You might also like

- Theory of Interest-Stephen Kellison-Solutions ManualDocument159 pagesTheory of Interest-Stephen Kellison-Solutions ManualGeOrGe GhOsT KoKKiNaKiS84% (43)

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Accountancy Assignment Grade 12Document4 pagesAccountancy Assignment Grade 12sharu SKNo ratings yet

- R27 CFA Level 3Document10 pagesR27 CFA Level 3Ashna0188No ratings yet

- Time For Trust: The Trillion-Dollar Reasons To Rethink BlockchainDocument23 pagesTime For Trust: The Trillion-Dollar Reasons To Rethink BlockchainForkLogNo ratings yet

- FinMa PDFDocument86 pagesFinMa PDFJolex Acid0% (1)

- Accountancy Worksheets 4Document15 pagesAccountancy Worksheets 4devanshubhattacharya018No ratings yet

- Bcom Semester Iii Accounts Mega Revision Cum Suggestion PDFDocument6 pagesBcom Semester Iii Accounts Mega Revision Cum Suggestion PDFAvirup ChakrabortyNo ratings yet

- TP 4 Pa 18 JuneDocument2 pagesTP 4 Pa 18 JuneAditya srivastavaNo ratings yet

- 12th Account 12-7-2019Document2 pages12th Account 12-7-2019Ajay GujjarNo ratings yet

- Partner Ship Accounts - I: Balance Sheet Dr. Cr. Particulars Amount Rs. Particulars Amount RsDocument17 pagesPartner Ship Accounts - I: Balance Sheet Dr. Cr. Particulars Amount Rs. Particulars Amount RsM JEEVARATHNAM NAIDUNo ratings yet

- Admission of A Partner PDFDocument8 pagesAdmission of A Partner PDFSpandan DasNo ratings yet

- Retirement of Partners - Updated WorksheetDocument8 pagesRetirement of Partners - Updated WorksheetMisri SoniNo ratings yet

- Worksheet AdmissionDocument3 pagesWorksheet AdmissionYogesh AdhikariNo ratings yet

- 12 Accounts Summer Vacation Assignment 2022-23Document15 pages12 Accounts Summer Vacation Assignment 2022-23Ashelle DsouzaNo ratings yet

- Worksheet - Retirement & DissolutionDocument4 pagesWorksheet - Retirement & DissolutionYogesh AdhikariNo ratings yet

- Sample Paper Class XII Subject-Accountancy Part ADocument5 pagesSample Paper Class XII Subject-Accountancy Part AKaran BhatnagarNo ratings yet

- REVISION TEST Admission of A PartnerDocument2 pagesREVISION TEST Admission of A PartnerOshvi Shrivastava100% (1)

- Unit 3 Admission of A Partner QuestionsDocument4 pagesUnit 3 Admission of A Partner QuestionsMitesh SethiNo ratings yet

- SEM III - Advanced Accounting (EM)Document4 pagesSEM III - Advanced Accounting (EM)Abdul MalikNo ratings yet

- AccountsDocument14 pagesAccountsshrutichoudhary436No ratings yet

- Retirement WSDocument2 pagesRetirement WSarhamenterprises5401No ratings yet

- 12 2006 Accountancy 1Document5 pages12 2006 Accountancy 1Akash TamuliNo ratings yet

- Retirement of Partners Cbse Question BankDocument6 pagesRetirement of Partners Cbse Question Bankabhayku1689No ratings yet

- Cbse Questions Adm RetirementDocument19 pagesCbse Questions Adm RetirementDeepanshu kaushikNo ratings yet

- Foundation Practice SumsDocument9 pagesFoundation Practice SumsBRISTI SAHANo ratings yet

- PYQ PartnershipDocument11 pagesPYQ Partnershipa86476007No ratings yet

- Book Keeping and AccountancyDocument9 pagesBook Keeping and AccountancyPriyanka SHELKENo ratings yet

- Class 12 CBSE ISC Accountancy Assignment 10Document15 pagesClass 12 CBSE ISC Accountancy Assignment 10studentNo ratings yet

- Accounts Parntership TestDocument6 pagesAccounts Parntership TestdhruvNo ratings yet

- 588c69bdc763b - Sample Paper Accountancy - 230102 - 185610Document7 pages588c69bdc763b - Sample Paper Accountancy - 230102 - 185610sanchitchaudhary431No ratings yet

- XII Acc CW Practice Questions Ch4.4 (Retirement)Document2 pagesXII Acc CW Practice Questions Ch4.4 (Retirement)Vaidehi BagraNo ratings yet

- Accountancy Unit Test 2 - WorksheetDocument12 pagesAccountancy Unit Test 2 - WorksheetFawaz YoosefNo ratings yet

- Board Paper 2018Document14 pagesBoard Paper 2018zaraniyaz14No ratings yet

- 1Document5 pages1firoozdasmanNo ratings yet

- PartnershipDocument10 pagesPartnershipOm JainNo ratings yet

- Admission of A Partner - 1Document2 pagesAdmission of A Partner - 1Tera baapNo ratings yet

- 12th Accounts Partnership Test 15 Sept.Document6 pages12th Accounts Partnership Test 15 Sept.SGEVirtualNo ratings yet

- Assessement Test - Retirment of A PartnerDocument2 pagesAssessement Test - Retirment of A PartnerShreya PushkarnaNo ratings yet

- Test Paper 12Document6 pagesTest Paper 12Sukhjinder SinghNo ratings yet

- New Model Test Paper 1Document8 pagesNew Model Test Paper 1Harry AryanNo ratings yet

- Additional Questions-5Document14 pagesAdditional Questions-5Shivam Kumar JhaNo ratings yet

- June 2019Document182 pagesJune 2019shankar k.c.No ratings yet

- RTP June 19 QnsDocument15 pagesRTP June 19 QnsbinuNo ratings yet

- Sample Question Paper IN AccountancyDocument7 pagesSample Question Paper IN AccountancyRahul TyagiNo ratings yet

- Retierment of PartnerDocument4 pagesRetierment of PartnerSaransh GhoshNo ratings yet

- Admission of A Partner - Work Sheet No .4Document12 pagesAdmission of A Partner - Work Sheet No .4Hamza MudassirNo ratings yet

- Retirement Hots and Application Based QuestionsDocument5 pagesRetirement Hots and Application Based Questionspriya longaniNo ratings yet

- Navya and Radhey Were Partners Sharing Profits and Losses in The RatioDocument9 pagesNavya and Radhey Were Partners Sharing Profits and Losses in The RatioMohammad Tariq AnsariNo ratings yet

- Practice Worksheet 2 For Admission: March 2018 Stood As Liabilities Amount Assets AmountDocument3 pagesPractice Worksheet 2 For Admission: March 2018 Stood As Liabilities Amount Assets AmountAaira IbrahimNo ratings yet

- 12 Accountancy Lyp 2015 Foreign Set1Document42 pages12 Accountancy Lyp 2015 Foreign Set1Ashish GangwalNo ratings yet

- FND Partnership QuestionDocument3 pagesFND Partnership QuestionShweta BhadauriaNo ratings yet

- 12 2006 Accountancy 2Document5 pages12 2006 Accountancy 2Akash TamuliNo ratings yet

- Advac SemifinalDocument8 pagesAdvac SemifinalDIVINE VILLENANo ratings yet

- Partnership FormationDocument2 pagesPartnership FormationMaria LopezNo ratings yet

- 12 2006 Accountancy 4Document5 pages12 2006 Accountancy 4Akash TamuliNo ratings yet

- Chapter-2: Partnership AccountsDocument6 pagesChapter-2: Partnership Accountsadityatiwari122006No ratings yet

- TtryuiopDocument6 pagesTtryuiopNAVEENNo ratings yet

- Partner Ship - IIDocument6 pagesPartner Ship - IIM JEEVARATHNAM NAIDUNo ratings yet

- PartnershipDocument10 pagesPartnershipShaz NagaNo ratings yet

- Accountancy TestDocument2 pagesAccountancy Testdixa mathpalNo ratings yet

- PT 06 (Partnership) (5 Dec)Document8 pagesPT 06 (Partnership) (5 Dec)Rajesh Kumar100% (2)

- Class Xii Time TableDocument1 pageClass Xii Time TableAditya srivastavaNo ratings yet

- Pa 1 Class Xii Business StudiesDocument2 pagesPa 1 Class Xii Business StudiesAditya srivastavaNo ratings yet

- Class Xii Time TableDocument1 pageClass Xii Time TableAditya srivastavaNo ratings yet

- TP 4 Pa 18 JuneDocument2 pagesTP 4 Pa 18 JuneAditya srivastavaNo ratings yet

- Aditya Birla Money SWOTDocument9 pagesAditya Birla Money SWOTGaurav SinghNo ratings yet

- Student NameDocument44 pagesStudent Name201930037No ratings yet

- Caf V TemplateDocument5 pagesCaf V Templatetatiana peacock100% (7)

- I Barnes - MIRF-withdrawalretreanchmentretDocument8 pagesI Barnes - MIRF-withdrawalretreanchmentretridbastraNo ratings yet

- Accounting For Government DisbursementsDocument12 pagesAccounting For Government DisbursementsMerlina Cuare100% (1)

- Sovereign Gold Bond - Product Features and FAQ'sDocument3 pagesSovereign Gold Bond - Product Features and FAQ'ssanjithchowdaryNo ratings yet

- Bank Branch Audit Presentation 2Document26 pagesBank Branch Audit Presentation 2karbalsNo ratings yet

- RBL Credit Card Statement - UnlockedDocument2 pagesRBL Credit Card Statement - UnlockedDipra DasNo ratings yet

- Books of Prime Entry and Control Account More Practice From A Level Topical Past PapersDocument21 pagesBooks of Prime Entry and Control Account More Practice From A Level Topical Past PapersJahanzaib ButtNo ratings yet

- Activity 9Document2 pagesActivity 9Kyle Marie PiñeroNo ratings yet

- Study On Call Money & Commercial Paper MarketDocument28 pagesStudy On Call Money & Commercial Paper MarketVarun Puri100% (2)

- Freddie MacDocument12 pagesFreddie Macانيس AnisNo ratings yet

- T Shape Account PreprationDocument5 pagesT Shape Account Preprationrajindere sainiNo ratings yet

- Sraj (Q4 - 2015)Document108 pagesSraj (Q4 - 2015)Wihelmina DeaNo ratings yet

- Financial Wellness Seminar: The Rock Unit Blue Horizon BranchDocument31 pagesFinancial Wellness Seminar: The Rock Unit Blue Horizon BranchKeiWakNo ratings yet

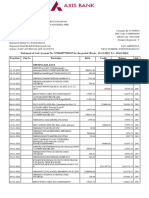

- Account STMT XX6767 20032024Document4 pagesAccount STMT XX6767 20032024jaidev DamarajuNo ratings yet

- Institute of Cost and Management Accountants of Pakistan Fall (Winter) 2010 ExaminationsDocument4 pagesInstitute of Cost and Management Accountants of Pakistan Fall (Winter) 2010 ExaminationsIrfanNo ratings yet

- Instructions: The Data Needed To Determine Year-End Adjustments Are As FollowsDocument2 pagesInstructions: The Data Needed To Determine Year-End Adjustments Are As FollowsyoantanNo ratings yet

- Secured Promissory Note: This Promissory Note Is Secured by Security Agreement of The Same DateDocument1 pageSecured Promissory Note: This Promissory Note Is Secured by Security Agreement of The Same DateFede CavalliNo ratings yet

- Contract Trade Usage: Cost-Plus or PercentageDocument4 pagesContract Trade Usage: Cost-Plus or Percentageraghav VarmaNo ratings yet

- FIN-AW3 AnswersDocument18 pagesFIN-AW3 AnswersRameesh DeNo ratings yet

- Finance Department PresentationDocument12 pagesFinance Department PresentationKMI7769% (13)

- The Unbanked and Underbanked by StateDocument11 pagesThe Unbanked and Underbanked by StatecaitlynharveyNo ratings yet

- Ratio Anlaysis Written ReportDocument5 pagesRatio Anlaysis Written ReportLyka Mae FajardoNo ratings yet

- Financial Management - Financial Statements, Cash Flow and TaxesDocument16 pagesFinancial Management - Financial Statements, Cash Flow and TaxesDonna ZanduetaNo ratings yet

- Project We LikeDocument45 pagesProject We LikeShashikant GujratiNo ratings yet