You might also like

- Bureau of Internal Revenue: Republic of The Philippines Department of FinanceDocument7 pagesBureau of Internal Revenue: Republic of The Philippines Department of FinancejoanneNo ratings yet

- RMO - No. 33-2019 PDFDocument7 pagesRMO - No. 33-2019 PDFRedbutterfly Del Mundo GalindoNo ratings yet

- Bureau of Internal Revenue Quezon CityDocument6 pagesBureau of Internal Revenue Quezon CityPeggy SalazarNo ratings yet

- Accounting of Income Tax Collection PerspectiveDocument12 pagesAccounting of Income Tax Collection PerspectiveadilshahkazmiNo ratings yet

- Rmo No 9-06 TCVD Tax MappingDocument16 pagesRmo No 9-06 TCVD Tax MappingGil PinoNo ratings yet

- Collection of Direct Taxes - OLTASDocument36 pagesCollection of Direct Taxes - OLTASnalluriimpNo ratings yet

- Rmo 13-2006Document3 pagesRmo 13-2006Ellen Grace LongosNo ratings yet

- Bureau of Internal RevenueDocument13 pagesBureau of Internal Revenuenathalie velasquezNo ratings yet

- RMO No. 25-2019Document7 pagesRMO No. 25-2019Jhenny Ann P. SalemNo ratings yet

- RR 16-02Document2 pagesRR 16-02saintkarriNo ratings yet

- Bureau of Internal RevenueDocument8 pagesBureau of Internal RevenueDianne EvardoneNo ratings yet

- 34036rmo 2-2007Document13 pages34036rmo 2-2007toniNo ratings yet

- Securities and Exchange Commission: Published: Manila Bulletin, January 22, 2019Document3 pagesSecurities and Exchange Commission: Published: Manila Bulletin, January 22, 20199einsNo ratings yet

- Rmo 1985Document58 pagesRmo 1985Mary graceNo ratings yet

- Municipal Financials and Audit Report SummaryDocument5 pagesMunicipal Financials and Audit Report SummaryThe ApprenticeNo ratings yet

- 48451rmc No. 1-2010Document3 pages48451rmc No. 1-2010Maureen PascualNo ratings yet

- RMO 11-2005 (Corrected Version)Document12 pagesRMO 11-2005 (Corrected Version)simey_kizhie07No ratings yet

- Rmo 32-05Document8 pagesRmo 32-05nathalie velasquezNo ratings yet

- Revenue Regulations No. 9-2001Document6 pagesRevenue Regulations No. 9-2001Anonymous GMUQYq8No ratings yet

- Master Circular 19.01.2022-Recovery of ArrearsDocument16 pagesMaster Circular 19.01.2022-Recovery of ArrearsShiv Swarup PandeyNo ratings yet

- San Miguel Executive Summary 2011Document12 pagesSan Miguel Executive Summary 2011Justine CastilloNo ratings yet

- Tax Summary of LawsDocument6 pagesTax Summary of LawsKatherine GutierrezNo ratings yet

- Rmo 40-2004Document21 pagesRmo 40-2004simey_kizhie07No ratings yet

- Bank Bulletin No. 2022-06 - Reiteration of Relevant Policies in The Acceptance of 2021 Annual Income Tax Return and PaymentDocument3 pagesBank Bulletin No. 2022-06 - Reiteration of Relevant Policies in The Acceptance of 2021 Annual Income Tax Return and PaymentRen Mar CruzNo ratings yet

- Rmo 28-07Document31 pagesRmo 28-07nathalie velasquezNo ratings yet

- Assignment Account ProcedureDocument24 pagesAssignment Account ProcedureAshraf Ali0% (1)

- BIR Revenue Memorandum Order 15-2003Document21 pagesBIR Revenue Memorandum Order 15-2003Yunit M StarirayNo ratings yet

- Bureau of Internal RevenueDocument5 pagesBureau of Internal RevenuegelskNo ratings yet

- Bureau of Internal Revenue: Republic of The Philippines Department of FinanceDocument4 pagesBureau of Internal Revenue: Republic of The Philippines Department of FinanceHanabishi RekkaNo ratings yet

- 01-LBP2016 Transmittal LettersDocument6 pages01-LBP2016 Transmittal LettersADRIAN 18No ratings yet

- Administrative Guidelines On The Waiver of Penalty and Interest UPDATEDDocument8 pagesAdministrative Guidelines On The Waiver of Penalty and Interest UPDATEDKomla Atsu TachieNo ratings yet

- UntitledDocument8 pagesUntitledSta Maria JamesNo ratings yet

- Santa Maria Executive Summary 2016Document10 pagesSanta Maria Executive Summary 2016Brene Joseph LuzNo ratings yet

- Nbi ML2014Document31 pagesNbi ML2014Early RoseNo ratings yet

- Concurrent Audit References 28-12-2012Document12 pagesConcurrent Audit References 28-12-2012Sj RaoNo ratings yet

- Guidelines For TDS On GSTDocument5 pagesGuidelines For TDS On GSTPWD HIGHWAYNo ratings yet

- 2009 RMC 23-2009 LOA RevalidationDocument2 pages2009 RMC 23-2009 LOA Revalidationedong the greatNo ratings yet

- Maigo Executive Summary 2021Document8 pagesMaigo Executive Summary 2021Rowena MahusayNo ratings yet

- Streamline TCC Cash ConversionDocument8 pagesStreamline TCC Cash ConversionjohnnayelNo ratings yet

- Memo No 1304Document8 pagesMemo No 1304chandra shekharNo ratings yet

- Taxation Law SummerDocument6 pagesTaxation Law SummerAnita Solano BoholNo ratings yet

- Business and Transfer Tax GuideDocument6 pagesBusiness and Transfer Tax Guideman ibeNo ratings yet

- BIR issues guidelines for modified tax compliance driveDocument3 pagesBIR issues guidelines for modified tax compliance driveReymund S BumanglagNo ratings yet

- Guidelines and Conduct of TCVD RMO09-2006Document45 pagesGuidelines and Conduct of TCVD RMO09-2006Kris CalabiaNo ratings yet

- Revised Uniform Guidelines for Revenue Collection OfficersDocument4 pagesRevised Uniform Guidelines for Revenue Collection OfficersJamie LynNo ratings yet

- Joint guidelines on tax remittanceDocument7 pagesJoint guidelines on tax remittancefred_barillo09No ratings yet

- Taxation (NIRC Sec 1-36Document11 pagesTaxation (NIRC Sec 1-36Angie Louh S. DiosoNo ratings yet

- Rmo No. 22 2016 PDFDocument6 pagesRmo No. 22 2016 PDFjtf1898No ratings yet

- ONETT - RMO 15-2003 - Policies&GuidelinesDocument19 pagesONETT - RMO 15-2003 - Policies&GuidelineszneraNo ratings yet

- GST Circular PDFDocument11 pagesGST Circular PDFNavnera divisionNo ratings yet

- Settlement of Accounts GuideDocument155 pagesSettlement of Accounts GuideRonnie Balleras Pagal100% (1)

- Improper Handling of Collections: Observations and RecommendationsDocument22 pagesImproper Handling of Collections: Observations and Recommendationsdemos reaNo ratings yet

- RMC No. 42-03 - Rules On Assessment of National INternal Revenue Taxes Covered by A LN Under The Relief System PDFDocument12 pagesRMC No. 42-03 - Rules On Assessment of National INternal Revenue Taxes Covered by A LN Under The Relief System PDFCkey ArNo ratings yet

- COA Presentation - RRSADocument155 pagesCOA Presentation - RRSAKristina Dacayo-Garcia100% (1)

- CH 1 and 2 (Paz, Ace)Document3 pagesCH 1 and 2 (Paz, Ace)Ace PazNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- 35060ops Manual FinalDocument153 pages35060ops Manual FinaltoniNo ratings yet

- Revenue Memorandum Order No. 7-2007: CY 2007 Goals (In Millions) Tax Classification TotalDocument7 pagesRevenue Memorandum Order No. 7-2007: CY 2007 Goals (In Millions) Tax Classification TotaltoniNo ratings yet

- Bureau of Internal Revenue: Republic of The Philippines Department of FinanceDocument5 pagesBureau of Internal Revenue: Republic of The Philippines Department of FinancetoniNo ratings yet

- 35060rmo 8-2007Document2 pages35060rmo 8-2007toniNo ratings yet

- Pre-Planning Workshop: Check No. Date AmountDocument2 pagesPre-Planning Workshop: Check No. Date AmounttoniNo ratings yet

- RMO 5-2007 Verification of 2005 Tax ReturnsDocument3 pagesRMO 5-2007 Verification of 2005 Tax ReturnstoniNo ratings yet

- 34036rmo 2-2007Document13 pages34036rmo 2-2007toniNo ratings yet

- RR No. 9-2021Document3 pagesRR No. 9-2021Theodore BallesterosNo ratings yet

- RMC No. 102-2020 Annex ADocument2 pagesRMC No. 102-2020 Annex AHerzl Hali V. HermosaNo ratings yet

- RMC No 31-2019 Candidates PDFDocument3 pagesRMC No 31-2019 Candidates PDFFrancis Nico PeñaNo ratings yet

- FF.L Q: Rever/Ue Memorandum CrrcrrlarDocument1 pageFF.L Q: Rever/Ue Memorandum CrrcrrlarMirabel VidalNo ratings yet

- rr98 01Document1 pagerr98 01toniNo ratings yet

- Kawanihan NG Rentas Internas: Republika NG Pilipinas Kagawarang NG PananalapiDocument2 pagesKawanihan NG Rentas Internas: Republika NG Pilipinas Kagawarang NG PananalapitoniNo ratings yet

- Alcantara Vs RepublicDocument25 pagesAlcantara Vs RepublictoniNo ratings yet

- De Lima Vs City of ManilaDocument43 pagesDe Lima Vs City of Manilatoni0% (1)

- City of Cagayan Vs CEPALCODocument36 pagesCity of Cagayan Vs CEPALCOtoniNo ratings yet

- RR No. 22-2020 PDFDocument2 pagesRR No. 22-2020 PDFSandyNo ratings yet

- Farmer Beneficiaries in Jalajala, Rizal vs. Heirs of Juliana Maronilla (2019)Document13 pagesFarmer Beneficiaries in Jalajala, Rizal vs. Heirs of Juliana Maronilla (2019)toniNo ratings yet

- RMC No 31-2019 Candidates PDFDocument3 pagesRMC No 31-2019 Candidates PDFFrancis Nico PeñaNo ratings yet

- Cta 2D CV 09179 M 2018oct04 AssDocument4 pagesCta 2D CV 09179 M 2018oct04 AsstoniNo ratings yet

- FF.L Q: Rever/Ue Memorandum CrrcrrlarDocument1 pageFF.L Q: Rever/Ue Memorandum CrrcrrlarMirabel VidalNo ratings yet

- Assignment Model Typical QuestionDocument17 pagesAssignment Model Typical Questionjagritiprakash00100No ratings yet

- Accounts PaperDocument2 pagesAccounts PaperRohan Ghadge-46No ratings yet

- Vinamilk Yogurt Report 2019: CTCP Sữa Việt Nam (Vinamilk)Document24 pagesVinamilk Yogurt Report 2019: CTCP Sữa Việt Nam (Vinamilk)Nguyễn Hoàng TrườngNo ratings yet

- Carbon Market Year in Review 2020Document26 pagesCarbon Market Year in Review 2020Sayaka TsugaiNo ratings yet

- One of Your Responsibilities As Division Manager of An ImportantDocument1 pageOne of Your Responsibilities As Division Manager of An ImportantAmit PandeyNo ratings yet

- Att-2.1 SowDocument5 pagesAtt-2.1 SowAgung FitrillaNo ratings yet

- M&ADocument27 pagesM&ArinacharNo ratings yet

- Module 3 Consumer Strategies GuideDocument19 pagesModule 3 Consumer Strategies GuideJoana Marie CabuteNo ratings yet

- P7112bgm-Catalogueb2010 0811 en A4 FullDocument810 pagesP7112bgm-Catalogueb2010 0811 en A4 FullShri ShriNo ratings yet

- Marketing Plan Guidelines:: Bus314 Marketing Management (Ncy)Document2 pagesMarketing Plan Guidelines:: Bus314 Marketing Management (Ncy)Murgi kun :3No ratings yet

- GUCCI - Case Only110910Document39 pagesGUCCI - Case Only110910sabastien_10dec5663No ratings yet

- reading_sample_sap_press_reporting_with_sap_s4hanaDocument32 pagesreading_sample_sap_press_reporting_with_sap_s4hanaCharles SantosNo ratings yet

- Eks 9 en 2015 01 14Document157 pagesEks 9 en 2015 01 14aykutNo ratings yet

- Business 5511 Group Project 0007ADocument15 pagesBusiness 5511 Group Project 0007ALinh NguyenNo ratings yet

- Building Contruction Workers Regulation of Employment and Working Conditions Act 1996Document14 pagesBuilding Contruction Workers Regulation of Employment and Working Conditions Act 1996omarmhusainNo ratings yet

- 7 Eleven Store Nantun District - Google SearchDocument1 page7 Eleven Store Nantun District - Google SearchArleen MallillinNo ratings yet

- Rajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Document1 pageRajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Bhavy Kumar JainNo ratings yet

- TCA PresentationDocument24 pagesTCA PresentationPrathap GNo ratings yet

- Technical Letter StructureDocument33 pagesTechnical Letter Structuresayed Tamir janNo ratings yet

- Becoming an Operations Consultant in 40 StepsDocument2 pagesBecoming an Operations Consultant in 40 StepsNicolae NistorNo ratings yet

- The Prevention of Corruption Act, 1988: A Critical StudyDocument33 pagesThe Prevention of Corruption Act, 1988: A Critical StudyRAJARAJESHWARI M GNo ratings yet

- TS16949 Training OverviewDocument23 pagesTS16949 Training OverviewPraveen CoolNo ratings yet

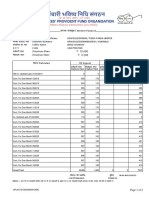

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Res. MethodDocument100 pagesRes. Methodhimanshug_43No ratings yet

- Free GameDocument1 pageFree GameSC AyuburiNo ratings yet

- CV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Document11 pagesCV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Agus NugrahaNo ratings yet

- Your Results For "Quick Quiz (Open Access) "Document2 pagesYour Results For "Quick Quiz (Open Access) "Manuel CornejoNo ratings yet

- Grameen BankDocument28 pagesGrameen Bankalpha34567No ratings yet

- Max AR Final 130812 PDFDocument731 pagesMax AR Final 130812 PDFsnjv2621No ratings yet

- Explore and Explain:: Grade 12 - EntrepreneurshipDocument12 pagesExplore and Explain:: Grade 12 - EntrepreneurshipLatifah EmamNo ratings yet