You might also like

- NCERT - Economic & Commercial Geography of India X (Old Edition)Document169 pagesNCERT - Economic & Commercial Geography of India X (Old Edition)Sumit SagarNo ratings yet

- How To Save Your TimeDocument1 pageHow To Save Your TimeSumit SagarNo ratings yet

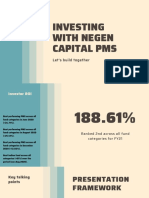

- INVESTING WITH NEGEN CAPITAL PMS: BEST PERFORMING FUND ACROSS CATEGORIESDocument12 pagesINVESTING WITH NEGEN CAPITAL PMS: BEST PERFORMING FUND ACROSS CATEGORIESSumit SagarNo ratings yet

- (Prelims Spotlight) Important Amendments in The Indian Constitution - CivilsdailyDocument10 pages(Prelims Spotlight) Important Amendments in The Indian Constitution - CivilsdailySumit SagarNo ratings yet

- Zac Efron Workout RoutineDocument9 pagesZac Efron Workout RoutineKhôi Nguyên100% (1)

- (NCERT) Principles of Geography XI (Old Edition) PDFDocument157 pages(NCERT) Principles of Geography XI (Old Edition) PDFPranshu SharmaNo ratings yet

- NCERT - Principle Basic of Geography XI (Old Edition)Document231 pagesNCERT - Principle Basic of Geography XI (Old Edition)Sumit SagarNo ratings yet

- Course Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallDocument3 pagesCourse Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallSumit SagarNo ratings yet

- AnnalPrg Exam RT 2022 Engl 130821Document1 pageAnnalPrg Exam RT 2022 Engl 130821Pruthaviraj BNo ratings yet

- Folding Faulting - NegiDocument31 pagesFolding Faulting - NegiSumit SagarNo ratings yet

- Negen Capital: (Portfolio Management Service)Document5 pagesNegen Capital: (Portfolio Management Service)Sumit SagarNo ratings yet

- Scanned With Camscanner: Kanishak Kataria: Air 1 Upsc Cse 2018Document3 pagesScanned With Camscanner: Kanishak Kataria: Air 1 Upsc Cse 2018Sumit SagarNo ratings yet

- BSK Ass 1Document8 pagesBSK Ass 1Sumit SagarNo ratings yet

- Underground: WaterDocument12 pagesUnderground: WaterSumit Sagar0% (1)

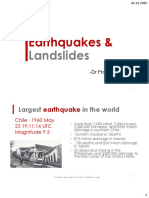

- Earthquakes and LandslidesDocument19 pagesEarthquakes and LandslidesSumit SagarNo ratings yet

- Rock mass classification and excavation guidelinesDocument6 pagesRock mass classification and excavation guidelinesSumit SagarNo ratings yet

- Law Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiesDocument2 pagesLaw Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiespratikNo ratings yet

- PT 365 Updation-2Document92 pagesPT 365 Updation-2ChaithanyaNo ratings yet

- Law Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiesDocument2 pagesLaw Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiespratikNo ratings yet

- Self Note - Historical Development of EducationDocument3 pagesSelf Note - Historical Development of EducationFINEworksNo ratings yet

- East Coast 2015 Letter Twin LightsDocument15 pagesEast Coast 2015 Letter Twin LightsSumit SagarNo ratings yet

- Master Document For FamilyDocument15 pagesMaster Document For FamilySumit SagarNo ratings yet

- NHRC CIC CVC CBI Lokpal: Home Ministry Responsible Only To ParliamentDocument4 pagesNHRC CIC CVC CBI Lokpal: Home Ministry Responsible Only To ParliamentpratikNo ratings yet

- Biodiversity Hotspots in IndiaDocument9 pagesBiodiversity Hotspots in IndiaSumit SagarNo ratings yet

- Architecture MCQ (Rohit Kumar Verma 170544)Document8 pagesArchitecture MCQ (Rohit Kumar Verma 170544)Sumit SagarNo ratings yet

- Parag Parikh Pole Star of Value InvestinDocument3 pagesParag Parikh Pole Star of Value InvestinSumit SagarNo ratings yet

- Cheetah: SR N O Name Picture Distributi ONDocument5 pagesCheetah: SR N O Name Picture Distributi ONSumit SagarNo ratings yet

- Hand and Seal: JSPSC-Statutory-Appoint: Prez - 62 Yrs - Report: GovernrDocument4 pagesHand and Seal: JSPSC-Statutory-Appoint: Prez - 62 Yrs - Report: Governrpratik100% (1)

- Architecture MCQsDocument8 pagesArchitecture MCQsSumit SagarNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Banking Courses in GujaratDocument2 pagesBanking Courses in GujaratSivaramakrishna SobhaNo ratings yet

- Literature Review Operations ManagementDocument4 pagesLiterature Review Operations Managementc5ry1f2g100% (1)

- SAMP CourseDocument4 pagesSAMP CourseJessieNo ratings yet

- Strategic Management and Strategic Competitiveness: Student VersionDocument16 pagesStrategic Management and Strategic Competitiveness: Student VersionCyrilraincreamNo ratings yet

- Business Process AnalysisDocument64 pagesBusiness Process AnalysisPanko MaalindogNo ratings yet

- The System Development Life CycleDocument3 pagesThe System Development Life CycleAfsana BashirNo ratings yet

- Comm1140 Week 2Document2 pagesComm1140 Week 2jenny kimNo ratings yet

- IAS 8 - How To Account For Artwork Under IFRSDocument5 pagesIAS 8 - How To Account For Artwork Under IFRSMuhammad Moin khanNo ratings yet

- International Financial Management 8th Edition Madura Test BankDocument40 pagesInternational Financial Management 8th Edition Madura Test Bankvioletciara4zr6100% (33)

- Accenture - Key Performance IndicatorsDocument169 pagesAccenture - Key Performance IndicatorsRajasekhar GotetiNo ratings yet

- SGS CBE Workplace Safety Risk Management A4 en 16 09 LRDocument8 pagesSGS CBE Workplace Safety Risk Management A4 en 16 09 LRnazirkuraNo ratings yet

- Agriculture Warehousing in IndiaDocument10 pagesAgriculture Warehousing in IndiaAmrit SharmaNo ratings yet

- Nykaa - Fundamental Technical AnalysisDocument6 pagesNykaa - Fundamental Technical Analysiskhyati kaulNo ratings yet

- PRTC 1stPB - 05.22 Sol AFARDocument4 pagesPRTC 1stPB - 05.22 Sol AFARCiatto SpotifyNo ratings yet

- EOS - Disney Pixar - Group 7Document9 pagesEOS - Disney Pixar - Group 7Amod VelingkarNo ratings yet

- Merchandising ProcessesDocument17 pagesMerchandising ProcessesvijayasethiiNo ratings yet

- Consumer Behavior - Week 3Document7 pagesConsumer Behavior - Week 3Jowjie TVNo ratings yet

- Boskalis Position Statement 01072022Document232 pagesBoskalis Position Statement 01072022citybizlist11No ratings yet

- Financial EngineeringDocument81 pagesFinancial Engineeringtannyjohny100% (2)

- Wica Guide 2020Document40 pagesWica Guide 2020Arthur LimNo ratings yet

- Test Bank For Marketing Defined Explained Applied 2nd Edition by LevensDocument27 pagesTest Bank For Marketing Defined Explained Applied 2nd Edition by Levensa6910172410% (1)

- Business Plan for Arooj Ice Cream ParlourDocument24 pagesBusiness Plan for Arooj Ice Cream ParlouronemanNo ratings yet

- Quiz 7Document1 pageQuiz 7vaniiqueNo ratings yet

- Manage production planning and scheduling with APS softwareDocument7 pagesManage production planning and scheduling with APS softwaresheebakbs5144100% (1)

- MpsDocument37 pagesMpsHari Krishnan RNo ratings yet

- Answers - SWOT Analysis in Action at SKODADocument7 pagesAnswers - SWOT Analysis in Action at SKODAMesay GulilatNo ratings yet

- Nielsen - Market Research For PanteneDocument21 pagesNielsen - Market Research For Panteneveerapratapreddy509No ratings yet

- BEST - Payroll HR Executive SummaryDocument7 pagesBEST - Payroll HR Executive SummarysimhengNo ratings yet

- NikeDocument27 pagesNikeKrishna KinkerNo ratings yet

- Va Study On Youtube As A Potential Tool For Marketing: Ms. Yogitha Sharma, Prof. Leena PhilipDocument12 pagesVa Study On Youtube As A Potential Tool For Marketing: Ms. Yogitha Sharma, Prof. Leena PhilipNaveen KNo ratings yet