You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 1st Exam Chapter 11Document9 pages1st Exam Chapter 11Imma Therese YuNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Writing a Thesis ProposalDocument39 pagesWriting a Thesis ProposalImma Therese YuNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

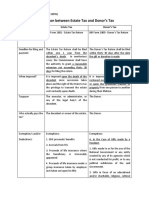

- Comparison Between Estate Tax and Donor's TaxDocument5 pagesComparison Between Estate Tax and Donor's TaxImma Therese YuNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Business and Transfer Taxation Chapter 13 Discussion Questions and AnswerDocument2 pagesBusiness and Transfer Taxation Chapter 13 Discussion Questions and AnswerKarla Faye LagangNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Business and Transfer Taxation Chapter 13 Discussion Questions and AnswerDocument2 pagesBusiness and Transfer Taxation Chapter 13 Discussion Questions and AnswerKarla Faye LagangNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Comparison Between Estate Tax and Donor's TaxDocument5 pagesComparison Between Estate Tax and Donor's TaxImma Therese YuNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- NotesDocument15 pagesNotesImma Therese YuNo ratings yet

- Banggawan Answer KeyDocument17 pagesBanggawan Answer Keyvallerie_lumantas76% (42)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Writing a Thesis ProposalDocument39 pagesWriting a Thesis ProposalImma Therese YuNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Intro To FMDocument4 pagesIntro To FMImma Therese YuNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Chapter 27Document8 pagesChapter 27Imma Therese YuNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Chapter 25: Borrowing Costs Borrowing CostDocument3 pagesChapter 25: Borrowing Costs Borrowing CostImma Therese YuNo ratings yet

- Contemporary Arts of The PhilippinesDocument5 pagesContemporary Arts of The PhilippinesImma Therese YuNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Definition: Assistance by Governemnt in The Form of TransferDocument4 pagesDefinition: Assistance by Governemnt in The Form of TransferImma Therese YuNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Fundamentals of AccountingDocument3 pagesFundamentals of AccountingImma Therese YuNo ratings yet

- Taxable Income and Income Tax - Foreign Tax Credit - AdministrDocument52 pagesTaxable Income and Income Tax - Foreign Tax Credit - AdministrCharlotte MalgapoNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Principle of Taxation LawDocument3 pagesPrinciple of Taxation LawTaraChandraChouhanNo ratings yet

- A Project Report On GSTDocument15 pagesA Project Report On GSTAnjali RatudiNo ratings yet

- RQ2019A14 - Online Assignment 1 - BSL301 - ROSHANDocument6 pagesRQ2019A14 - Online Assignment 1 - BSL301 - ROSHANroshan satpathyNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Form No. 12B: Prabhakarappa ShashidharDocument1 pageForm No. 12B: Prabhakarappa ShashidharAmbika BpNo ratings yet

- Qatar Tax Law 2009Document18 pagesQatar Tax Law 2009Jitendra NagvekarNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- April Sathish Pay SlipDocument1 pageApril Sathish Pay Slipmsathish7428No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Afroza Sultana RumaDocument1 pageAfroza Sultana RumaImam HasanNo ratings yet

- FD 941 Apr-Jun 2017 PDFDocument3 pagesFD 941 Apr-Jun 2017 PDFScott WinklerNo ratings yet

- Homework - Income TaxesDocument3 pagesHomework - Income TaxesPeachyNo ratings yet

- Banking Industry Risk ProfilingDocument34 pagesBanking Industry Risk ProfilingGopal SharmaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Tax Notes Section 28Document3 pagesTax Notes Section 28Jacqueline LeonciaNo ratings yet

- Chi MangaDocument3 pagesChi MangaHAbbunoNo ratings yet

- Theory and Basis of TaxationDocument1 pageTheory and Basis of TaxationLaica MontefalcoNo ratings yet

- DTC Bill proposes modest changes to tax slabs and ratesDocument5 pagesDTC Bill proposes modest changes to tax slabs and ratesSumit DaraNo ratings yet

- ECONOMIC BENEFIT THEORY - BIR Ruling No. 123-97 (Retirement and Separation Benefits Paid To Employees)Document2 pagesECONOMIC BENEFIT THEORY - BIR Ruling No. 123-97 (Retirement and Separation Benefits Paid To Employees)KriszanFrancoManiponNo ratings yet

- Creba Vs Romulo TaxDocument3 pagesCreba Vs Romulo TaxNichole LanuzaNo ratings yet

- Basic Financial Management Booklet For Elementary Community Primary SchoolsDocument42 pagesBasic Financial Management Booklet For Elementary Community Primary SchoolsFrance Bejosa100% (1)

- CPA UGANDA PAPER 11 TAXATION November 20Document4 pagesCPA UGANDA PAPER 11 TAXATION November 20agaba fredNo ratings yet

- Input VAT DeductionsDocument2 pagesInput VAT DeductionsKim Cristian MaañoNo ratings yet

- Payslip Apr2020Document1 pagePayslip Apr2020Pinki Mitra DasNo ratings yet

- Job Work Challan: Aadinath Industries (111341) C-11/2, Wazirpur Industrial Area Delhi DL - Delhi 110052Document1 pageJob Work Challan: Aadinath Industries (111341) C-11/2, Wazirpur Industrial Area Delhi DL - Delhi 110052Anshu SinghNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Pay SlipDocument1 pagePay SlipnauvalNo ratings yet

- ACCT 553 Week 7 HW SolutionDocument3 pagesACCT 553 Week 7 HW SolutionMohammad Islam100% (1)

- Cash Budget - Payal Plastics CompanyDocument4 pagesCash Budget - Payal Plastics Companysukesh80% (5)

- Rajkot Airport E and M AMC 1st RADocument2 pagesRajkot Airport E and M AMC 1st RANanu PatelNo ratings yet

- Withholding-Taxes (ZRA)Document2 pagesWithholding-Taxes (ZRA)Noah MwansaNo ratings yet

- CP71ADocument6 pagesCP71AFunny ChunksNo ratings yet

- E-WAY BILL DetailsDocument1 pageE-WAY BILL DetailsrohanNo ratings yet

- How Much Is The Distributable Income of The GPP?Document2 pagesHow Much Is The Distributable Income of The GPP?Katrina Dela CruzNo ratings yet