You might also like

- Franchise Agreement Between Emeralds Fields Trading Inc. and I.L. Antonio Petroleum CorporationDocument19 pagesFranchise Agreement Between Emeralds Fields Trading Inc. and I.L. Antonio Petroleum CorporationMartha Jewel GomezNo ratings yet

- International Journal of Economics and Financial Issues Consumers' Attitude Towards Usage of Debit and Credit Cards: Evidences From The Digital Economy of PakistanDocument10 pagesInternational Journal of Economics and Financial Issues Consumers' Attitude Towards Usage of Debit and Credit Cards: Evidences From The Digital Economy of PakistanSummamNo ratings yet

- The Relationship Between Credit Card Attributes and The Demographic Characteristics of Card Users in ChinaDocument19 pagesThe Relationship Between Credit Card Attributes and The Demographic Characteristics of Card Users in ChinaAbhijeet GangulyNo ratings yet

- Moderating Effects of PerceivedDocument20 pagesModerating Effects of PerceivedharyeniNo ratings yet

- Modeling Customers Intention To Use E-Wallet in ADocument5 pagesModeling Customers Intention To Use E-Wallet in AFaten bakloutiNo ratings yet

- Credit Card Uses Pattern Among Student in BangladeshDocument8 pagesCredit Card Uses Pattern Among Student in Bangladeshsalmanzaki12No ratings yet

- Banking Technology and CashlessDocument12 pagesBanking Technology and Cashlessjose david perezNo ratings yet

- 6026-Article Text-16886-1-10-20201201Document12 pages6026-Article Text-16886-1-10-20201201Nuriel AguilarNo ratings yet

- Paper 5Document15 pagesPaper 5Ahmed A. M. Al-AfifiNo ratings yet

- Monetary Policy Transmission and Credit Cards - Evidence From IndoDocument27 pagesMonetary Policy Transmission and Credit Cards - Evidence From IndoNanang ArifinNo ratings yet

- Awareness About Cash Less Economy Among Students: K. Girija & M. NandhiniDocument8 pagesAwareness About Cash Less Economy Among Students: K. Girija & M. NandhiniTJPRC PublicationsNo ratings yet

- Yao 2018Document13 pagesYao 2018Victor Josue FloresNo ratings yet

- 66459-Article Text-171732-1-10-20220331Document16 pages66459-Article Text-171732-1-10-20220331lehoangduc1972No ratings yet

- 136-Full Manuscript-702-1-10-20210210Document19 pages136-Full Manuscript-702-1-10-20210210Azwa SafrinaNo ratings yet

- Integration of UTAUT Model in Thailand Cashless Payment System Adoption: The Mediating Role of Perceived Risk and TrustDocument26 pagesIntegration of UTAUT Model in Thailand Cashless Payment System Adoption: The Mediating Role of Perceived Risk and TrustDeepak RoyNo ratings yet

- Credit Card Usage Patterns in NepalDocument18 pagesCredit Card Usage Patterns in NepalPrakash KhadkaNo ratings yet

- Adbi Financial Inclusion AsiaDocument151 pagesAdbi Financial Inclusion AsiaMarius AngaraNo ratings yet

- 5 6059900569177293719Document76 pages5 6059900569177293719chinna ladduNo ratings yet

- Analysing Consumer Adoption of Cashless Payment in MalaysiaDocument11 pagesAnalysing Consumer Adoption of Cashless Payment in Malaysiaridho zynNo ratings yet

- 1 s2.0 S1877042814029760 MainDocument9 pages1 s2.0 S1877042814029760 MainVittaya RiaNo ratings yet

- Growth of The Use of Plastic Money in IndiaDocument46 pagesGrowth of The Use of Plastic Money in IndiaHarshitGupta81% (21)

- Credit Card Dues: Faculty of Business and Management, Universiti Teknologi MARA, MalaysiaDocument7 pagesCredit Card Dues: Faculty of Business and Management, Universiti Teknologi MARA, MalaysiaDiela KasimNo ratings yet

- Odad 2023 Vol8iss1 52 73 5938Document22 pagesOdad 2023 Vol8iss1 52 73 5938linhmilumiluNo ratings yet

- SYNOSISDocument29 pagesSYNOSISRahul SunilNo ratings yet

- Utaut2021journal of Theoretical and Applied Electronic Commerce Research Open AccessDocument20 pagesUtaut2021journal of Theoretical and Applied Electronic Commerce Research Open AccessFaisal KeryNo ratings yet

- Intraduction To Plastic MoneyDocument8 pagesIntraduction To Plastic MoneyArul KiranNo ratings yet

- Jetirz006011 PDFDocument9 pagesJetirz006011 PDFChiranjit KamilyaNo ratings yet

- Factors Affecting Growth of Plastic Money in PakistanDocument5 pagesFactors Affecting Growth of Plastic Money in PakistanArafat IslamNo ratings yet

- Determinant of Cashless in MalaysiaDocument11 pagesDeterminant of Cashless in MalaysiaHBC ONE SOLUTIONNo ratings yet

- Pia InglesDocument45 pagesPia InglesYahir MedellinNo ratings yet

- ProjectDocument76 pagesProjectDashing HemantNo ratings yet

- The Changing Face of Asian Personal Financial Services: September 2011Document4 pagesThe Changing Face of Asian Personal Financial Services: September 2011Samadarshi SiddharthaNo ratings yet

- ISEAS Perspective 2021 112Document9 pagesISEAS Perspective 2021 112Intuch SomboontanasarnNo ratings yet

- Economic Effects of Foreign Bank Liberalization and E-Payment: A Comparative Study of The Philippines and SingaporeDocument15 pagesEconomic Effects of Foreign Bank Liberalization and E-Payment: A Comparative Study of The Philippines and SingaporeInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Drivers and Outcomes of Consumer Engagement: Insights From Mobile Money Usage in GhanaDocument20 pagesDrivers and Outcomes of Consumer Engagement: Insights From Mobile Money Usage in Ghanamingchiat88No ratings yet

- Credit CardDocument50 pagesCredit CardThakur Bhim Singh67% (3)

- A/ The Reason Why Choosing This Subject: 1) The Importance of Digital Banking Development in VietnamDocument41 pagesA/ The Reason Why Choosing This Subject: 1) The Importance of Digital Banking Development in VietnamYến NhiNo ratings yet

- GERALDMATINDEJOURNALPAPER2016Document15 pagesGERALDMATINDEJOURNALPAPER2016Shammah MahobeleNo ratings yet

- A/ The Reason Why Choosing This Subject: 1) The Importance of Digital Banking Development in VietnamDocument27 pagesA/ The Reason Why Choosing This Subject: 1) The Importance of Digital Banking Development in VietnamYến NhiNo ratings yet

- Society's Attitude Towards Debit and Credit CardsDocument76 pagesSociety's Attitude Towards Debit and Credit Cardskaran chaware100% (1)

- Growth of Plastic Money in Pakistan - A Study of Factors Affecting Use of Plastic MoneyDocument14 pagesGrowth of Plastic Money in Pakistan - A Study of Factors Affecting Use of Plastic MoneyPhoenix LabradorsNo ratings yet

- The Impact of CSR On Trust and Intention To Adopt Mobile Banking: Evidence From Developing CountryDocument20 pagesThe Impact of CSR On Trust and Intention To Adopt Mobile Banking: Evidence From Developing CountryLee Hock SengNo ratings yet

- IJCRT2309325Document10 pagesIJCRT2309325sunilshayriwalashortsNo ratings yet

- Abdullah BaabdullahDocument41 pagesAbdullah BaabdullahFadel BusthomyNo ratings yet

- 2.Ijbgm-A Cointegration Analysis of The Relationship Between Money Supply and Financial Inclusion in Nigeria - 1981-2016 - RewrittenDocument14 pages2.Ijbgm-A Cointegration Analysis of The Relationship Between Money Supply and Financial Inclusion in Nigeria - 1981-2016 - Rewritteniaset123No ratings yet

- 03_chapters PArt 1 CCDocument21 pages03_chapters PArt 1 CCSheetal SaylekarNo ratings yet

- A Study On Future Prospects of Plastic Money PDFDocument18 pagesA Study On Future Prospects of Plastic Money PDFAbhinav AgrawalNo ratings yet

- Credit CardDocument60 pagesCredit CardBhushan RohaneNo ratings yet

- Admin, Zahayu MD YusofDocument24 pagesAdmin, Zahayu MD YusofFirdaus RazaliNo ratings yet

- Accenture Banking Retail LendingDocument16 pagesAccenture Banking Retail LendingRaunak MotwaniNo ratings yet

- JETIR2201263Document9 pagesJETIR2201263Maha RachithaNo ratings yet

- Credit Card India PDFDocument21 pagesCredit Card India PDFmanojjecrcNo ratings yet

- Literacy and Usage of Credit Cards in IndiaDocument10 pagesLiteracy and Usage of Credit Cards in IndiaMadhur GuptaNo ratings yet

- Banking Services For Smes ' Internationalization: Evaluating Customer SatisfactionDocument19 pagesBanking Services For Smes ' Internationalization: Evaluating Customer SatisfactionnjchengjiayiNo ratings yet

- Chapter 1Document3 pagesChapter 1akhileshNo ratings yet

- DBS BankDocument18 pagesDBS BankAbs PangaderNo ratings yet

- Credit Card Holders in Malaysia Customer PDFDocument15 pagesCredit Card Holders in Malaysia Customer PDFsharath kumarNo ratings yet

- Influencing Factors of Using GCASHDocument8 pagesInfluencing Factors of Using GCASHGilconedo Baya JrNo ratings yet

- Customer Perceived Risk and Adoption of E Banking Services in Southeast Nigeria The Moderating Effect of Educational QualificationDocument13 pagesCustomer Perceived Risk and Adoption of E Banking Services in Southeast Nigeria The Moderating Effect of Educational QualificationEditor IJTSRDNo ratings yet

- The Road to Better Long-Term Care in Asia and the Pacific: Building Systems of Care and Support for Older PersonsFrom EverandThe Road to Better Long-Term Care in Asia and the Pacific: Building Systems of Care and Support for Older PersonsNo ratings yet

- Country Diagnostic Study on Long-Term Care in ThailandFrom EverandCountry Diagnostic Study on Long-Term Care in ThailandNo ratings yet

- RRL (Self-Efficacy)Document14 pagesRRL (Self-Efficacy)John Joshua S. GeronaNo ratings yet

- Journal of Behavioral and Experimental Finance: Liu Liu, Hua ZhangDocument9 pagesJournal of Behavioral and Experimental Finance: Liu Liu, Hua ZhangJohn Joshua S. GeronaNo ratings yet

- Self-Leadership, Financial Self-Efficacy, and Student Loan DebtDocument11 pagesSelf-Leadership, Financial Self-Efficacy, and Student Loan DebtJohn Joshua S. GeronaNo ratings yet

- RRL (Self-Efficacy) (H4)Document17 pagesRRL (Self-Efficacy) (H4)John Joshua S. GeronaNo ratings yet

- Case StudyDocument1 pageCase StudyJohn Joshua S. GeronaNo ratings yet

- Discussion Question1Document2 pagesDiscussion Question1John Joshua S. GeronaNo ratings yet

- RRL (Self-Efficacy)Document12 pagesRRL (Self-Efficacy)John Joshua S. GeronaNo ratings yet

- Grp-2. STM Paper (Whole)Document19 pagesGrp-2. STM Paper (Whole)John Joshua S. GeronaNo ratings yet

- I Love You BabeDocument1 pageI Love You BabeJohn Joshua S. GeronaNo ratings yet

- Negotiable Instruments Law With Bouncing Checks Law: Dycbanil413 Bsba 4Th Year - 1St Semester 2021-2022Document55 pagesNegotiable Instruments Law With Bouncing Checks Law: Dycbanil413 Bsba 4Th Year - 1St Semester 2021-2022John Joshua S. GeronaNo ratings yet

- SpamDocument1 pageSpamJohn Joshua S. GeronaNo ratings yet

- Report of Condition Total AssetsDocument8 pagesReport of Condition Total AssetsJohn Joshua S. GeronaNo ratings yet

- Ritmo DownpaymentDocument1 pageRitmo DownpaymentJohn Joshua S. GeronaNo ratings yet

- RRL (Self-Efficacy)Document14 pagesRRL (Self-Efficacy)John Joshua S. GeronaNo ratings yet

- Game OptionDocument2 pagesGame OptionJohn Joshua S. GeronaNo ratings yet

- Proj Olli BeeDocument7 pagesProj Olli BeeRam BoNo ratings yet

- 3FM Bonifacio Hazel G Activity 4 PDFDocument2 pages3FM Bonifacio Hazel G Activity 4 PDFJohn Joshua S. GeronaNo ratings yet

- Secondary Data SourcesDocument7 pagesSecondary Data SourcesVinay SharmaNo ratings yet

- Secondary Data SourcesDocument7 pagesSecondary Data SourcesVinay SharmaNo ratings yet

- 7 - Pure and Conditional Obligations (1) Classification of ObligationsDocument4 pages7 - Pure and Conditional Obligations (1) Classification of Obligationskeuliseutel chaNo ratings yet

- School Corporate Governance and Risk ManagementDocument1 pageSchool Corporate Governance and Risk ManagementJohn Joshua S. GeronaNo ratings yet

- Ritmo DownpaymentDocument1 pageRitmo DownpaymentJohn Joshua S. GeronaNo ratings yet

- Secondary Data SourcesDocument7 pagesSecondary Data SourcesVinay SharmaNo ratings yet

- Proj Olli BeeDocument7 pagesProj Olli BeeRam BoNo ratings yet

- Activity: Planning Your Recovery Contingencies. It Is A Big Advantage For Facing A Risk SinceDocument1 pageActivity: Planning Your Recovery Contingencies. It Is A Big Advantage For Facing A Risk SinceJohn Joshua S. GeronaNo ratings yet

- Activity: Planning Your Recovery Contingencies. It Is A Big Advantage For Facing A Risk SinceDocument1 pageActivity: Planning Your Recovery Contingencies. It Is A Big Advantage For Facing A Risk SinceJohn Joshua S. GeronaNo ratings yet

- School Corporate Governance and Risk ManagementDocument1 pageSchool Corporate Governance and Risk ManagementJohn Joshua S. GeronaNo ratings yet

- Discussion Question1Document2 pagesDiscussion Question1John Joshua S. GeronaNo ratings yet

- Discussion Question1Document2 pagesDiscussion Question1John Joshua S. GeronaNo ratings yet

- 1 The Companies Act 1994 and Secretarial PracticeDocument45 pages1 The Companies Act 1994 and Secretarial PracticeIQBALNo ratings yet

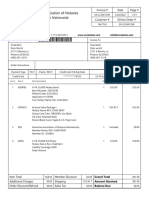

- TAX INVOICEDocument6 pagesTAX INVOICEPraveen YadavNo ratings yet

- Emergence of Service EconomyDocument1 pageEmergence of Service EconomyAditya0% (1)

- Cebu Pacific - Print ItineraryDocument5 pagesCebu Pacific - Print ItineraryPinky Jane PalomiqueNo ratings yet

- Ausfb Credit Card Usage Terms Condition PDFDocument2 pagesAusfb Credit Card Usage Terms Condition PDFSagar GuptaNo ratings yet

- Iesco Online BillDocument1 pageIesco Online BillMaazAliYousufNo ratings yet

- HSBC MM FinalDocument15 pagesHSBC MM FinalRobinsNo ratings yet

- Comfort O. Odoma & CO.: Plot 573 by Livestock House Junction Jabi, Abuja. Tel: 08097579530Document4 pagesComfort O. Odoma & CO.: Plot 573 by Livestock House Junction Jabi, Abuja. Tel: 08097579530Comfort OdomaNo ratings yet

- Strategies adopted in organizations for stability and growthDocument9 pagesStrategies adopted in organizations for stability and growthMd R H ShakibNo ratings yet

- The Asset Allocation Decision: Key Factors for InvestorsDocument28 pagesThe Asset Allocation Decision: Key Factors for InvestorsAbuzafar AbdullahNo ratings yet

- Fin ManDocument7 pagesFin ManLiandra AmorNo ratings yet

- Case Analysis SAMPLEDocument12 pagesCase Analysis SAMPLEStephen TylerNo ratings yet

- Adventare Group & Airport Kinesis Consulting Political and Economic EnvironmentDocument5 pagesAdventare Group & Airport Kinesis Consulting Political and Economic EnvironmentShio WenzanNo ratings yet

- Friday 5 June 2020: EconomicsDocument20 pagesFriday 5 June 2020: EconomicsChloe TsueNo ratings yet

- Invoice 09 223061398Document1 pageInvoice 09 223061398ChadNo ratings yet

- IcmlDocument1 pageIcmlCwsNo ratings yet

- Financial Management: Core Concepts: Fourth EditionDocument22 pagesFinancial Management: Core Concepts: Fourth EditionTyler HaoNo ratings yet

- Paint Industry Analysis - SIMCON BlogDocument10 pagesPaint Industry Analysis - SIMCON BlogVishnu KanthNo ratings yet

- Management Principles Developed by Henri FayolDocument15 pagesManagement Principles Developed by Henri FayolMa Crisel QuibelNo ratings yet

- Treasury stock transactionsDocument2 pagesTreasury stock transactionsFeizhen MaeNo ratings yet

- Modes of Raising Capital From Primary MarketDocument7 pagesModes of Raising Capital From Primary MarketMeet GandhiNo ratings yet

- By Ismat Sabir: Tea IndustryDocument10 pagesBy Ismat Sabir: Tea Industryask4mohsinNo ratings yet

- Risk ManagementDocument22 pagesRisk ManagementPaw AdanNo ratings yet

- Bank Reconciliation ReviewerDocument2 pagesBank Reconciliation Reviewerfred ferrera jrNo ratings yet

- Cash Budgeting Chapter Appendix On December 1 2009Document1 pageCash Budgeting Chapter Appendix On December 1 2009trilocksp SinghNo ratings yet

- UCSP11 Module 10Document17 pagesUCSP11 Module 10Queenie Bhell AtibagosNo ratings yet

- Project Report On Working Capital ManageDocument70 pagesProject Report On Working Capital ManageJanaklal ShahNo ratings yet

- 1 Head Kit SubDocument2 pages1 Head Kit SubAndres BelloNo ratings yet

- SBR SD22 Examiner ReportDocument15 pagesSBR SD22 Examiner Reportjunk2023No ratings yet