You might also like

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Income Tax On IndividualsDocument25 pagesIncome Tax On IndividualsMohammadNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Unit 5 - Inclusions & Exclusions To Bus & Other Sources of IncomeDocument10 pagesUnit 5 - Inclusions & Exclusions To Bus & Other Sources of IncomeJoseph Anthony RomeroNo ratings yet

- Income Tax Rates & ClassificationsDocument216 pagesIncome Tax Rates & ClassificationsalicorpanaoNo ratings yet

- Definition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeDocument13 pagesDefinition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeSKEETER BRITNEY COSTANo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- Chapter 3 Concept of IncomeDocument12 pagesChapter 3 Concept of IncomeGlomarie GonayonNo ratings yet

- Notes On Income TaxationDocument21 pagesNotes On Income TaxationBen Dela Cruz100% (2)

- Review of Financial Statements, Tax Returns & Business IncomeDocument29 pagesReview of Financial Statements, Tax Returns & Business IncomeLia Nicole BungabongNo ratings yet

- Bac03-Chapter 5Document25 pagesBac03-Chapter 5Rea Mariz JordanNo ratings yet

- (Ikaw Yung Employee at Employer) : Tax On Individuals Tax Rates of Purely Self-EmployedDocument5 pages(Ikaw Yung Employee at Employer) : Tax On Individuals Tax Rates of Purely Self-Employedchizz popcornnNo ratings yet

- Taxation On Individuals - ReviewerDocument2 pagesTaxation On Individuals - ReviewerLouiseNo ratings yet

- Guide 15 Taxable and Non Taxable Income3Document9 pagesGuide 15 Taxable and Non Taxable Income3Zubair GhaznaviNo ratings yet

- Inctax Lecture Notes Froup 2 and 6Document27 pagesInctax Lecture Notes Froup 2 and 6KrizahMarieCaballeroNo ratings yet

- NT - Items of Gross Income 0510 - Income TaxDocument7 pagesNT - Items of Gross Income 0510 - Income TaxElizah PorcadoNo ratings yet

- Lesson 5 - Exclusions and Deductions of Income TaxationDocument34 pagesLesson 5 - Exclusions and Deductions of Income TaxationKhu AbenesNo ratings yet

- B - Individual Taxation: PhilippinesDocument4 pagesB - Individual Taxation: PhilippinesJasper Allen B. Barrientos100% (1)

- Income Tax IndividualDocument22 pagesIncome Tax IndividualJohn Oicemen RocaNo ratings yet

- Taxation: DATE: November 10,2018 Presented By: Mr. Florante P. de Leon, Mba, CBDocument35 pagesTaxation: DATE: November 10,2018 Presented By: Mr. Florante P. de Leon, Mba, CBFlorante De LeonNo ratings yet

- Kinds of Income and Income Tax of Individuals: Take NoteDocument7 pagesKinds of Income and Income Tax of Individuals: Take NoteKen RaquinioNo ratings yet

- Income Taxation (Individuals & Corporation) AALDocument51 pagesIncome Taxation (Individuals & Corporation) AALBon Joshua SegismundoNo ratings yet

- Pure Compensation Income Earner.Document6 pagesPure Compensation Income Earner.Daisy Diane TorresNo ratings yet

- Tax exemptions and incentives for minimum wage earners, BMBEs, cooperatives, non-profit entitiesDocument2 pagesTax exemptions and incentives for minimum wage earners, BMBEs, cooperatives, non-profit entitiesdailydoseoflawNo ratings yet

- Acc212 Handout:: Midlands State University Department of AccountingDocument23 pagesAcc212 Handout:: Midlands State University Department of AccountingPhebieon MukwenhaNo ratings yet

- TSU-CBA Tax Deductions GuideDocument6 pagesTSU-CBA Tax Deductions GuideJamaica DavidNo ratings yet

- Amended Bsa Handout For Gross Income Part 1Document40 pagesAmended Bsa Handout For Gross Income Part 1Dianne Lontac100% (1)

- Lecture 1 - Introduction To Income TaxDocument27 pagesLecture 1 - Introduction To Income TaxMimi kupiNo ratings yet

- DeductionsDocument7 pagesDeductionsConcerned CitizenNo ratings yet

- Tax Midterm ReviewerDocument18 pagesTax Midterm ReviewerAyessa GayamoNo ratings yet

- Adzu Tax 01 B Learning Packet 3 Concept of IncomeDocument5 pagesAdzu Tax 01 B Learning Packet 3 Concept of IncomeDanielle JoenNo ratings yet

- TAX1-LagguiRichelle 2Document4 pagesTAX1-LagguiRichelle 2Richelle GraceNo ratings yet

- DeductionsDocument6 pagesDeductionsjerome rodejoNo ratings yet

- IT Module No. 7: Introduction To Regular Income TaxDocument13 pagesIT Module No. 7: Introduction To Regular Income TaxjakeNo ratings yet

- Taxation of Income: Exclusions and InclusionsDocument11 pagesTaxation of Income: Exclusions and Inclusionsmary jhoyNo ratings yet

- Clwtaxn - Lecture Week4Document17 pagesClwtaxn - Lecture Week4Maria Angelika ArcillaNo ratings yet

- Definition of Income Tax: FinanceDocument10 pagesDefinition of Income Tax: FinanceStXvrNo ratings yet

- INCOME TAX BASICSDocument38 pagesINCOME TAX BASICSElson TalotaloNo ratings yet

- Chapter 3 Concept of IncomeDocument6 pagesChapter 3 Concept of IncomeChesca Marie Arenal Peñaranda100% (1)

- Inclusion and Exclusion of Gross IncomeDocument70 pagesInclusion and Exclusion of Gross IncomeEnola HeitsgerNo ratings yet

- Midterm tax deductions guideDocument9 pagesMidterm tax deductions guideThe Second OneNo ratings yet

- Income Tax Principles and Types in the PhilippinesDocument36 pagesIncome Tax Principles and Types in the PhilippinesPascua PeejayNo ratings yet

- Taxation For Professional Services: TopicDocument35 pagesTaxation For Professional Services: TopicLANCENo ratings yet

- REGULAR INCOME TAX: KEY ITEMS AND RULESDocument24 pagesREGULAR INCOME TAX: KEY ITEMS AND RULESAce ReytaNo ratings yet

- Chapter 13 ADocument22 pagesChapter 13 AAdmNo ratings yet

- Regular Income Tax Inclusion RulesDocument33 pagesRegular Income Tax Inclusion RulesAaron BuendiaNo ratings yet

- Allowable Deductions NotesDocument5 pagesAllowable Deductions NotesPaula Mae DacanayNo ratings yet

- MidTerm Lesson Part 1Document34 pagesMidTerm Lesson Part 1ARMAN WAYNE ANGELESNo ratings yet

- L.B and TaxationDocument18 pagesL.B and TaxationHasnain RazaNo ratings yet

- tAX LESSON B .Document10 pagestAX LESSON B .intramuramazingNo ratings yet

- Deductions From Gross Income Lesson 13Document72 pagesDeductions From Gross Income Lesson 13Mikaela SamonteNo ratings yet

- 3 Income Tax ConceptsDocument37 pages3 Income Tax ConceptsRommel Espinocilla Jr.No ratings yet

- Income Tax On Individuals Part 2Document22 pagesIncome Tax On Individuals Part 2mmhNo ratings yet

- FS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoDocument11 pagesFS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoKatring O.No ratings yet

- I. Basic Concepts in Income TaxationDocument79 pagesI. Basic Concepts in Income Taxationcmv mendoza100% (1)

- Gross Incom TaxationDocument32 pagesGross Incom TaxationSummer ClaronNo ratings yet

- Gross Income: Lecture Notes OnDocument2 pagesGross Income: Lecture Notes Onmigueltanfelix149No ratings yet

- Preliminaries Tax'Document14 pagesPreliminaries Tax'J A SoriaNo ratings yet

- Intermediate Accounting ReviewerDocument5 pagesIntermediate Accounting ReviewerJosephine YenNo ratings yet

- Multiplication Missing Multiplier US LetterDocument1 pageMultiplication Missing Multiplier US LettermmhNo ratings yet

- Mustapha, Samrina A. - Final ExamDocument2 pagesMustapha, Samrina A. - Final ExammmhNo ratings yet

- Subtraction Within 100 Worksheet US LetterDocument1 pageSubtraction Within 100 Worksheet US LettermmhNo ratings yet

- Multiplication Single Double Digit Worksheet US LetterDocument1 pageMultiplication Single Double Digit Worksheet US LettermmhNo ratings yet

- Addition Within 100 Worksheet US LetterDocument1 pageAddition Within 100 Worksheet US LettermmhNo ratings yet

- LAWONSALES QUIZ 3 Draft 2Document3 pagesLAWONSALES QUIZ 3 Draft 2mmhNo ratings yet

- Income Tax On Individuals Part 2Document22 pagesIncome Tax On Individuals Part 2mmhNo ratings yet

- Law On Partnership and Corporation by Hector de LeonDocument113 pagesLaw On Partnership and Corporation by Hector de LeonShiela Marie Vics75% (12)

- Law On Partnership and Corporation by Hector de LeonDocument113 pagesLaw On Partnership and Corporation by Hector de LeonShiela Marie Vics75% (12)

- ABS-CBN v. Court of Appeals - No Contract Formed Between ABS-CBN and VIVA; Corporations Cannot Claim Moral DamagesDocument4 pagesABS-CBN v. Court of Appeals - No Contract Formed Between ABS-CBN and VIVA; Corporations Cannot Claim Moral DamagesmmhNo ratings yet

- Law On Partnership and Corporation by Hector de LeonDocument113 pagesLaw On Partnership and Corporation by Hector de LeonShiela Marie Vics75% (12)

- FIL101 Term Paper DraftDocument1 pageFIL101 Term Paper DraftmmhNo ratings yet

- Explaining Key Provisions of the Anti-Money Laundering ActDocument6 pagesExplaining Key Provisions of the Anti-Money Laundering ActmmhNo ratings yet

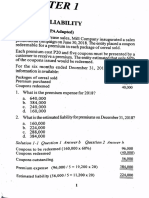

- Calculating Premium Liabilities for Sales PromotionsDocument25 pagesCalculating Premium Liabilities for Sales PromotionskianamarieNo ratings yet

- Module 1 Taxation PrinciplesDocument15 pagesModule 1 Taxation PrinciplesmmhNo ratings yet

- CASE 2 Mambulao Lumber Vs Philippine National BankDocument3 pagesCASE 2 Mambulao Lumber Vs Philippine National BankmmhNo ratings yet

- Calculating Premium Liabilities for Sales PromotionsDocument25 pagesCalculating Premium Liabilities for Sales PromotionskianamarieNo ratings yet

- Intacc EditedDocument61 pagesIntacc EditedKonrad Lorenz Madriaga UychocoNo ratings yet

- CASE 1 Noel Whesseo Inc. Vs Independent Testing ConsultantsDocument6 pagesCASE 1 Noel Whesseo Inc. Vs Independent Testing ConsultantsmmhNo ratings yet

- Calculating Premium Liabilities for Sales PromotionsDocument25 pagesCalculating Premium Liabilities for Sales PromotionskianamarieNo ratings yet

- Note PayableDocument6 pagesNote PayablemmhNo ratings yet

- Module 5 Note Payable and Debt RestructureDocument15 pagesModule 5 Note Payable and Debt Restructuremmh100% (1)

- CASE 2 Mambulao Lumber Vs Philippine National BankDocument3 pagesCASE 2 Mambulao Lumber Vs Philippine National BankmmhNo ratings yet

- Note Payable AccountingDocument8 pagesNote Payable AccountingJane Gavino0% (1)

- Shareholders Equity PDF FreeDocument111 pagesShareholders Equity PDF FreeJoseph Asis100% (1)

- Shareholders Equity PDF FreeDocument111 pagesShareholders Equity PDF FreeJoseph Asis100% (1)

- Note PayableDocument6 pagesNote PayablemmhNo ratings yet

- Shareholders Equity PDF FreeDocument111 pagesShareholders Equity PDF FreeJoseph Asis100% (1)

- Auditing ProblemsDocument7 pagesAuditing ProblemsMelcah Buhi100% (1)

- Tar MRL Company PDFDocument18 pagesTar MRL Company PDFrishi Kr.No ratings yet

- Common Size Analys3esDocument5 pagesCommon Size Analys3esSaw Mee LowNo ratings yet

- Commissioner of Internal Revenue, Petitioner, v. La Flor Dela Isabela, Inc., RespondentDocument9 pagesCommissioner of Internal Revenue, Petitioner, v. La Flor Dela Isabela, Inc., Respondentkristel jane caldozaNo ratings yet

- SampleRF Guidebook C2019 2 PDFDocument174 pagesSampleRF Guidebook C2019 2 PDFJessie XinyingNo ratings yet

- Keventers Financial EstimationDocument4 pagesKeventers Financial EstimationAnirudhNo ratings yet

- Journal FSRUDocument63 pagesJournal FSRUShah Reza Dwiputra100% (1)

- Profit LossDocument8 pagesProfit LossVishnu S. M. YarlagaddaNo ratings yet

- Senior Management Finance Controller in Hoffman Estates IL Resume Todd MajewskiDocument2 pagesSenior Management Finance Controller in Hoffman Estates IL Resume Todd MajewskiToddMajewskiNo ratings yet

- 1992 Rules Regulating The Issuance of Property Dividends PDFDocument2 pages1992 Rules Regulating The Issuance of Property Dividends PDFJerome AzarconNo ratings yet

- OffShore Vessel GlossaryDocument21 pagesOffShore Vessel Glossarydaniel8iosif_178% (9)

- FN1623 2406Document1,036 pagesFN1623 24064207west59thNo ratings yet

- Alpha Portfolio Seeks Superior Stock SelectionDocument2 pagesAlpha Portfolio Seeks Superior Stock SelectionDhirendra PradhanNo ratings yet

- Vertical and Horizontal AnalysisDocument19 pagesVertical and Horizontal Analysissanamehar89% (9)

- 1 Introduction To Accounting Concepts and Structure UDDocument9 pages1 Introduction To Accounting Concepts and Structure UDERICK MLINGWANo ratings yet

- National Textile Corporation Annual ReportDocument186 pagesNational Textile Corporation Annual ReportSimran BohraNo ratings yet

- Albania Apartments in Saranda - Saranda Alba ResidenceDocument9 pagesAlbania Apartments in Saranda - Saranda Alba ResidenceAlbania PropertyNo ratings yet

- PAW Fiction - Tired Old Man (Gary D Ott) - DestinyDocument127 pagesPAW Fiction - Tired Old Man (Gary D Ott) - DestinyBruce ArmstrongNo ratings yet

- 9 Partnership Question 3Document5 pages9 Partnership Question 3kautiNo ratings yet

- 1959 - Gordon Dividends, Earnings, and Stock Prices PDFDocument8 pages1959 - Gordon Dividends, Earnings, and Stock Prices PDFHop LuuNo ratings yet

- Financial Inclusion QuestionnaireDocument6 pagesFinancial Inclusion QuestionnairesheglinalNo ratings yet

- Globalization and StateDocument5 pagesGlobalization and Stateshereen padchongaNo ratings yet

- 15-Mca-Or-Accounting and Financial ManagementDocument4 pages15-Mca-Or-Accounting and Financial ManagementSRINIVASA RAO GANTANo ratings yet

- US Internal Revenue Service: Irb07-40Document48 pagesUS Internal Revenue Service: Irb07-40IRSNo ratings yet

- DLF Annual ReportDocument194 pagesDLF Annual ReportKailash BhandariNo ratings yet

- Cash Flow StatementDocument18 pagesCash Flow StatementBrian Reyes Gangca50% (4)

- AP.2806 Investments PDFDocument6 pagesAP.2806 Investments PDFMay Grethel Joy Perante0% (1)

- Chapter 15 & 17 Q & SDocument7 pagesChapter 15 & 17 Q & Sgabie stgNo ratings yet

- New Business Green GrocerDocument40 pagesNew Business Green Grocernaveed009No ratings yet

- HK DSE 2020 BAFS Paper 1 Section A Multiple-Choice QuestionsDocument21 pagesHK DSE 2020 BAFS Paper 1 Section A Multiple-Choice QuestionswwlNo ratings yet