You might also like

- CH 8 ExerciseshDocument14 pagesCH 8 Exercisesh김가온No ratings yet

- RF Ltd Cash BudgetDocument26 pagesRF Ltd Cash BudgetRiaz Baloch Notezai100% (1)

- Cash BudgetingDocument3 pagesCash BudgetingAngel Kitty Labor67% (3)

- Cash Sales Credit Sales: ACCT201B Practice Questions Chapter 8Document9 pagesCash Sales Credit Sales: ACCT201B Practice Questions Chapter 8GuinevereNo ratings yet

- Cash Budgeting QuestionsDocument5 pagesCash Budgeting QuestionsAnissa GeddesNo ratings yet

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocument9 pagesExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNo ratings yet

- Master Budget With SolutionsDocument12 pagesMaster Budget With SolutionsDea Andal100% (4)

- Solution and AnswerDocument4 pagesSolution and AnswerMicaela EncinasNo ratings yet

- Mozammil 029Document4 pagesMozammil 029Iqbal Shan LifestyleNo ratings yet

- ACCT 10001: Accounting Reports & Analysis – Lecture 9 Budgeting & Variance ReportDocument4 pagesACCT 10001: Accounting Reports & Analysis – Lecture 9 Budgeting & Variance ReportBáchHợpNo ratings yet

- AFDM - Assign 4Document1 pageAFDM - Assign 4Tausif IlyasNo ratings yet

- Exercises Budgeting ACCT2105 3s2010Document7 pagesExercises Budgeting ACCT2105 3s2010Hanh Bui0% (1)

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- Assignment 9 MADocument9 pagesAssignment 9 MAHassam SiddiqiNo ratings yet

- Assignment 5Document2 pagesAssignment 5NABILAH KHANSA 1911000089No ratings yet

- Hillyard CompanyDocument3 pagesHillyard CompanyJea BalagtasNo ratings yet

- Budgeting - ExamplesDocument2 pagesBudgeting - Examplessunil.ctNo ratings yet

- Question Compilation - 230316 - 072454Document9 pagesQuestion Compilation - 230316 - 072454Ranjan DhakalNo ratings yet

- CH 9 PDFDocument35 pagesCH 9 PDFhmmmNo ratings yet

- SophisticatesDocument3 pagesSophisticatesLuis Melquiades P. GarciaNo ratings yet

- Fin Activity For Sales Budget EtcDocument3 pagesFin Activity For Sales Budget EtcMariz TimarioNo ratings yet

- Functions of Each BudgetDocument23 pagesFunctions of Each BudgetNguyen Dac ThichNo ratings yet

- Financial PlanningDocument6 pagesFinancial Planningakimasa raizeNo ratings yet

- Chapter 4 Best Master Budget IllustrationDocument23 pagesChapter 4 Best Master Budget IllustrationLeykun GizealemNo ratings yet

- Problem 8.17: Cash Budget For The Month of December 1. Ashton CompanyDocument3 pagesProblem 8.17: Cash Budget For The Month of December 1. Ashton CompanyAbdul MoeezNo ratings yet

- Taller de Ejercicios de PresupuestosDocument11 pagesTaller de Ejercicios de PresupuestosalexNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Isfi Nuraida - Anggaran KasDocument86 pagesIsfi Nuraida - Anggaran KasGhinaNo ratings yet

- Cash Accrual Practice SetDocument2 pagesCash Accrual Practice SetMa. Trixcy De VeraNo ratings yet

- Budget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Document7 pagesBudget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Suraj KumarNo ratings yet

- Quiz #2 - CH 4 & 5: Question 1 (48 Marks)Document2 pagesQuiz #2 - CH 4 & 5: Question 1 (48 Marks)JamNo ratings yet

- Cost Accounting Assignment #2Document5 pagesCost Accounting Assignment #2BRIANNIE ASRI VIVASNo ratings yet

- Multiple Choice: Select The Best Answer From The Given Choices and Write It Down On Your Answer SheetDocument14 pagesMultiple Choice: Select The Best Answer From The Given Choices and Write It Down On Your Answer Sheetmimi supasNo ratings yet

- TugasDocument3 pagesTugasLina EkaNo ratings yet

- Ejercicios ProformaDocument3 pagesEjercicios ProformaSaira veru bernalNo ratings yet

- Cash Management-ProblemsDocument2 pagesCash Management-ProblemsNagma ParmarNo ratings yet

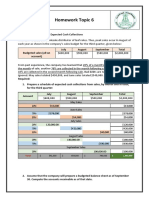

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Obien, Francine Denise Eleanor G. Abm 12 Y1-7Document2 pagesObien, Francine Denise Eleanor G. Abm 12 Y1-7Emar Kim0% (1)

- Bud GettingDocument8 pagesBud GettingLorena Mae LasquiteNo ratings yet

- Questions On Cash Budget-2Document7 pagesQuestions On Cash Budget-2Mpolokeng HlabanaNo ratings yet

- HL Business Management 12 Exam 4Document6 pagesHL Business Management 12 Exam 4Micah M100% (1)

- Pre Finals Manacc 1Document8 pagesPre Finals Manacc 1Gesselle Acebedo0% (1)

- Foundations of Financial Management: Spreadsheet TemplatesDocument9 pagesFoundations of Financial Management: Spreadsheet Templatesalaa_h1100% (1)

- Ejercicios ContabilidadDocument3 pagesEjercicios ContabilidadCarolina RvNo ratings yet

- HASF Hardware Store 2011 budget schedules and financial forecastsDocument2 pagesHASF Hardware Store 2011 budget schedules and financial forecastsHaris HasanNo ratings yet

- Working 4Document8 pagesWorking 4Hà Lê DuyNo ratings yet

- Extra Questions - A LevelDocument8 pagesExtra Questions - A LevelMUSTHARI KHANNo ratings yet

- Accounts Receivable CalculationDocument5 pagesAccounts Receivable CalculationCarmina SanchezNo ratings yet

- BudgetingDocument74 pagesBudgetingRevathi AnandNo ratings yet

- Cash Budget AnalysisDocument23 pagesCash Budget Analysisarjun sachdevNo ratings yet

- CMA Exam Principles of AccountingDocument4 pagesCMA Exam Principles of AccountingMohammad ShahidNo ratings yet

- BASTRCSX-Learning-Activity-5_with-answersDocument10 pagesBASTRCSX-Learning-Activity-5_with-answersChel EscuetaNo ratings yet

- Exercises 4 Financial Planning BudgetingDocument2 pagesExercises 4 Financial Planning BudgetingKyle PereiraNo ratings yet

- Acct 2020 Excel Budget ProblemDocument6 pagesAcct 2020 Excel Budget Problemapi-307661249No ratings yet

- Unit 3 - Business Finance - AppendixDocument5 pagesUnit 3 - Business Finance - Appendixmhmir9.95No ratings yet

- Required: Using The Data Above, Complete The Following Statements and Schedules For The First QuarterDocument6 pagesRequired: Using The Data Above, Complete The Following Statements and Schedules For The First QuarterteferiNo ratings yet

- ACCT1003 - Worksheet - 8 - Summer 2016Document5 pagesACCT1003 - Worksheet - 8 - Summer 2016sandrae brownNo ratings yet

- 2021-22 F5 BAFS Mid-Year Exam (Question)Document7 pages2021-22 F5 BAFS Mid-Year Exam (Question)Anna TungNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Components of GDP over time in IndiaDocument14 pagesComponents of GDP over time in IndiaAkankshaNo ratings yet

- Answer:: Be Present. It's Crucial To Clear Out The Mental Fog Before Going On Stage, One Way Is To Talk ToDocument2 pagesAnswer:: Be Present. It's Crucial To Clear Out The Mental Fog Before Going On Stage, One Way Is To Talk ToAkankshaNo ratings yet

- Scarcity AkDocument3 pagesScarcity AkAkankshaNo ratings yet

- GDP Growth Rate Over The YearsDocument3 pagesGDP Growth Rate Over The YearsAkankshaNo ratings yet

- SpeechDocument2 pagesSpeechAkankshaNo ratings yet

- Answer:: Be Present. It's Crucial To Clear Out The Mental Fog Before Going On Stage, One Way Is To Talk ToDocument2 pagesAnswer:: Be Present. It's Crucial To Clear Out The Mental Fog Before Going On Stage, One Way Is To Talk ToAkankshaNo ratings yet

- Answer:: Be Present. It's Crucial To Clear Out The Mental Fog Before Going On Stage, One Way Is To Talk ToDocument2 pagesAnswer:: Be Present. It's Crucial To Clear Out The Mental Fog Before Going On Stage, One Way Is To Talk ToAkankshaNo ratings yet

- Emailing ListDocument388 pagesEmailing ListAkanksha0% (1)

- Global Drone Market Projections - AsteriaDocument13 pagesGlobal Drone Market Projections - AsteriaAkankshaNo ratings yet

- Ob 05Document26 pagesOb 05nayangoelNo ratings yet

- Case Study: Fabguard'S - Book My Mentor' IntroductionDocument2 pagesCase Study: Fabguard'S - Book My Mentor' IntroductionAkankshaNo ratings yet

- Global Drone Market Projections - AsteriaDocument13 pagesGlobal Drone Market Projections - AsteriaAkankshaNo ratings yet

- ResponseDocument1 pageResponseAkankshaNo ratings yet

- Organisational Behaviour Notes PTUDocument89 pagesOrganisational Behaviour Notes PTUOsamaAnjumNo ratings yet

- Communicating With LFBB: RecommendDocument1 pageCommunicating With LFBB: RecommendAkankshaNo ratings yet

- Drone Expo Preparation Check-ListDocument5 pagesDrone Expo Preparation Check-ListAkankshaNo ratings yet

- Acquired Brand Decision Tree Tool: Transition To The Nordson Brand Transition To An Existing Approved Nordson Sub-BrandDocument1 pageAcquired Brand Decision Tree Tool: Transition To The Nordson Brand Transition To An Existing Approved Nordson Sub-BrandAkankshaNo ratings yet

- Tracxn Case StudyDocument2 pagesTracxn Case StudyAkankshaNo ratings yet

- Walmart - KeynotesDocument10 pagesWalmart - KeynotesAkankshaNo ratings yet

- Uniqueness Paradox: Marketing Strategy and Positioningbenchmarking - Benchmarking Is Important. You Should CollectDocument1 pageUniqueness Paradox: Marketing Strategy and Positioningbenchmarking - Benchmarking Is Important. You Should CollectAkankshaNo ratings yet

- 6 Reasons People Buy: RecommendDocument1 page6 Reasons People Buy: RecommendAkankshaNo ratings yet

- Walmart - KeynotesDocument10 pagesWalmart - KeynotesAkankshaNo ratings yet

- 908 Sanchita Chauhan Faculty Profile 1Document2 pages908 Sanchita Chauhan Faculty Profile 1AkankshaNo ratings yet

- 908 Sanchita Chauhan Faculty Profile 1Document2 pages908 Sanchita Chauhan Faculty Profile 1AkankshaNo ratings yet

- Walmart Success in Mexico, Canada and China Global Expansion, Strategies, Entry Modes, Threats and Opportunities (Finalized)Document11 pagesWalmart Success in Mexico, Canada and China Global Expansion, Strategies, Entry Modes, Threats and Opportunities (Finalized)LeesaChenNo ratings yet

- Evolution and Development of International IPR RegimesDocument18 pagesEvolution and Development of International IPR RegimesAkankshaNo ratings yet

- Walmart - KeynotesDocument10 pagesWalmart - KeynotesAkankshaNo ratings yet

- Notification NABARD Asst Manager PostsDocument28 pagesNotification NABARD Asst Manager Postsrakesh_200003No ratings yet

- E-Receipt For State Bank Collect PaymentDocument1 pageE-Receipt For State Bank Collect PaymentAkankshaNo ratings yet

- Introduction To Bangladesh Leather IndustryDocument28 pagesIntroduction To Bangladesh Leather IndustryMostafa Noman DeepNo ratings yet

- SKILLO VILLA Group 7 FinalDocument18 pagesSKILLO VILLA Group 7 FinalPrateek Kumar vlogsNo ratings yet

- Test Banks Chapter 6 PDFDocument25 pagesTest Banks Chapter 6 PDFHeba SamiNo ratings yet

- Retail LogisticsDocument1 pageRetail LogisticsCuteEmo nyxNo ratings yet

- Supply Chain Management at Cattle Feedlot CompanyDocument3 pagesSupply Chain Management at Cattle Feedlot CompanyAmanda Viona Shafitri 3006No ratings yet

- Business Plan Feasibility Edna Mall Expansion Project ProposalDocument30 pagesBusiness Plan Feasibility Edna Mall Expansion Project ProposalShimels Shawel ZewudieNo ratings yet

- Index of Activities: Chartered Accountants Program Financial Accounting & ReportingDocument150 pagesIndex of Activities: Chartered Accountants Program Financial Accounting & ReportingJAGRUITI JAGRITINo ratings yet

- Almednralejo Chap7 DiscussionDocument10 pagesAlmednralejo Chap7 DiscussionRhywen Fronda GilleNo ratings yet

- Schedule Impact Analysis 1648959255Document54 pagesSchedule Impact Analysis 1648959255Khaled Abdel bakiNo ratings yet

- Strategic Souring and Category ManagementDocument24 pagesStrategic Souring and Category ManagementBlaze PanevNo ratings yet

- Aqap 2070 2019 Eng DataDocument80 pagesAqap 2070 2019 Eng Data신동득No ratings yet

- Conceptual Framework For Financial Reporting. General PrinciplesDocument5 pagesConceptual Framework For Financial Reporting. General PrinciplesLuis PurutongNo ratings yet

- Eastern Refinery Limited Eastern Refinery LimitedDocument1 pageEastern Refinery Limited Eastern Refinery LimitedMuntasir MunirNo ratings yet

- Chapter 9 ReportDocument44 pagesChapter 9 ReportArt Virgel DensingNo ratings yet

- Introduction to Quality Assurance in the Analytical Chemistry LaboratoryDocument25 pagesIntroduction to Quality Assurance in the Analytical Chemistry LaboratoryLily ERc Peter100% (3)

- Project ppt-1Document17 pagesProject ppt-1GYANDEEP BONIANo ratings yet

- Shut Up and WaitDocument20 pagesShut Up and WaitVersatile Beast100% (1)

- Lean Information For Lean Communication Analysis of Concepts, ToolsDocument13 pagesLean Information For Lean Communication Analysis of Concepts, ToolsMomen AlodatNo ratings yet

- HNB404 Assignment Brief UpdatedDocument8 pagesHNB404 Assignment Brief Updatedentertainment015156No ratings yet

- 0.IM 13 Sub Contractor Management ProcedureDocument79 pages0.IM 13 Sub Contractor Management Procedureharish14586No ratings yet

- Worksheet For Evaluating Alternatives: Use This Tool To Help You Think Through Your AlternativesDocument2 pagesWorksheet For Evaluating Alternatives: Use This Tool To Help You Think Through Your AlternativesrameelNo ratings yet

- HIRARCDocument13 pagesHIRARCfaizNo ratings yet

- MBA21094 - Kothapalli Sai Mythili - ENVPDocument32 pagesMBA21094 - Kothapalli Sai Mythili - ENVPKOTHAPALLI SAI SARADA MYTHILINo ratings yet

- Valuation and Deals Structuring Concepts and TrendsDocument114 pagesValuation and Deals Structuring Concepts and TrendsBulent InanNo ratings yet

- Relevant CostsDocument82 pagesRelevant CostsRamil ElambayoNo ratings yet

- ISO 9000 VS 9001 ADocument2 pagesISO 9000 VS 9001 AJanieNo ratings yet

- Entrepreneurs and business ownership formsDocument30 pagesEntrepreneurs and business ownership formsEllie Housen100% (1)

- Curriculum Vitae: Anthovan Adyna PutraDocument28 pagesCurriculum Vitae: Anthovan Adyna PutraIKRIMA SABRINo ratings yet

- Relevant CostingDocument7 pagesRelevant CostingVassy EsperatNo ratings yet

- Learning To Lead at ToyotaDocument11 pagesLearning To Lead at ToyotaerkbsaNo ratings yet