDocument14 pagesAnnexure - Financial AccountingAndrea AgliettiNo ratings yet

- Valuation Concepts and Methods IntroductionDocument18 pagesValuation Concepts and Methods IntroductionPatricia Nicole BarriosNo ratings yet

- Sess 19-20 - Fx. ExposureDocument19 pagesSess 19-20 - Fx. ExposureAjay KumarNo ratings yet

- Standalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Document9 pagesStandalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- NISM SERIES 1 – CURRENCY DERIVATIVES CERTIFICATION EXAM – PRACTICE TEST 1Document19 pagesNISM SERIES 1 – CURRENCY DERIVATIVES CERTIFICATION EXAM – PRACTICE TEST 1Neeraj KumarNo ratings yet

- AirAsia Bursa Announcement - Q42017 27feb18 FinalDocument43 pagesAirAsia Bursa Announcement - Q42017 27feb18 FinalHenry Lee0% (1)

- Futures Contract Generic SpecificationsDocument5 pagesFutures Contract Generic SpecificationsPuthpura PuthNo ratings yet

- PFRS 9, Paragraph 4.1.2, Provides That A Financial Asset Shall MeasuredDocument3 pagesPFRS 9, Paragraph 4.1.2, Provides That A Financial Asset Shall MeasuredSwai RosendeNo ratings yet

- Accounting for Investments ClassificationDocument19 pagesAccounting for Investments ClassificationJhon Vincent BuragaNo ratings yet

- R26 CFA Level 3Document12 pagesR26 CFA Level 3Ashna0188No ratings yet