You might also like

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- 6 - Basic Methods For Making Economy StudiesDocument25 pages6 - Basic Methods For Making Economy StudiesChu KathNo ratings yet

- Profitability of An InvestmentDocument3 pagesProfitability of An InvestmentnikunjNo ratings yet

- Profitability AnalysisDocument43 pagesProfitability AnalysisAvinash Iyer100% (1)

- Payback Period-1Document12 pagesPayback Period-1OlamiNo ratings yet

- Internal Rate of ReturnDocument28 pagesInternal Rate of ReturnVaidyanathan Ravichandran100% (1)

- Econ 7Document10 pagesEcon 7ceejay RedondiezNo ratings yet

- Course Learning Outcomes For Unit II: Opportunity Costs and Organizational ArchitectureDocument3 pagesCourse Learning Outcomes For Unit II: Opportunity Costs and Organizational ArchitectureSwapan Kumar SahaNo ratings yet

- Capital BudgetingDocument5 pagesCapital BudgetingMaria StephenNo ratings yet

- Net Present Value Method Net Present Value Method (Also Known As Discounted Cash Flow Method) Is A PopularDocument15 pagesNet Present Value Method Net Present Value Method (Also Known As Discounted Cash Flow Method) Is A PopularImranNo ratings yet

- Main Project Capital Budgeting MbaDocument110 pagesMain Project Capital Budgeting MbaRaviKiran Avula65% (34)

- Project Appraisal - Investment Appraisal - 2023Document40 pagesProject Appraisal - Investment Appraisal - 2023ThaboNo ratings yet

- Written by Professor Gregory M. Burbage, MBA, CPA, CMA, CFM: Notes-C14Document2 pagesWritten by Professor Gregory M. Burbage, MBA, CPA, CMA, CFM: Notes-C14Joeban R. PazaNo ratings yet

- Rate of Return Method ExplainedDocument11 pagesRate of Return Method ExplainedAira_DirectonerNo ratings yet

- PROJECT APPRAISAL METHODSDocument28 pagesPROJECT APPRAISAL METHODSMîñåk ŞhïïNo ratings yet

- Financial Management Basics Capital BudgetingDocument14 pagesFinancial Management Basics Capital BudgetingVandana KaushikNo ratings yet

- Net Present Value MethodDocument9 pagesNet Present Value MethodRain Roslan100% (2)

- Unit 4 - CEPDEDocument71 pagesUnit 4 - CEPDEsrinu02062No ratings yet

- IRR, ERR and Payback - pptx-1470084967Document41 pagesIRR, ERR and Payback - pptx-1470084967Alexie GonzalesNo ratings yet

- Capital Budgeting Techniques and CalculationsDocument22 pagesCapital Budgeting Techniques and CalculationsKaRin MerRoNo ratings yet

- Chapter 3 BecDocument11 pagesChapter 3 BecStephen ZhaoNo ratings yet

- Chapter 8 EcoDocument10 pagesChapter 8 EcoAngel Jasmin TupazNo ratings yet

- Assignment On FaseelDocument6 pagesAssignment On FaseelAbdul KhanNo ratings yet

- Internal Rate of ReturnDocument4 pagesInternal Rate of Returnram_babu_59No ratings yet

- Summary of Capital Budgeting Techniques GitmanDocument12 pagesSummary of Capital Budgeting Techniques GitmanHarold Dela FuenteNo ratings yet

- Capital Budgeting AnalysisDocument37 pagesCapital Budgeting AnalysisEsha ThawalNo ratings yet

- PAYBACK PERIOD ANALYSIS: HOW TO EVALUATE INVESTMENT PROJECTS USING THE PAYBACK METHODDocument7 pagesPAYBACK PERIOD ANALYSIS: HOW TO EVALUATE INVESTMENT PROJECTS USING THE PAYBACK METHODSurya SumanNo ratings yet

- What Is Internal Rate of Return (IRR) ?Document10 pagesWhat Is Internal Rate of Return (IRR) ?anayochukwuNo ratings yet

- BUAD 839 ASSIGNMENT (Group F)Document4 pagesBUAD 839 ASSIGNMENT (Group F)Yemi Jonathan OlusholaNo ratings yet

- Project Eco Begrippen LijstDocument3 pagesProject Eco Begrippen LijstKishen HarlalNo ratings yet

- 03 - 20th Aug Capital Budgeting, 2019Document37 pages03 - 20th Aug Capital Budgeting, 2019anujNo ratings yet

- Ebtm3103 Slides Topic 3Document26 pagesEbtm3103 Slides Topic 3SUHAILI BINTI BOHORI STUDENTNo ratings yet

- CAPEX Guide: Capital Expenditure and Investment Analysis MethodsDocument8 pagesCAPEX Guide: Capital Expenditure and Investment Analysis Methodsmagoimoi100% (1)

- ARR, IRR and PIDocument8 pagesARR, IRR and PIAli HamzaNo ratings yet

- Chapter 6 Basic Methods For Making Economy StudiesDocument37 pagesChapter 6 Basic Methods For Making Economy StudiesJustine joy cruzNo ratings yet

- CH-2 RivewDocument57 pagesCH-2 RivewMulugeta DefaruNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisAngel MallariNo ratings yet

- Top 21 Real Estate Analysis Measures & Formulas PDFDocument3 pagesTop 21 Real Estate Analysis Measures & Formulas PDFDustin HumphreysNo ratings yet

- Document (1) (3) .EditedDocument7 pagesDocument (1) (3) .EditedMoses WabunaNo ratings yet

- BF 14Document5 pagesBF 14zhairenaguila22No ratings yet

- Candidates expected to calculate theoretical ex-rights priceDocument3 pagesCandidates expected to calculate theoretical ex-rights priceFloyd DaltonNo ratings yet

- Capital Budgeting: Should We Build This Plant?Document33 pagesCapital Budgeting: Should We Build This Plant?Bhuvan SemwalNo ratings yet

- 5 Evaluating A Single ProjectDocument32 pages5 Evaluating A Single ProjectImie CamachoNo ratings yet

- Maximizing Profits Through Profitability Standards and Investment AnalysisDocument27 pagesMaximizing Profits Through Profitability Standards and Investment AnalysisRamez AlaliNo ratings yet

- Example of Calculating IRRDocument6 pagesExample of Calculating IRRJameel AhmadNo ratings yet

- Residual Income ValuationDocument6 pagesResidual Income ValuationKumar AbhishekNo ratings yet

- BUS-635 Final Assignment QuestionsDocument12 pagesBUS-635 Final Assignment QuestionsAlvee Musharrat Hridita 1825132No ratings yet

- Evaluating A Single ProjectDocument31 pagesEvaluating A Single ProjectDave Despabiladeras50% (2)

- Alternative Investment Profitability AnalysisDocument24 pagesAlternative Investment Profitability AnalysisSakthi S100% (1)

- Combined Heating, Cooling & Power HandbookDocument8 pagesCombined Heating, Cooling & Power HandbookFREDIELABRADORNo ratings yet

- Capital BudgetingDocument6 pagesCapital BudgetingHannahbea LindoNo ratings yet

- Economic Evaluation: DefinitionsDocument5 pagesEconomic Evaluation: DefinitionsAnglicaNo ratings yet

- ProfitabilityDocument12 pagesProfitabilityAbdullah RamzanNo ratings yet

- Capital Budgeting of Googlosoft Technologies 1Document16 pagesCapital Budgeting of Googlosoft Technologies 1Dheeraj Y V S RNo ratings yet

- Internal Rate of ReturnDocument4 pagesInternal Rate of ReturnMaria Ali ZulfiqarNo ratings yet

- Internal Rate of ReturnDocument5 pagesInternal Rate of ReturnCalvince OumaNo ratings yet

- Topic IV - Economic Study MethodsDocument13 pagesTopic IV - Economic Study MethodsMc John PobleteNo ratings yet

- The Internal Rate of Return MethodDocument4 pagesThe Internal Rate of Return MethodMùhammad TàhaNo ratings yet

- Chapter 3Document173 pagesChapter 3Maria HafeezNo ratings yet

- Internal Rate of Return - Wikipedia, The Free EncyclopediaDocument8 pagesInternal Rate of Return - Wikipedia, The Free EncyclopediaOluwafemi Samuel AdesanmiNo ratings yet

- Activity 11Document2 pagesActivity 11raymond moscosoNo ratings yet

- ESECON Lesson Plan Week 14Document2 pagesESECON Lesson Plan Week 14raymond moscosoNo ratings yet

- Activity 12Document2 pagesActivity 12raymond moscosoNo ratings yet

- Activity 12Document2 pagesActivity 12raymond moscosoNo ratings yet

- Midterm Exam - Esecon 1ST Sem. 2021-2022Document3 pagesMidterm Exam - Esecon 1ST Sem. 2021-2022raymond moscosoNo ratings yet

- The ERR Method and Payback Period Method Handout (Week 10)Document3 pagesThe ERR Method and Payback Period Method Handout (Week 10)raymond moscosoNo ratings yet

- ESECON Lesson Plan Week 11Document2 pagesESECON Lesson Plan Week 11raymond moscosoNo ratings yet

- Midterm Exam - Esecon 1ST Sem. 2021-2022Document3 pagesMidterm Exam - Esecon 1ST Sem. 2021-2022raymond moscosoNo ratings yet

- ESECON Lesson Plan Week 10Document2 pagesESECON Lesson Plan Week 10raymond moscosoNo ratings yet

- Lesson PlanDocument2 pagesLesson Planraymond moscosoNo ratings yet

- Lesson PlanDocument2 pagesLesson Planraymond moscosoNo ratings yet

- Lesson 8 MIller Indices and Packing EfficiencyDocument9 pagesLesson 8 MIller Indices and Packing Efficiencyraymond moscosoNo ratings yet

- COMMUNICATION MODELS (Week 3) - GECDocument12 pagesCOMMUNICATION MODELS (Week 3) - GECraymond moscosoNo ratings yet

- ESECON Lesson Plan Week 4Document2 pagesESECON Lesson Plan Week 4raymond moscosoNo ratings yet

- Gec 105 - Non-Verbal CommunicationDocument5 pagesGec 105 - Non-Verbal Communicationraymond moscosoNo ratings yet

- Chapter 5. Equity MarketsDocument150 pagesChapter 5. Equity MarketsHiếu Nhi TrịnhNo ratings yet

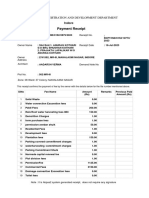

- Payment Receipt: Urban Administration and Development DepartmentDocument2 pagesPayment Receipt: Urban Administration and Development Departmentaadarsh vermaNo ratings yet

- Underwriting SOPDocument5 pagesUnderwriting SOPChris JacksonNo ratings yet

- Invoice: Thank You For Staying With Us at Fairfield by Marriott, KolkataDocument1 pageInvoice: Thank You For Staying With Us at Fairfield by Marriott, Kolkatakousik ChatterjeeNo ratings yet

- 10 1108 - MF 06 2020 0300Document20 pages10 1108 - MF 06 2020 0300fenny maryandiNo ratings yet

- PE PlayersDocument9 pagesPE PlayersSatbir Singh100% (1)

- Gov Act Reviewer (Punzalan)Document13 pagesGov Act Reviewer (Punzalan)Kenneth WilburNo ratings yet

- Statement of Commission: Mobile Phones. Simply Dial 525 11# To Pay. To Know More, SMS MPAY To 56767Document1 pageStatement of Commission: Mobile Phones. Simply Dial 525 11# To Pay. To Know More, SMS MPAY To 56767L VermaNo ratings yet

- Lirag Textile Mills Vs Sss - FullDocument7 pagesLirag Textile Mills Vs Sss - FullLariza AidieNo ratings yet

- Director Commercial Real Estate in Columbus OH Resume Richard WolneyDocument2 pagesDirector Commercial Real Estate in Columbus OH Resume Richard WolneyRichardWolneyNo ratings yet

- Cadbury Schweppes DF 2006Document1 pageCadbury Schweppes DF 2006JORGENo ratings yet

- My CA Articleship Experience of Working at Deloitte (Big 4)Document5 pagesMy CA Articleship Experience of Working at Deloitte (Big 4)Rudrin Das100% (1)

- Letter of CreditDocument31 pagesLetter of Creditmariachristina8850% (2)

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsan100% (1)

- AccountingDocument414 pagesAccountingMuddasir HussainNo ratings yet

- LKBF 2Document8 pagesLKBF 2Aseki Shakib Khan SimantoNo ratings yet

- Bcoc 136Document2 pagesBcoc 136Suraj JaiswalNo ratings yet

- Bootcamp 2018 Quant Wipro I1Document2 pagesBootcamp 2018 Quant Wipro I1Dileep TrivediNo ratings yet

- ADM 3351-Final With SolutionsDocument14 pagesADM 3351-Final With SolutionsGraeme RalphNo ratings yet

- Cash Flow StatmentDocument91 pagesCash Flow StatmentSathishmuNo ratings yet

- Valuation of Tata SteelDocument3 pagesValuation of Tata SteelNishtha Mehra100% (1)

- Starting The Venture Business PlanDocument19 pagesStarting The Venture Business PlanIshan RatnakarNo ratings yet

- Digital Currencies As Tools For Electronic PaymentDocument6 pagesDigital Currencies As Tools For Electronic PaymentSuchi UshaNo ratings yet

- Feasibility Analysis Offtake CANDI From The UMBULAN Drinking Water Supply SystemDocument7 pagesFeasibility Analysis Offtake CANDI From The UMBULAN Drinking Water Supply SystemInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- ITO notice for escaped incomeDocument2 pagesITO notice for escaped incomeSukalp WarhekarNo ratings yet

- Cash Flow Statement New For YoutubeDocument48 pagesCash Flow Statement New For YoutubeTapan BarikNo ratings yet

- Audited Financial Statements Airlines 2021Document60 pagesAudited Financial Statements Airlines 2021VENICE OMOLONNo ratings yet

- SEC Form 20-Is Definitive - 2015 - 0Document263 pagesSEC Form 20-Is Definitive - 2015 - 0Aeron Paul AntonioNo ratings yet

- Ice Giants Desserts & Snack Inc.Document9 pagesIce Giants Desserts & Snack Inc.ronnel_amper12345678No ratings yet