You might also like

- KTKO Final Advanced Managerial Accounting Final ProjectDocument21 pagesKTKO Final Advanced Managerial Accounting Final Projectyasser al khuledyNo ratings yet

- Paper 10newDocument436 pagesPaper 10newaparna100% (1)

- Criteria For Product RationalizationDocument4 pagesCriteria For Product RationalizationAnthony MichailNo ratings yet

- Competitiveness, Strategy, and Productivity: or Distribution Without The Prior Written Consent of Mcgraw-Hill EducationDocument39 pagesCompetitiveness, Strategy, and Productivity: or Distribution Without The Prior Written Consent of Mcgraw-Hill EducationnuggsNo ratings yet

- ch13 - Current LiabilitiesDocument85 pagesch13 - Current LiabilitiesAhmad FauziNo ratings yet

- Solution Manual For Fundamentals of Modern Manufacturing Materials Processes and Systems 7th Edition Mikell P GrooverDocument12 pagesSolution Manual For Fundamentals of Modern Manufacturing Materials Processes and Systems 7th Edition Mikell P GrooverReginald Sanchez100% (35)

- Job Order Costing: Patrick Louie E. Reyes, CTT, Micb, Rca, CpaDocument45 pagesJob Order Costing: Patrick Louie E. Reyes, CTT, Micb, Rca, CpaClaudette Clemente100% (1)

- Law PPR FinalDocument4 pagesLaw PPR FinalMariumm ParusNo ratings yet

- Chapter 2 - Selected AnswersDocument16 pagesChapter 2 - Selected AnswersJohsyutNo ratings yet

- 4 Sem Bcom - Cost AccountingDocument54 pages4 Sem Bcom - Cost Accountingraja chatterjeeNo ratings yet

- Garment CM Cost Estimation Using SAM or SMVDocument2 pagesGarment CM Cost Estimation Using SAM or SMVkbalabala100% (3)

- HE - LOCALGUIDING - GR12 - Q1 - MODULE 7 For TeacherDocument18 pagesHE - LOCALGUIDING - GR12 - Q1 - MODULE 7 For TeacherNhatz Gallosa MarticioNo ratings yet

- Valuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitDocument41 pagesValuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitArundhati SinhaNo ratings yet

- Business Plan, BurgerDocument117 pagesBusiness Plan, Burgermarklogan87% (15)

- Goal ProgrammingDocument52 pagesGoal Programmingvineeth kumarNo ratings yet

- Assignment 4 Job Order Costing - ACTG321 - Cost Accounting and Cost ManagementDocument3 pagesAssignment 4 Job Order Costing - ACTG321 - Cost Accounting and Cost ManagementGenithon PanisalesNo ratings yet

- Prelim Quiz ProdmanDocument4 pagesPrelim Quiz ProdmanJoyce Ann CahusayNo ratings yet

- Managerial EconomicsDocument3 pagesManagerial EconomicsbeaNo ratings yet

- SemiDocument5 pagesSemiBobbie LittleNo ratings yet

- Final Term Paper Managerial Economics 2019Document10 pagesFinal Term Paper Managerial Economics 2019Andleeb AKhtarNo ratings yet

- Management Accounting Notes1Document170 pagesManagement Accounting Notes1Anish Gambhir100% (1)

- Selected Ratios For Three Different Companies That Operate inDocument1 pageSelected Ratios For Three Different Companies That Operate indhanya1995No ratings yet

- Linear ProgrammingDocument27 pagesLinear ProgrammingBerkshire Hathway cold100% (1)

- 02 Quiz 1Document1 page02 Quiz 1Xu XuNo ratings yet

- Quiz 3 CADocument30 pagesQuiz 3 CAbasilnaeem7No ratings yet

- Question 2: Ias 19 Employee Benefits: Page 1 of 2Document2 pagesQuestion 2: Ias 19 Employee Benefits: Page 1 of 2paul sagudaNo ratings yet

- An Introduction To Cost Terms and PurposesDocument17 pagesAn Introduction To Cost Terms and PurposesAmit DeyNo ratings yet

- Topic 5. The Basics of Capital BudgetingDocument10 pagesTopic 5. The Basics of Capital BudgetingCerf VintNo ratings yet

- EconomicsDocument7 pagesEconomicsDua FatimaNo ratings yet

- Marginal AbsorptionDocument4 pagesMarginal Absorptionbalachmalik100% (1)

- Relative Valuations FINALDocument44 pagesRelative Valuations FINALChinmay ShirsatNo ratings yet

- Absorption CostingDocument34 pagesAbsorption Costinggaurav pandeyNo ratings yet

- Emmanuel Santos - OJTDocument11 pagesEmmanuel Santos - OJTIan Conan JuanicoNo ratings yet

- Marginal & Absorption CostingDocument26 pagesMarginal & Absorption CostingPrachi VaishNo ratings yet

- Chapter 7 Supplement 1Document20 pagesChapter 7 Supplement 1Anbang XiaoNo ratings yet

- Wallace Garden SupplyDocument4 pagesWallace Garden SupplyestoniloannNo ratings yet

- Session 12 - The Transportation ModelDocument46 pagesSession 12 - The Transportation ModelNicolás SilvaNo ratings yet

- 11 Solutions PDFDocument9 pages11 Solutions PDFKenneth KibataNo ratings yet

- Chapter 7 (An Introduction To Portfolio Management)Document28 pagesChapter 7 (An Introduction To Portfolio Management)Abuzafar AbdullahNo ratings yet

- Chapter 13 Income Taxes of PartnershipsDocument2 pagesChapter 13 Income Taxes of PartnershipsMike Rajas33% (6)

- 2 Pay Off TableDocument2 pages2 Pay Off TableIanNo ratings yet

- Assignment Chapter 11Document9 pagesAssignment Chapter 11Ibrahim AbdallahNo ratings yet

- Eonomics Questions That May Be On A Business ExamDocument8 pagesEonomics Questions That May Be On A Business ExamVic Burrack100% (1)

- Chapter Two Relevant Information and Decision Making: 5.1 The Role of Accounting in Special DecisionsDocument11 pagesChapter Two Relevant Information and Decision Making: 5.1 The Role of Accounting in Special DecisionsshimelisNo ratings yet

- Capital Budgeting Cash Flows1Document37 pagesCapital Budgeting Cash Flows1Mofdy MinaNo ratings yet

- Intermediate Accounting 2Document88 pagesIntermediate Accounting 2Mj ArbisonNo ratings yet

- Ugrd-Ite6301 Technopreneurship Midterm ExamDocument28 pagesUgrd-Ite6301 Technopreneurship Midterm Exampatricia geminaNo ratings yet

- 4587 2261 10 1487 54 BudgetingDocument46 pages4587 2261 10 1487 54 BudgetingDolly BadlaniNo ratings yet

- Better Business, 2e (Solomon) Chapter 6 Forms of Business OwnershipDocument40 pagesBetter Business, 2e (Solomon) Chapter 6 Forms of Business OwnershipAngelita Dela cruzNo ratings yet

- Chapter 4 - IbfDocument23 pagesChapter 4 - IbfMuhib NoharioNo ratings yet

- The Electronic AgeDocument3 pagesThe Electronic AgeMitchang ValdeviezoNo ratings yet

- Chapter 26 - Review QuestionsDocument7 pagesChapter 26 - Review QuestionsAli MohamedNo ratings yet

- Product Market StakeholdersDocument3 pagesProduct Market Stakeholdersqaqapataqa100% (1)

- Receivable Management KanchanDocument12 pagesReceivable Management KanchanSanchita NaikNo ratings yet

- Agan Interior Design - ExerciseDocument2 pagesAgan Interior Design - ExerciseLouieNo ratings yet

- Chapter # 8 Exercise & Problems - AnswersDocument8 pagesChapter # 8 Exercise & Problems - AnswersZia UddinNo ratings yet

- Operation Management Model ExamDocument4 pagesOperation Management Model ExamBedri M AhmeduNo ratings yet

- Financial Statement AnalysisDocument2 pagesFinancial Statement AnalysisAsad RehmanNo ratings yet

- Tantan EME311 (FT)Document2 pagesTantan EME311 (FT)John stephen InteNo ratings yet

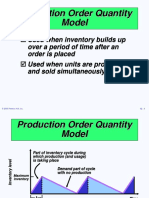

- Production Order Quantity Model: Used When Inventory Builds UpDocument7 pagesProduction Order Quantity Model: Used When Inventory Builds UpANKITA LUTHRA EPGDIB 2018-20No ratings yet

- Coefficient of Variation : Standard Deviation Expected EPSDocument2 pagesCoefficient of Variation : Standard Deviation Expected EPSJPNo ratings yet

- Review Questions and ProblemsDocument4 pagesReview Questions and ProblemsIsha LarionNo ratings yet

- Time Box 1 Box 2 Box 3 Box 4 Sample Means Sample RangeDocument7 pagesTime Box 1 Box 2 Box 3 Box 4 Sample Means Sample RangevrankNo ratings yet

- Marjon Limot & Jose Araneta Jr. December 09, 2020 Bsba-3B MWF (6:00PM-7:00PM) CBM130: Strategic Management Prof: Maam Teoxon Paired ActivityDocument3 pagesMarjon Limot & Jose Araneta Jr. December 09, 2020 Bsba-3B MWF (6:00PM-7:00PM) CBM130: Strategic Management Prof: Maam Teoxon Paired ActivityMarjonNo ratings yet

- Aveeno Booklet FinalDocument16 pagesAveeno Booklet FinalClaire Hacker0% (1)

- Unit Costing and Job CostingDocument3 pagesUnit Costing and Job Costinglevix hyuniNo ratings yet

- BM1805 Marginal Costing and Absorption CostingDocument4 pagesBM1805 Marginal Costing and Absorption CostingMaria Anndrea MendozaNo ratings yet

- Cost & ProductionDocument56 pagesCost & Productionraghavendra_20835414No ratings yet

- Production and CostsDocument110 pagesProduction and CostsramandeepkaurNo ratings yet

- BM1805 Cost-Volume-Profit and Break-Even AnalysisDocument4 pagesBM1805 Cost-Volume-Profit and Break-Even AnalysisMaria Anndrea MendozaNo ratings yet

- Price Theory: BM1805 Pricing Theories and StrategiesDocument5 pagesPrice Theory: BM1805 Pricing Theories and StrategiesMaria Anndrea MendozaNo ratings yet

- Compre Geas Eval 1Document11 pagesCompre Geas Eval 1Maria Anndrea MendozaNo ratings yet

- BM1805 Marginal Costing and Absorption CostingDocument4 pagesBM1805 Marginal Costing and Absorption CostingMaria Anndrea MendozaNo ratings yet

- BM1805 Service Costing and Retail Inventory MethodDocument5 pagesBM1805 Service Costing and Retail Inventory MethodMaria Anndrea MendozaNo ratings yet

- BM1805 Marginal Costing and Absorption CostingDocument4 pagesBM1805 Marginal Costing and Absorption CostingMaria Anndrea MendozaNo ratings yet

- Batangas State University: College of Engineering, Architecture, Fine Arts & Computing SciencesDocument2 pagesBatangas State University: College of Engineering, Architecture, Fine Arts & Computing SciencesMaria Anndrea MendozaNo ratings yet

- Compre Est 2016 (Done B)Document11 pagesCompre Est 2016 (Done B)Maria Anndrea MendozaNo ratings yet

- Generation in C#: MIS 21 - Introduction To Applications DevelopmentDocument16 pagesGeneration in C#: MIS 21 - Introduction To Applications DevelopmentMaria Anndrea MendozaNo ratings yet

- Compre Est 2016Document11 pagesCompre Est 2016Maria Anndrea MendozaNo ratings yet

- Mysql: MIS 21 - Introduction To Applications DevelopmentDocument11 pagesMysql: MIS 21 - Introduction To Applications DevelopmentMaria Anndrea MendozaNo ratings yet

- C# and Mysql: Mis 21 - Introduction To Applications DevelopmentDocument21 pagesC# and Mysql: Mis 21 - Introduction To Applications DevelopmentMaria Anndrea MendozaNo ratings yet

- Calculator Technique For Solving Volume Flow Rate Problems in CalculusDocument3 pagesCalculator Technique For Solving Volume Flow Rate Problems in CalculusMaria Anndrea MendozaNo ratings yet

- Lecture 08-Gauss-EleminationDocument55 pagesLecture 08-Gauss-EleminationMaria Anndrea MendozaNo ratings yet

- Product Specifications Product Specifications: 264SE 264SEDocument2 pagesProduct Specifications Product Specifications: 264SE 264SEMaria Anndrea MendozaNo ratings yet

- Truncation Errors and Taylor Series: Numerical Methods ECE 453Document21 pagesTruncation Errors and Taylor Series: Numerical Methods ECE 453Maria Anndrea MendozaNo ratings yet

- Least Square Regression: Numerical Methods ECE 410Document44 pagesLeast Square Regression: Numerical Methods ECE 410Maria Anndrea MendozaNo ratings yet

- 10-C# Forms InteractionDocument22 pages10-C# Forms InteractionMaria Anndrea MendozaNo ratings yet

- Repeat Rate No .Repeated Films Total No - of Films X 100 %Document41 pagesRepeat Rate No .Repeated Films Total No - of Films X 100 %Maria Anndrea MendozaNo ratings yet

- GEAS Compile Part2Document4 pagesGEAS Compile Part2Maria Anndrea MendozaNo ratings yet

- plk118 1 SusSubstrateDiplexersDocument1 pageplk118 1 SusSubstrateDiplexersMaria Anndrea MendozaNo ratings yet

- CMAC Section A, B Mid-Term Q.PaperDocument5 pagesCMAC Section A, B Mid-Term Q.PaperWaseim khan Barik zaiNo ratings yet

- Standard Costing and Flexible Budget 10Document5 pagesStandard Costing and Flexible Budget 10Lhorene Hope DueñasNo ratings yet

- CH 07Document39 pagesCH 07Shahnawaz KhanNo ratings yet

- Incremental Analysis - WileyDocument57 pagesIncremental Analysis - WileyLeojelaineIgcoyNo ratings yet

- Manacc Assignment 14-3: Make or Buy A ComponentDocument7 pagesManacc Assignment 14-3: Make or Buy A ComponentCuster CoNo ratings yet

- Gibrannudin Effendi - Lambeth Case Managerial AccountingDocument5 pagesGibrannudin Effendi - Lambeth Case Managerial AccountingGibrannudin Effendi AlRasyidNo ratings yet

- Skema PSPM 17-18 Aa025Document4 pagesSkema PSPM 17-18 Aa025Dehey KNo ratings yet

- Internals II - Managerial Accounting Question PaperDocument3 pagesInternals II - Managerial Accounting Question PaperasdeNo ratings yet

- Stratford Corporation Is A Diversified Company Whose Products ArDocument2 pagesStratford Corporation Is A Diversified Company Whose Products ArAmit PandeyNo ratings yet

- F2-11 Alternative Costing PrinciplesDocument20 pagesF2-11 Alternative Costing PrinciplesJaved ImranNo ratings yet

- Chapter 06 - Question SolutionsDocument13 pagesChapter 06 - Question SolutionsxxxNo ratings yet

- Relevant CostingDocument7 pagesRelevant CostingVassy EsperatNo ratings yet

- Cost Accounting - Job Process Costing Flashcards - QuizletDocument56 pagesCost Accounting - Job Process Costing Flashcards - QuizletReicci Lisette JumalonNo ratings yet

- Cost Accounting: Ex 2-7 Statement of Cost of Goods ManufacturedDocument8 pagesCost Accounting: Ex 2-7 Statement of Cost of Goods Manufacturedatiq76No ratings yet

- (A) Implementation of ABCDocument4 pages(A) Implementation of ABCMalik Asim AzizNo ratings yet

- M11-Chp-06-5-Prb-Direct-Costing. Page 1 of 2Document2 pagesM11-Chp-06-5-Prb-Direct-Costing. Page 1 of 2ALLIA LOPEZNo ratings yet

- Annexure - Cost AccountingDocument14 pagesAnnexure - Cost AccountingAndrea AgliettiNo ratings yet

- Overhead Variance: CP 202 (A) - Unit VDocument4 pagesOverhead Variance: CP 202 (A) - Unit VKumardeep SinghaNo ratings yet

- Solution Cost AccountingDocument3 pagesSolution Cost AccountingHaris KhanNo ratings yet

- MAS-42E (Budgeting With Probability Analysis)Document10 pagesMAS-42E (Budgeting With Probability Analysis)Fella GultianoNo ratings yet

- Cost Accounting Quiz No 1docx PDF FreeDocument5 pagesCost Accounting Quiz No 1docx PDF FreeDeryl GalveNo ratings yet