You might also like

- 2.1 Assessment Test 2.2: Receivables Prelim Exam Intermediate AccountingDocument9 pages2.1 Assessment Test 2.2: Receivables Prelim Exam Intermediate AccountingWinoah HubaldeNo ratings yet

- MODULE 5 To Module 6Document10 pagesMODULE 5 To Module 6Winoah HubaldeNo ratings yet

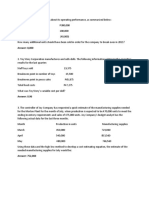

- Answer: 215,000Document2 pagesAnswer: 215,000Winoah HubaldeNo ratings yet

- Strategic Cost Management Is The Process of Reducing Total Costs While Improving The Strategic PositionDocument9 pagesStrategic Cost Management Is The Process of Reducing Total Costs While Improving The Strategic PositionWinoah HubaldeNo ratings yet

- Break-Even Is The Point Where Total Sales Equal To Total CostsDocument5 pagesBreak-Even Is The Point Where Total Sales Equal To Total CostsWinoah HubaldeNo ratings yet

- Answer: 8,000Document2 pagesAnswer: 8,000Winoah HubaldeNo ratings yet

- FinalsDocument3 pagesFinalsWinoah HubaldeNo ratings yet

- Assignment 1: Variable CostingDocument4 pagesAssignment 1: Variable CostingWinoah HubaldeNo ratings yet

- Quiz 6.1 Capital BudgetingDocument1 pageQuiz 6.1 Capital BudgetingWinoah HubaldeNo ratings yet

- Segment MarginDocument1 pageSegment MarginWinoah HubaldeNo ratings yet

- Lesson 1Document30 pagesLesson 1Winoah HubaldeNo ratings yet

- HW5 1Document4 pagesHW5 1Winoah HubaldeNo ratings yet

- Data of Barbados Company:: Variable Cost Per UnitDocument2 pagesData of Barbados Company:: Variable Cost Per UnitWinoah HubaldeNo ratings yet

- Assignment 1: Variable CostingDocument4 pagesAssignment 1: Variable CostingWinoah HubaldeNo ratings yet

- Lesson 2Document10 pagesLesson 2Winoah HubaldeNo ratings yet

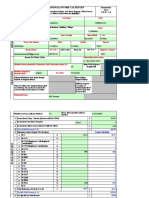

- Module 3: Completing The Accounting Cycles of A Service Business 3.1 Worksheet and The Financial StatementsDocument10 pagesModule 3: Completing The Accounting Cycles of A Service Business 3.1 Worksheet and The Financial StatementsWinoah HubaldeNo ratings yet

- Assignment 1: Variable CostingDocument4 pagesAssignment 1: Variable CostingWinoah HubaldeNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 2015 Itr1 PR9Document9 pages2015 Itr1 PR9Soumyaranjan SwainNo ratings yet

- Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageCertificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)fernandoNo ratings yet

- OKDHSBenefitsRequestedReportTimothy LaCroixDocument6 pagesOKDHSBenefitsRequestedReportTimothy LaCroixTimothy A. LaCroixNo ratings yet

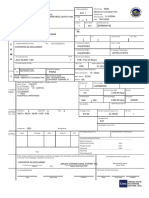

- TAX Invoice: Order DetailsDocument1 pageTAX Invoice: Order DetailsAtulSanapNo ratings yet

- Equity Delighteth in EqualityDocument5 pagesEquity Delighteth in Equalitysyed jaffar aliNo ratings yet

- 3rd Sem Taxation Ppt-3.Pdf328Document34 pages3rd Sem Taxation Ppt-3.Pdf328Harpreet SinghNo ratings yet

- GST Tax Invoice Format For GoodsDocument3 pagesGST Tax Invoice Format For GoodsYaser Ali TariqNo ratings yet

- ExportDecDoc E6RB000010EDocument2 pagesExportDecDoc E6RB000010ENaj MusorNo ratings yet

- Tanzania Revenue Authority Institute of Tax Administration: Tax Compliance and Customer Care PGDT EDocument33 pagesTanzania Revenue Authority Institute of Tax Administration: Tax Compliance and Customer Care PGDT EPostgraduate 2020ReNo ratings yet

- Royalty FTS by CA. Sudin Sabnis 1Document64 pagesRoyalty FTS by CA. Sudin Sabnis 1Bhagyashree JainNo ratings yet

- IRPF 2022 2021 Origi Imagem Declaracao01Document1 pageIRPF 2022 2021 Origi Imagem Declaracao01BVC RoleplayNo ratings yet

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruAadityaa PawarNo ratings yet

- RMC 124-2020Document19 pagesRMC 124-2020Glenn Sabanal GarciaNo ratings yet

- Form 1099GDocument2 pagesForm 1099GMarcus KreseNo ratings yet

- Panama Papers: Dirty Money and Tax Tricks: How The Rich, The Powerful and Criminals Rip Us Off!Document40 pagesPanama Papers: Dirty Money and Tax Tricks: How The Rich, The Powerful and Criminals Rip Us Off!Vishwajit PatilNo ratings yet

- 6 - GR No.201398-99-CIR V AvonDocument2 pages6 - GR No.201398-99-CIR V AvonPamela Jane I. TornoNo ratings yet

- "E-Banking in India": Project Report ONDocument27 pages"E-Banking in India": Project Report ONBiplab SwainNo ratings yet

- Manila Electric Company v. Province of LagunaDocument1 pageManila Electric Company v. Province of LagunaRukmini Dasi Rosemary GuevaraNo ratings yet

- MCQ Public FinanceDocument4 pagesMCQ Public FinanceWild Gaming YT100% (2)

- Receipt BookingDocument1 pageReceipt BookingFR ChannelNo ratings yet

- Clubbing of IncomeDocument1 pageClubbing of IncomeHanuman MeenaNo ratings yet

- Principles of Taxation Part 1Document68 pagesPrinciples of Taxation Part 1not funny didn't laughNo ratings yet

- IRS Notice 1446Document1 pageIRS Notice 1446Courier JournalNo ratings yet

- Garcia Arby Jay D. Ba 223-Income Taxation Midterm ExaminationDocument4 pagesGarcia Arby Jay D. Ba 223-Income Taxation Midterm ExaminationfssdsddsfdsfsdNo ratings yet

- Structural Functional Analysis of Ra 10963Document2 pagesStructural Functional Analysis of Ra 10963Shaina NavaNo ratings yet

- Amadeus Automated Refund StepsDocument3 pagesAmadeus Automated Refund StepsRana JeeNo ratings yet

- Chio, Rahma S. - Tax Ii AssignmentDocument4 pagesChio, Rahma S. - Tax Ii AssignmentPIKACHUCHIENo ratings yet

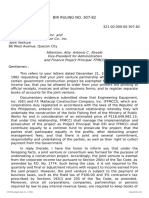

- BIR Ruling No. 307-82Document2 pagesBIR Ruling No. 307-82Alfred Hernandez CampañanoNo ratings yet

- Church Financial Report-2Document8 pagesChurch Financial Report-2Grace ChandaNo ratings yet

- Salary Deduction Certificate Us 149 FormatDocument1 pageSalary Deduction Certificate Us 149 FormatAbdul Qadir Inventory ContollerNo ratings yet