You might also like

- Partnerships Corporations Partnership Act 1890 Joint and Several Liability Limited LiabilityDocument1 pagePartnerships Corporations Partnership Act 1890 Joint and Several Liability Limited LiabilityMonuNo ratings yet

- Limited Liability Partnership - Wikipedia PDFDocument51 pagesLimited Liability Partnership - Wikipedia PDFNAVAMY MRNo ratings yet

- Difference between LLCs and LLPsDocument7 pagesDifference between LLCs and LLPsAlok MishraNo ratings yet

- LLP Overview: Structure, Registration, Advantages in IndiaDocument4 pagesLLP Overview: Structure, Registration, Advantages in IndiaDeevanshu ShrivastavaNo ratings yet

- LLP Partnership Guide: Structure, Advantages & Key ElementsDocument9 pagesLLP Partnership Guide: Structure, Advantages & Key ElementsAnkita SrivastavaNo ratings yet

- Limited Liability Partnership - RidhiDocument5 pagesLimited Liability Partnership - Ridhivarunendra pandeyNo ratings yet

- Limited Liability Partnership: Anjum TanwarDocument14 pagesLimited Liability Partnership: Anjum TanwarKartik GambhirNo ratings yet

- A Project Report On LLPDocument10 pagesA Project Report On LLPPiyush Saraogi0% (1)

- LLP Final Project by Jashan WarraichDocument28 pagesLLP Final Project by Jashan WarraichJashanNo ratings yet

- LLP or Private Limited CompanyDocument4 pagesLLP or Private Limited CompanyScholarNo ratings yet

- Limited Liability Partnership - RidhiDocument4 pagesLimited Liability Partnership - Ridhivarunendra pandeyNo ratings yet

- Limited Liability PartnershipDocument10 pagesLimited Liability PartnershipPalak GulabaniNo ratings yet

- Unique Id - Topic-Limited Liability Partnership: Balance Between Partnership and CompanyDocument8 pagesUnique Id - Topic-Limited Liability Partnership: Balance Between Partnership and CompanyUTKARSH MISHRANo ratings yet

- Limited Liability PartnershipDocument5 pagesLimited Liability PartnershipABHIJIT MAZUMDERNo ratings yet

- India LLP Taxguru - inDocument7 pagesIndia LLP Taxguru - inJatan HundalNo ratings yet

- LLPARTNERSHIPDocument6 pagesLLPARTNERSHIPAltafMakaiNo ratings yet

- Business Law - Module - IVDocument21 pagesBusiness Law - Module - IVdrashti vaishnavNo ratings yet

- Narsee Monjee Institute OF Management Studies, Bangalore School of Law (Sol)Document9 pagesNarsee Monjee Institute OF Management Studies, Bangalore School of Law (Sol)Saurabh Krishna SinghNo ratings yet

- Limited Liability Partnerships in KenyaDocument5 pagesLimited Liability Partnerships in KenyaStephen Mallowah100% (1)

- Yash Jain Short Assignment 5Document4 pagesYash Jain Short Assignment 5YashJainNo ratings yet

- Business Legal Structures PPT 1Document45 pagesBusiness Legal Structures PPT 1api-316477395No ratings yet

- Your Initial Guide Towards Your Business DreamDocument30 pagesYour Initial Guide Towards Your Business DreamShefali TripathiNo ratings yet

- Companies and PartnershipsDocument24 pagesCompanies and Partnershipsh1kiddNo ratings yet

- Limited Liability Partnership NotesDocument28 pagesLimited Liability Partnership NotesPraveen Kumar DuggalNo ratings yet

- Limited Liability PartnershipDocument3 pagesLimited Liability PartnershipShruti BhatiaNo ratings yet

- Partnerships CorporationsDocument2 pagesPartnerships Corporationsshanmughipriya nagarajanNo ratings yet

- Comparison Partnership and LLPDocument9 pagesComparison Partnership and LLPSiti Nazatul MurnirahNo ratings yet

- THE LIMITED LIABILITY PARTNERSHIP ACTDocument17 pagesTHE LIMITED LIABILITY PARTNERSHIP ACTABINASHNo ratings yet

- Limited Liability Partnership (LLP): Key Features and Comparison (39Document15 pagesLimited Liability Partnership (LLP): Key Features and Comparison (39khalsa computersNo ratings yet

- Law LLP PaperDocument6 pagesLaw LLP PaperGaurav ChopraNo ratings yet

- LLP RegistrationDocument2 pagesLLP RegistrationLopamudracsNo ratings yet

- Meaning and Features of Limited Liability PartnershipDocument57 pagesMeaning and Features of Limited Liability PartnershipManisha RaiNo ratings yet

- LLPDocument24 pagesLLPPrashant MauryaNo ratings yet

- What Is A Business Partnership?Document3 pagesWhat Is A Business Partnership?Skylar FunnelNo ratings yet

- Everything You Need to Know About Forming an LLPDocument4 pagesEverything You Need to Know About Forming an LLPManoj Kumar MannepalliNo ratings yet

- Limited Liability Partnership (LLP) - Advantages and DisadvantagesDocument3 pagesLimited Liability Partnership (LLP) - Advantages and DisadvantagesMyo Kyaw SwarNo ratings yet

- Joint and Several Liability of The Partners. The Traditional Partnerships Are Also ConsideredDocument20 pagesJoint and Several Liability of The Partners. The Traditional Partnerships Are Also ConsideredMukesh RathiNo ratings yet

- Limited Liability Partnership - A Comprehensive CommentaryDocument43 pagesLimited Liability Partnership - A Comprehensive CommentarySoumitra Chawathe0% (1)

- LLP in India GuideDocument5 pagesLLP in India GuideShivam AgarwalNo ratings yet

- Types of Registered CompaniesDocument8 pagesTypes of Registered Companiesvidrascu0% (2)

- LLP Notes As Per DU SyllabusDocument39 pagesLLP Notes As Per DU SyllabusAryan GuptaNo ratings yet

- The Limited Liability Partnership ActDocument10 pagesThe Limited Liability Partnership ActIshwar MeenaNo ratings yet

- CompanyDocument15 pagesCompanykgatoNo ratings yet

- Definition of A Limited Liability PartnershipDocument3 pagesDefinition of A Limited Liability PartnershipHashi MohamedNo ratings yet

- BL ProjectDocument6 pagesBL Projectsarathat7No ratings yet

- LLPs Offer Limited Liability for PartnersDocument5 pagesLLPs Offer Limited Liability for PartnersGiancarlo CobinoNo ratings yet

- Limited Liability PartnershipDocument19 pagesLimited Liability PartnershipKanan JainNo ratings yet

- Solution Manual Business EntitiesDocument34 pagesSolution Manual Business EntitiesKiranNo ratings yet

- Corporate Law (Dba354)Document67 pagesCorporate Law (Dba354)Awini ShadrachNo ratings yet

- What Is A Limited PartnershipDocument9 pagesWhat Is A Limited Partnershipsonali mahajan 833No ratings yet

- Benefits of LLPDocument2 pagesBenefits of LLPSwarup SarkarNo ratings yet

- What Is A Partnership?: Types of Partnership Arrangements Limited LiabilityDocument3 pagesWhat Is A Partnership?: Types of Partnership Arrangements Limited LiabilityBella AyabNo ratings yet

- Limited Liability Partnership Act, 2008: Concept of LLPDocument3 pagesLimited Liability Partnership Act, 2008: Concept of LLPridhi soodNo ratings yet

- Synopsis LLPDocument6 pagesSynopsis LLPnischayn10No ratings yet

- Short Note On LLPDocument3 pagesShort Note On LLPRajeshNo ratings yet

- Characteristics of Ownership in MyanmarDocument2 pagesCharacteristics of Ownership in MyanmarShin ThantNo ratings yet

- Limited Liability Partnership LLP in India and Other CountriesDocument2 pagesLimited Liability Partnership LLP in India and Other CountriesGagan NarangNo ratings yet

- Company Types ExplainedDocument8 pagesCompany Types ExplainedRizwan AhmedNo ratings yet

- Limited Liability Partnership: An Insight: Corporate and Allied LawsDocument5 pagesLimited Liability Partnership: An Insight: Corporate and Allied LawshunkashuNo ratings yet

- The Covid-19 pa-WPS OfficeDocument2 pagesThe Covid-19 pa-WPS OfficeTamanna BajiyaNo ratings yet

- Preamble-WPS OfficeDocument11 pagesPreamble-WPS OfficeTamanna BajiyaNo ratings yet

- Laxmi v. Union-WPS OfficeDocument18 pagesLaxmi v. Union-WPS OfficeTamanna BajiyaNo ratings yet

- School of Law: Women EntrepreneurshipDocument16 pagesSchool of Law: Women EntrepreneurshipTamanna BajiyaNo ratings yet

- School of Law: Women EntrepreneurshipDocument16 pagesSchool of Law: Women EntrepreneurshipTamanna BajiyaNo ratings yet

- BS 8081 File 1Document60 pagesBS 8081 File 1ekaamf100% (1)

- Company Law PDFDocument81 pagesCompany Law PDFYounis Khan50% (2)

- Panel of Transaction AdvisorsDocument3 pagesPanel of Transaction AdvisorsDey LiNo ratings yet

- Room Assignments - Secondary - T.L.E (Pagadian) PDFDocument35 pagesRoom Assignments - Secondary - T.L.E (Pagadian) PDFPhilBoardResultsNo ratings yet

- Physical Therapist Licensure Exam Room AssignmentsDocument24 pagesPhysical Therapist Licensure Exam Room AssignmentsdericNo ratings yet

- Top 100 Companies in PolandDocument3 pagesTop 100 Companies in PolandBaktygul KosimovaNo ratings yet

- BVRIT Hyderabad College of Engineering For Women 2017-21 Batch Placement DetailsDocument2 pagesBVRIT Hyderabad College of Engineering For Women 2017-21 Batch Placement DetailsRajendra KrishnaNo ratings yet

- 3RD Degree Relationship 1.8.15Document2 pages3RD Degree Relationship 1.8.15Adonis BarraquiasNo ratings yet

- IFSC BANK CODES LISTDocument20 pagesIFSC BANK CODES LISTChirag Tanavala100% (1)

- HR DetailDocument2 pagesHR DetailHariprasathNo ratings yet

- Robert E. KernDocument3 pagesRobert E. KernRiverheadLOCALNo ratings yet

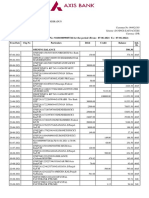

- TUSHAR SHARMA'S AXIS BANK ACCOUNT STATEMENTDocument22 pagesTUSHAR SHARMA'S AXIS BANK ACCOUNT STATEMENTTusharNo ratings yet

- Bank allotment and marks of candidatesDocument157 pagesBank allotment and marks of candidatesSaurabhNo ratings yet

- EON IT Park Kharadi 2015-16Document14 pagesEON IT Park Kharadi 2015-16surajNo ratings yet

- IEC 60947-4-1 Low-Voltage Switch Gear and Control Gear - Cont Actors and Motor Starters - ElectromecDocument188 pagesIEC 60947-4-1 Low-Voltage Switch Gear and Control Gear - Cont Actors and Motor Starters - ElectromecValentin Pal0% (1)

- Legazpi Room Assignment Elementary LETDocument160 pagesLegazpi Room Assignment Elementary LETTheSummitExpress100% (1)

- By Kaushal Pal:: The List of Bins Card These Are Non VBV Cards Bins and BanksDocument13 pagesBy Kaushal Pal:: The List of Bins Card These Are Non VBV Cards Bins and BanksJaveed Ahamed100% (2)

- Fun Game - ReviewDocument6 pagesFun Game - Reviewapi-518386723No ratings yet

- Consignment Daily Sales Report PT. Matahari Department Store TBK by SupplierDocument106 pagesConsignment Daily Sales Report PT. Matahari Department Store TBK by SupplierMaharani Amalia PutriNo ratings yet

- Magnit: Magnit (Магнит, "Magnet") is one of Russia's largest foodDocument6 pagesMagnit: Magnit (Магнит, "Magnet") is one of Russia's largest foodMohamedou Matar SeckNo ratings yet

- S.No Code Bank Name Netbanking Debit Card Aadhaar: Bank Status in API E-MandateDocument2 pagesS.No Code Bank Name Netbanking Debit Card Aadhaar: Bank Status in API E-MandateBhaskarNo ratings yet

- Asme B73-1 PDFDocument52 pagesAsme B73-1 PDFJoan Camilo PovedaNo ratings yet

- Company Law ProjectDocument28 pagesCompany Law ProjectpushpanjaliNo ratings yet

- Asme PTC 1 PDFDocument26 pagesAsme PTC 1 PDFpiziyuNo ratings yet

- Certification: Maria Concepcion V. CanlasDocument117 pagesCertification: Maria Concepcion V. CanlasCarl Yry BitengNo ratings yet

- Classifications of Bank and ExaampleDocument6 pagesClassifications of Bank and ExaampleJosel AposagaNo ratings yet

- Jackson Rising: New Economies Conference International Decade of Cooperatives StatementDocument1 pageJackson Rising: New Economies Conference International Decade of Cooperatives StatementKali AkunoNo ratings yet

- Forms of Business Organisation MCQ Class 11 Business StudiesDocument18 pagesForms of Business Organisation MCQ Class 11 Business StudiesGunjan SabriNo ratings yet

- List of Qualified Bidder For NH-12, Nh-75-E & NH-7)Document7 pagesList of Qualified Bidder For NH-12, Nh-75-E & NH-7)AneeshNo ratings yet

- Syllabus (Course Outline) Cum Lecture Plan Semester - VII Credit: 3Document7 pagesSyllabus (Course Outline) Cum Lecture Plan Semester - VII Credit: 3Mandira PriyaNo ratings yet