You might also like

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Bab 6 Intercompany Profit TransactionsDocument2 pagesBab 6 Intercompany Profit TransactionsAnonymous dMkY9G2No ratings yet

- Advanced Accounting 1Document6 pagesAdvanced Accounting 1Tax TrainingNo ratings yet

- Unrealized Gross ProfitDocument3 pagesUnrealized Gross Profitels emsNo ratings yet

- 2 Template PPT2Document16 pages2 Template PPT2ダイ アンNo ratings yet

- Managerial Accounting Exam CHDocument17 pagesManagerial Accounting Exam CH808kailuaNo ratings yet

- Chap 6.1Document32 pagesChap 6.1Natsu DragneelNo ratings yet

- Chapter 6 - Solution ManualDocument91 pagesChapter 6 - Solution Manualgilli1tr58% (12)

- Consolidated Financial StatementsDocument51 pagesConsolidated Financial Statementscaztinahernandez100% (4)

- Statement of Comprehensive Income (SCI)Document35 pagesStatement of Comprehensive Income (SCI)Jung WonnieNo ratings yet

- Methods of Estimating InventoryDocument46 pagesMethods of Estimating Inventoryone formanyNo ratings yet

- Module 6 Elimination of Unrealized Profit Intercompany Sales of InventoryDocument31 pagesModule 6 Elimination of Unrealized Profit Intercompany Sales of InventoryJulliena BakersNo ratings yet

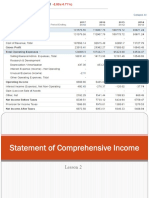

- Lesson 2 Statement of Comprehensive IncomeDocument23 pagesLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Chapter 5 SolutionsDocument21 pagesChapter 5 SolutionsIzu EvansNo ratings yet

- Left Column For Inner Computation - Right Column For Totals - Peso Sign at The Beginning Amount and at Final Answer TwoDocument6 pagesLeft Column For Inner Computation - Right Column For Totals - Peso Sign at The Beginning Amount and at Final Answer Twoamberle smithNo ratings yet

- CMPC 221 Finals Part 1: Mulitple ChoiceDocument7 pagesCMPC 221 Finals Part 1: Mulitple ChoiceIyarna YasraNo ratings yet

- Solution Manual: (Updated Through November 11, 2013)Document55 pagesSolution Manual: (Updated Through November 11, 2013)Jay BrockNo ratings yet

- Intercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupDocument60 pagesIntercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupPhil MO JoeNo ratings yet

- Chapter 5 Advanced AccountingDocument19 pagesChapter 5 Advanced AccountingMarife De Leon VillalonNo ratings yet

- TranscriptionDocument3 pagesTranscriptionCasdingan Bayawa AugieNo ratings yet

- Association of Chartered Certified Accountants: Sales Taxes and InventoryDocument81 pagesAssociation of Chartered Certified Accountants: Sales Taxes and InventoryBetseline IgnatiusNo ratings yet

- For The The Key ActivitiesDocument3 pagesFor The The Key ActivitiesMarie AnneNo ratings yet

- Teaching Note On Financial StatementsDocument36 pagesTeaching Note On Financial StatementsMilton StevensNo ratings yet

- Financial Statement Analysis A Look at The Income SheetDocument4 pagesFinancial Statement Analysis A Look at The Income SheetNajmalinda ZenithaNo ratings yet

- Business Finance FormulaDocument9 pagesBusiness Finance FormulaGeorge Nicole BaybayanNo ratings yet

- Business Finance FormulaDocument9 pagesBusiness Finance FormulaGeorge Nicole BaybayanNo ratings yet

- Day 11 Chap 6 Rev. FI5 Ex PRDocument8 pagesDay 11 Chap 6 Rev. FI5 Ex PRChristian De Leon0% (2)

- Tutorial Solutions5 TheoryDocument1 pageTutorial Solutions5 TheoryEriiNo ratings yet

- FMCG Profit AnalysisDocument8 pagesFMCG Profit AnalysisTarun BhatiaNo ratings yet

- Chapter2 Statement of Comprehensive IncomeDocument46 pagesChapter2 Statement of Comprehensive IncomeRonald De La Rama100% (1)

- Sales VarianceDocument22 pagesSales VarianceTejitu AdebaNo ratings yet

- 676254Document89 pages676254Shofiana IfadaNo ratings yet

- CashflowDocument6 pagesCashflowAizia Sarceda Guzman71% (7)

- Statement of Comprehensive IncomeDocument16 pagesStatement of Comprehensive IncomeDindin Oromedlav Lorica100% (4)

- Intercompany Profit Transactions - Inventories: Answers To Questions 1Document22 pagesIntercompany Profit Transactions - Inventories: Answers To Questions 1NisrinaPArisantyNo ratings yet

- CH 06Document50 pagesCH 06Dr-Bahaaeddin Alareeni100% (1)

- Gross Profit Net Sales - Cost of Goods Sold Operating Income Gross Profit - Operating Expense Net Income Operating Income + Non Operating ItemsDocument8 pagesGross Profit Net Sales - Cost of Goods Sold Operating Income Gross Profit - Operating Expense Net Income Operating Income + Non Operating ItemsIan VinoyaNo ratings yet

- Intercompany Inventory and Land Profits: Solutions Manual, Chapter 6Document40 pagesIntercompany Inventory and Land Profits: Solutions Manual, Chapter 6HelloWorldNowNo ratings yet

- Equity Capital FinancingDocument6 pagesEquity Capital FinancingMirza ShoaibbaigNo ratings yet

- AE24 Lesson 5Document9 pagesAE24 Lesson 5Majoy BantocNo ratings yet

- Chapter 5 Intra Entity TransactionsDocument56 pagesChapter 5 Intra Entity TransactionsTilahun S. KuraNo ratings yet

- Gross Profit Variance AnalysisDocument6 pagesGross Profit Variance AnalysisKatherine DimaunahanNo ratings yet

- Intercompany Inventory Transactions EliminationsDocument77 pagesIntercompany Inventory Transactions EliminationsPeng ChuNo ratings yet

- Task 2: Part B (Annex C) : Statement of Working Capital (FY 2015 and 2016)Document6 pagesTask 2: Part B (Annex C) : Statement of Working Capital (FY 2015 and 2016)nikita pareekNo ratings yet

- Fabm ReviewerDocument2 pagesFabm Reviewer治太宰No ratings yet

- Far 4Document9 pagesFar 4Sonu NayakNo ratings yet

- FABM 2 Module 3 Statement of Comprehensive IncomeDocument10 pagesFABM 2 Module 3 Statement of Comprehensive IncomebabyjamskieNo ratings yet

- Think of Words That Best Describe Revenues. Expenses Statement of Comprehensive IncomeDocument30 pagesThink of Words That Best Describe Revenues. Expenses Statement of Comprehensive IncomeJasy Nupt GilloNo ratings yet

- Difference Between EBIT & EPSDocument3 pagesDifference Between EBIT & EPSPranab MahapatraNo ratings yet

- How To Prepare A Profit and Loss (Income) Statement: Zions Business Resource CenterDocument16 pagesHow To Prepare A Profit and Loss (Income) Statement: Zions Business Resource CenterSiti Asma MohamadNo ratings yet

- EF Chapter 2 - The Income StatementDocument19 pagesEF Chapter 2 - The Income StatementPandi IndraNo ratings yet

- Break Even AnalysisDocument15 pagesBreak Even AnalysisPawan BiswaNo ratings yet

- Profitability AnalysisDocument9 pagesProfitability AnalysisBurhan Al MessiNo ratings yet

- Intercompany Inventory ConsolidationDocument31 pagesIntercompany Inventory ConsolidationIm In Trouble100% (2)

- Gross Profit RatioDocument2 pagesGross Profit RatioShahzad AhmedNo ratings yet

- Jaiib 4rd JuneDocument45 pagesJaiib 4rd JuneDeepesh SrivastavaNo ratings yet

- Stock Investments – Accounting Methods and ReportingDocument9 pagesStock Investments – Accounting Methods and ReportingZachra MeirizaNo ratings yet

- Bahan Ajar Investasi SahamDocument9 pagesBahan Ajar Investasi SahamZachra MeirizaNo ratings yet

- Bahan Ajar KonsolidasiDocument13 pagesBahan Ajar KonsolidasiZachra MeirizaNo ratings yet

- Bahan Ajar Teknik KonsolidasiDocument14 pagesBahan Ajar Teknik KonsolidasiZachra MeirizaNo ratings yet

- Bahan Ajar Penggabungan UsahaDocument6 pagesBahan Ajar Penggabungan UsahaZachra MeirizaNo ratings yet

- Bahan Ajar Penggabungan UsahaDocument6 pagesBahan Ajar Penggabungan UsahaZachra MeirizaNo ratings yet

- Tugas Mandiri Lab. Ak. Meng 1 - PersediaanDocument9 pagesTugas Mandiri Lab. Ak. Meng 1 - PersediaanZachra MeirizaNo ratings yet

- CH 2 - Group Financial StatmentDocument47 pagesCH 2 - Group Financial StatmentWedaje AlemayehuNo ratings yet

- Bab 2 MateriDocument4 pagesBab 2 MateriAndikaNo ratings yet

- Forms of Combinations Chart of Forms of Business: 1. Simple AssociationDocument3 pagesForms of Combinations Chart of Forms of Business: 1. Simple AssociationshabanNo ratings yet

- Fundamentals of Advanced Accounting 8th Edition Hoyle Solutions ManualDocument24 pagesFundamentals of Advanced Accounting 8th Edition Hoyle Solutions ManualJanetSmithonybNo ratings yet

- Advanced Accounting Baker Chapter 4 AnswersDocument58 pagesAdvanced Accounting Baker Chapter 4 AnswersOksana McCord86% (7)

- Intra-Group Adjustments: PreambleDocument3 pagesIntra-Group Adjustments: PreambleErnest NyangiNo ratings yet

- CA Final Financial Reporting Self Study Notes by Ashwani JMLK3HFFDocument46 pagesCA Final Financial Reporting Self Study Notes by Ashwani JMLK3HFFJashwanthNo ratings yet

- Group Accounts Consolidation Questions BankDocument43 pagesGroup Accounts Consolidation Questions BankAli Sheikh93% (14)

- 6534 PDFDocument6 pages6534 PDFPunish Kumar Pandey100% (1)

- Consolidation of Financial StatementsDocument2 pagesConsolidation of Financial StatementsmanojjecrcNo ratings yet

- p4 2Document5 pagesp4 2Ernike SariNo ratings yet

- Latihan - Ch.11Document16 pagesLatihan - Ch.11DiditNo ratings yet

- 2024M&ADocument80 pages2024M&AJingwen YangNo ratings yet

- 1.2 Corporate Accounting PDFDocument6 pages1.2 Corporate Accounting PDFRech MJNo ratings yet

- Chapter 618Document25 pagesChapter 618Pranav GargNo ratings yet

- Inventory Management Study at Asian PaintsDocument101 pagesInventory Management Study at Asian PaintsSumitNo ratings yet

- ACC2001 Lecture 9 Business Combinations IIIDocument46 pagesACC2001 Lecture 9 Business Combinations IIImichael krueseiNo ratings yet

- Chap 001Document41 pagesChap 001ms_cherriesNo ratings yet

- Beams 12ge LN01Document41 pagesBeams 12ge LN01Setia Nurul MNo ratings yet

- Everything You Need to Know About Combinations Under Competition LawDocument23 pagesEverything You Need to Know About Combinations Under Competition LawMishika PanditaNo ratings yet

- MBA Mergers & Acquisitions Lesson PlanDocument3 pagesMBA Mergers & Acquisitions Lesson PlanVaishnavi NvNo ratings yet

- Solution Practice 6 Consolidations 3Document8 pagesSolution Practice 6 Consolidations 3Mya Hmuu KhinNo ratings yet

- Investment Undertakings PDFDocument64 pagesInvestment Undertakings PDFDianneNo ratings yet

- Corporate Restructuring Concepts and Forms SEODocument19 pagesCorporate Restructuring Concepts and Forms SEOAnuska JayswalNo ratings yet

- Corporation Law SyllabusDocument7 pagesCorporation Law SyllabusHuey CalabinesNo ratings yet

- Intercorporate Transfers of Services and Noncurrent Assets: Baker / Lembke / KingDocument98 pagesIntercorporate Transfers of Services and Noncurrent Assets: Baker / Lembke / KingKristiany AmboNo ratings yet

- Advanced Financial Accounting TopicsDocument8 pagesAdvanced Financial Accounting TopicsAndualem ZenebeNo ratings yet

- CONSOLIDATION SummaryDocument5 pagesCONSOLIDATION Summaryjamaica deangNo ratings yet

- Employee Stock Option Agreement Template: How To Use This TemplateDocument11 pagesEmployee Stock Option Agreement Template: How To Use This TemplateZhaye100% (1)

- Bank of Commerce v. RPN DIGESTDocument3 pagesBank of Commerce v. RPN DIGESTkathrynmaydeveza100% (1)