You might also like

- Sean 2022 Tax ReturnDocument18 pagesSean 2022 Tax Returnaaakinkumi115100% (1)

- Csec Poa January 2012 p2Document9 pagesCsec Poa January 2012 p2Renelle RampersadNo ratings yet

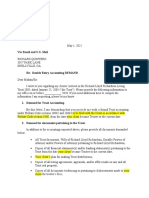

- Sample Accounting Demand LetterDocument2 pagesSample Accounting Demand LetterJOHNNY100% (2)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Statement of CashflowDocument9 pagesStatement of CashflowOwen Lustre50% (2)

- The Math of Intrinsic ValueDocument33 pagesThe Math of Intrinsic ValuelogeshmechNo ratings yet

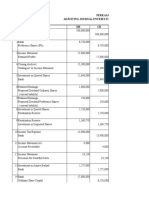

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

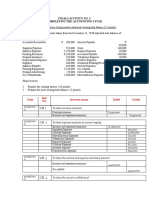

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- 2020 Acc 410 Test 1Document8 pages2020 Acc 410 Test 1Kesa Metsi100% (1)

- ACCT 4200 Project Solution - Final Posting 2022Document14 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- BUSINESS COMBINATION Lecture NotesDocument4 pagesBUSINESS COMBINATION Lecture NotesJia Cruz0% (1)

- Cash Flow Tutorial QnsDocument13 pagesCash Flow Tutorial QnsCristian Renatus100% (1)

- M4 - Problem Exercises - Statement of Financial Position PDFDocument7 pagesM4 - Problem Exercises - Statement of Financial Position PDFCamille CastroNo ratings yet

- Far110 Group Assignment 2Document7 pagesFar110 Group Assignment 21ANurul AnisNo ratings yet

- Class Discussion On Ratios 28022023Document2 pagesClass Discussion On Ratios 28022023lil telNo ratings yet

- Consolidated Statement of Financial Position As at 31 December 20X2 20X2 20X1 Rs.000 Rs.000Document1 pageConsolidated Statement of Financial Position As at 31 December 20X2 20X2 20X1 Rs.000 Rs.000.No ratings yet

- Rivera and Santos PartnershipDocument31 pagesRivera and Santos PartnershipDaneca GallardoNo ratings yet

- PDE4232 Individual Coursework - 2023-24 UpdatedDocument5 pagesPDE4232 Individual Coursework - 2023-24 UpdatedTariq KhanNo ratings yet

- Tutorial 8Document6 pagesTutorial 8WEI QUAN LEENo ratings yet

- Grade 11 Test On AdjustmentsDocument6 pagesGrade 11 Test On AdjustmentsENKK 25No ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document15 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- Financial Statement AnalysisDocument2 pagesFinancial Statement Analysissmallvin62No ratings yet

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Financial Statement AnalysisDocument4 pagesFinancial Statement AnalysisAsad RehmanNo ratings yet

- Poa 2012 Jan p.2.q.1 1Document4 pagesPoa 2012 Jan p.2.q.1 1RealGenius (Carl)No ratings yet

- Socw - 1263543589Document7 pagesSocw - 1263543589dolevov652No ratings yet

- BU51009 (5BA) - Assessed Coursework - EBT 2019-20Document2 pagesBU51009 (5BA) - Assessed Coursework - EBT 2019-20Sravya MagantiNo ratings yet

- Advanced Accounting 2BDocument4 pagesAdvanced Accounting 2BHarusiNo ratings yet

- Income Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsDocument1 pageIncome Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsAik Luen LimNo ratings yet

- Incomplete Records: Calculation of Profit or Loss (Without Preparing Financial Statements)Document5 pagesIncomplete Records: Calculation of Profit or Loss (Without Preparing Financial Statements)Tawanda Tatenda Herbert100% (1)

- Cashflwo TABBA F7Document6 pagesCashflwo TABBA F7Pocpoca100% (2)

- Question ADV GMDocument6 pagesQuestion ADV GMsherlockNo ratings yet

- Advanced Accounting 2CDocument5 pagesAdvanced Accounting 2CHarusiNo ratings yet

- Acc106 Assignment 2 Tie Beauty Enterprise FinalDocument15 pagesAcc106 Assignment 2 Tie Beauty Enterprise Finalnur anisNo ratings yet

- Answer Sheet Mock Test 23Document5 pagesAnswer Sheet Mock Test 23Nam Nguyễn HoàngNo ratings yet

- What Are The Advantages To A Business of Being Formed As A Company? What Are The Disadvantages?Document12 pagesWhat Are The Advantages To A Business of Being Formed As A Company? What Are The Disadvantages?Nguyễn HoàngNo ratings yet

- Class Problem: 2Document7 pagesClass Problem: 2Riad FaisalNo ratings yet

- SFP ACT 2021 Answer SheetDocument1 pageSFP ACT 2021 Answer SheetmoreNo ratings yet

- Cash Flow Part 2 For ClassDocument9 pagesCash Flow Part 2 For ClassKgothatso ArnanzaNo ratings yet

- FE QUESTION FIN 2224 Sept2021Document6 pagesFE QUESTION FIN 2224 Sept2021Tabish HyderNo ratings yet

- DR Group - 2019-2020Document43 pagesDR Group - 2019-2020Mohammad Rejwan UllahNo ratings yet

- Pa Revision For FinalsDocument9 pagesPa Revision For FinalsKhải Hưng NguyễnNo ratings yet

- 5.2. Unit 5 AAB AP A2 Report SunDocument5 pages5.2. Unit 5 AAB AP A2 Report SunHằng Nguyễn ThuNo ratings yet

- Answer Sheet Mock Test 23-2Document5 pagesAnswer Sheet Mock Test 23-2Nam Nguyễn HoàngNo ratings yet

- ACC106 Assignment AccountDocument5 pagesACC106 Assignment AccountsyafiqahNo ratings yet

- Cash Flow Statement PT - NandiDocument1 pageCash Flow Statement PT - NandiHelena KambongelaNo ratings yet

- Quiz - 2 - BAAB1014 - (Sept2022) AnswerDocument8 pagesQuiz - 2 - BAAB1014 - (Sept2022) AnswerTheresa AnneNo ratings yet

- Bac316 018358Document4 pagesBac316 018358arthurNo ratings yet

- Brianne Kylle Dela Cruz FSA3 111Document29 pagesBrianne Kylle Dela Cruz FSA3 111Kathlene JaoNo ratings yet

- Brianne Kylle Dela Cruz FSA3 10 20 21Document35 pagesBrianne Kylle Dela Cruz FSA3 10 20 21Kathlene JaoNo ratings yet

- Workshop 5 QsDocument7 pagesWorkshop 5 QsNaresh SehdevNo ratings yet

- Toaz - Info Prelim Midterm PRDocument98 pagesToaz - Info Prelim Midterm PRClandestine SoulNo ratings yet

- JournalDocument7 pagesJournalathierahNo ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- Daa 101 Introduction To Accounting Ii - RispahDocument4 pagesDaa 101 Introduction To Accounting Ii - RispahSpencerNo ratings yet

- Capital Budgeting - 2021Document7 pagesCapital Budgeting - 2021Mohamed ZaitoonNo ratings yet

- Manufacturing AccountingDocument12 pagesManufacturing AccountingNana OpokuNo ratings yet

- PYQ June 2018Document4 pagesPYQ June 2018Nur Amira NadiaNo ratings yet

- ACCN. LOCKDOWN WORKSHEET 2aDocument2 pagesACCN. LOCKDOWN WORKSHEET 2aRyno de BeerNo ratings yet

- Accounting 621Document2 pagesAccounting 621Sarah Precious NkoanaNo ratings yet

- Acc PaperDocument4 pagesAcc PaperYUSRINA MOHD YUSOFFNo ratings yet

- June 2009 Fa4a1Document9 pagesJune 2009 Fa4a1ksakala58No ratings yet

- T Fraser, Motif and Meath Cash Flow QuestionsDocument5 pagesT Fraser, Motif and Meath Cash Flow Questionschalah DeriNo ratings yet

- Best Options BoooksDocument1 pageBest Options Boooksabhaymvyas1144No ratings yet

- 4 20200212 Format Teaching Prof Asso ProfDocument10 pages4 20200212 Format Teaching Prof Asso Profabhaymvyas1144No ratings yet

- FireShot Capture 062 - Level 13 - 301 - 325 - 5000 German Words (Top 87%) - MemriseDocument1 pageFireShot Capture 062 - Level 13 - 301 - 325 - 5000 German Words (Top 87%) - Memriseabhaymvyas1144No ratings yet

- Shri G. S. Institute of Technology and ScienceDocument32 pagesShri G. S. Institute of Technology and Scienceabhaymvyas1144No ratings yet

- FireShot Capture 057 - Level 8 - 176 - 200 - 5000 German Words (Top 87%) - MemriseDocument1 pageFireShot Capture 057 - Level 8 - 176 - 200 - 5000 German Words (Top 87%) - Memriseabhaymvyas1144No ratings yet

- FireShot Capture 001 - Level 1 - 1 - 25 - 5000 German Words (Top 87%) - MemriseDocument1 pageFireShot Capture 001 - Level 1 - 1 - 25 - 5000 German Words (Top 87%) - Memriseabhaymvyas1144No ratings yet

- Monitor 28 3 21Document2 pagesMonitor 28 3 21abhaymvyas1144No ratings yet

- FireShot Capture 007 - Level 6 - 126 - 150 - 5000 German Words (Top 87%) - MemriseDocument1 pageFireShot Capture 007 - Level 6 - 126 - 150 - 5000 German Words (Top 87%) - Memriseabhaymvyas1144No ratings yet

- Indian Institute of Technology Bombay Powai, Mumbai 400 076Document5 pagesIndian Institute of Technology Bombay Powai, Mumbai 400 076abhaymvyas1144No ratings yet

- Monitor 19 NovDocument1 pageMonitor 19 Novabhaymvyas1144No ratings yet

- (Autumn Semester) : TH THDocument4 pages(Autumn Semester) : TH THabhaymvyas1144No ratings yet

- Monitor 15 OctDocument2 pagesMonitor 15 Octabhaymvyas1144No ratings yet

- Monitor 23sepDocument4 pagesMonitor 23sepabhaymvyas1144No ratings yet

- Monitor 13 9 2020Document2 pagesMonitor 13 9 2020abhaymvyas1144No ratings yet

- Acccob2 Portfolio2Document19 pagesAcccob2 Portfolio2Reshawn Kimi SantosNo ratings yet

- Age Is Not A Limit For Lajwanti Phulkari'Document2 pagesAge Is Not A Limit For Lajwanti Phulkari'Diksha Kanwar100% (1)

- IDFC BANK Repayment Schedule-10865556Document2 pagesIDFC BANK Repayment Schedule-10865556Dinesh KumarNo ratings yet

- Global and Caribbean Tourism and Its Contribution To The Global EconomyDocument25 pagesGlobal and Caribbean Tourism and Its Contribution To The Global EconomyDre's Graphic DesignsNo ratings yet

- Factors Influencing Plant LayoutDocument1 pageFactors Influencing Plant LayoutAkarshNo ratings yet

- Date (DD/MM) Value Doc - No Particulars Debit Credit BalanceDocument6 pagesDate (DD/MM) Value Doc - No Particulars Debit Credit BalanceHassaanNo ratings yet

- Introduction To Managerial EconomicsDocument13 pagesIntroduction To Managerial EconomicsPrayag rajNo ratings yet

- Summer Internship Final Report: Submitted To: Submitted byDocument35 pagesSummer Internship Final Report: Submitted To: Submitted byAyushi NautiyalNo ratings yet

- Assignment - 3Document3 pagesAssignment - 3Aditi RawatNo ratings yet

- Crypto PecuniaDocument20 pagesCrypto PecuniaOtter VictorNo ratings yet

- Ci Awb Sample Rootcroop Ofi 28.07.2023Document3 pagesCi Awb Sample Rootcroop Ofi 28.07.2023hendy febrianiNo ratings yet

- Indonesia Aviation Decarbonization Roundtable - FinalDocument33 pagesIndonesia Aviation Decarbonization Roundtable - FinalEvans Azka FNo ratings yet

- Westpac New Zealand LTD V New Dawn Holdings LTD - Bc202261586Document25 pagesWestpac New Zealand LTD V New Dawn Holdings LTD - Bc202261586NUR INSYIRAH ZAININo ratings yet

- Slm-Iii Sem - Corpo AccountingDocument304 pagesSlm-Iii Sem - Corpo AccountingAlbin K BijuNo ratings yet

- Dokumen - Tips Dubai Islamic Bank Pakistan Internship ReportdocxDocument19 pagesDokumen - Tips Dubai Islamic Bank Pakistan Internship Reportdocxnouman sandhuNo ratings yet

- Project Management 1 EMBA JnUDocument12 pagesProject Management 1 EMBA JnUShamima AkterNo ratings yet

- 1 s2.0 S095965262300046X MainDocument13 pages1 s2.0 S095965262300046X MainLaura NituNo ratings yet

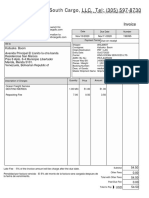

- South Cargo, LLC. Tel: (305) 597-8730: InvoiceDocument1 pageSouth Cargo, LLC. Tel: (305) 597-8730: InvoiceChevyveronaNo ratings yet

- ReportHistory 48173905Document46 pagesReportHistory 48173905Dhanush AsapuNo ratings yet

- Asuransi Dayin Mitra TBK Asdm: Company History Dividend AnnouncementDocument3 pagesAsuransi Dayin Mitra TBK Asdm: Company History Dividend AnnouncementJandri Zhen TomasoaNo ratings yet

- Marketing Management: Prof. Vibhas AmawateDocument42 pagesMarketing Management: Prof. Vibhas AmawateSagar GadhviNo ratings yet

- Case StudiesDocument3 pagesCase StudiesPranjal Satpute100% (1)

- Inflation and Its TypesDocument12 pagesInflation and Its TypesHarnoorpreet JotkaurNo ratings yet

- Voluntary Petition For Non-Individuals Filing For BankruptcyDocument23 pagesVoluntary Petition For Non-Individuals Filing For BankruptcyMike McSweeneyNo ratings yet

- 11th Economics Reduced Syllabus 2021 - 2022 English Medium - WWW - Kalvikadal.inDocument8 pages11th Economics Reduced Syllabus 2021 - 2022 English Medium - WWW - Kalvikadal.inDhivyaNo ratings yet

- Adverse Action NoticeDocument2 pagesAdverse Action NoticepassmeinNo ratings yet