You might also like

- Financial Accounting and Reporting 1Document11 pagesFinancial Accounting and Reporting 1BablooNo ratings yet

- IAS 16 PracticeDocument3 pagesIAS 16 PracticeWaqas Younas Bandukda0% (1)

- Cost Attemptwise PPDocument317 pagesCost Attemptwise PPHassnain SardarNo ratings yet

- Specific Financial Reporting Ac413 MAY2016Document5 pagesSpecific Financial Reporting Ac413 MAY2016AnishahNo ratings yet

- Assignment 5 4.2Document1 pageAssignment 5 4.2ehte19797177No ratings yet

- Taxation Practice: Dunhinda (PVT) Ltd. Was Incorporated On 01Document8 pagesTaxation Practice: Dunhinda (PVT) Ltd. Was Incorporated On 01Muhazzam MaazNo ratings yet

- The Institute of Chartered Accountants of PakistanDocument4 pagesThe Institute of Chartered Accountants of PakistanShehrozSTNo ratings yet

- Mock Test QuestionsDocument36 pagesMock Test QuestionsKish VNo ratings yet

- Ias16 Q3Document2 pagesIas16 Q3ziamz219No ratings yet

- Lecture 11-11Document2 pagesLecture 11-11Nouman ShamasNo ratings yet

- Cost Accounting: T I C A PDocument6 pagesCost Accounting: T I C A PShehrozSTNo ratings yet

- MAY 2016 SkillsDocument188 pagesMAY 2016 SkillsOnaderu Oluwagbenga EnochNo ratings yet

- Q06A Audit of Non Cash AssetsDocument7 pagesQ06A Audit of Non Cash AssetsChristine Jane ParroNo ratings yet

- CAF-3 CMAModelpaperDocument5 pagesCAF-3 CMAModelpaperAsad ZahidNo ratings yet

- CafDocument5 pagesCaftokeeer100% (1)

- Jun Zen Ralph V. Yap BSA - 3 Year Let's CheckDocument5 pagesJun Zen Ralph V. Yap BSA - 3 Year Let's CheckJunzen Ralph YapNo ratings yet

- Live: Exam Questions (Asset Disposal) 12 November 2014 Lesson DescriptionDocument5 pagesLive: Exam Questions (Asset Disposal) 12 November 2014 Lesson DescriptionsandiekaysNo ratings yet

- Group Assignment On FSDocument4 pagesGroup Assignment On FSHuyền TrangNo ratings yet

- Accountancy Auditing 2021Document5 pagesAccountancy Auditing 2021Abdul basitNo ratings yet

- OSA Question - Cost AccountingDocument9 pagesOSA Question - Cost AccountingMohola Tebello GriffithNo ratings yet

- Caf 5 Far-IDocument5 pagesCaf 5 Far-IYahyaNo ratings yet

- As 10Document8 pagesAs 10krithika vasanNo ratings yet

- Laboratory Activity #5 Depreciation: ITEC 30 Accounting Information SystemDocument2 pagesLaboratory Activity #5 Depreciation: ITEC 30 Accounting Information SystemSohfia Jesse VergaraNo ratings yet

- Exercise IAS 16Document1 pageExercise IAS 16robertallie73No ratings yet

- CHP 2. Contract Costing SumsDocument59 pagesCHP 2. Contract Costing SumsUchit MehtaNo ratings yet

- CAF-07 FAR-II Q. Paper (Final)Document5 pagesCAF-07 FAR-II Q. Paper (Final)ANo ratings yet

- Cma Past PapersDocument437 pagesCma Past PapersTooba MaqboolNo ratings yet

- Form 6 Accounts (C)Document8 pagesForm 6 Accounts (C)David MutandaNo ratings yet

- Chapter 6Document40 pagesChapter 6vukicevic.ivan5No ratings yet

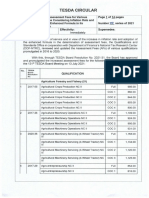

- TESDA Circular No. 072-2021, Mecha, TM EtcDocument14 pagesTESDA Circular No. 072-2021, Mecha, TM EtcAldwin Olivo100% (1)

- QQAA GREEN TECH Comprehensive ExampleDocument7 pagesQQAA GREEN TECH Comprehensive ExampleZulhelmy NazriNo ratings yet

- 2018 Accounts Paper PracticalDocument5 pages2018 Accounts Paper PracticalHmingsangliana HauhnarNo ratings yet

- Practice Question (Accounting Cycle) With Solution v2Document17 pagesPractice Question (Accounting Cycle) With Solution v2Laiba ManzoorNo ratings yet

- Cost Accounting: T I C A PDocument4 pagesCost Accounting: T I C A PShehrozSTNo ratings yet

- Unit 7 Audit of Property Plant and Equipment Handout Final t21516Document10 pagesUnit 7 Audit of Property Plant and Equipment Handout Final t21516Mikaella BengcoNo ratings yet

- Unit 7 Audit of Property Plant and Equipment Handout Final t21516Document10 pagesUnit 7 Audit of Property Plant and Equipment Handout Final t21516Mikaella BengcoNo ratings yet

- Question-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Document6 pagesQuestion-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Letsah BrightNo ratings yet

- Q2Document2 pagesQ2Wathz NawarathnaNo ratings yet

- Diy-Problems (Questionnaire)Document10 pagesDiy-Problems (Questionnaire)May RamosNo ratings yet

- FFA MockDocument4 pagesFFA MockGeeta LalwaniNo ratings yet

- PPE NotesDocument4 pagesPPE Notesaldric taclanNo ratings yet

- As GR 1 Ipcc Compiler 2015-18Document24 pagesAs GR 1 Ipcc Compiler 2015-18KRISHNA MANDLOINo ratings yet

- 2.manufacturing Accounts IllustrationDocument2 pages2.manufacturing Accounts Illustrationdaniel.maina2005No ratings yet

- Test Series: March, 2022 Mock Test Paper - 1 Intermediate: Group - I Paper - 3: Cost and Management AccountingDocument7 pagesTest Series: March, 2022 Mock Test Paper - 1 Intermediate: Group - I Paper - 3: Cost and Management AccountingMusic WorldNo ratings yet

- Lecture 3 - Practice QuestionDocument6 pagesLecture 3 - Practice QuestionBhunesh KumarNo ratings yet

- Group AssignmentDocument12 pagesGroup AssignmentAn Phan Thị HoàiNo ratings yet

- Unit and Output Costing QuestionDocument14 pagesUnit and Output Costing QuestionSilver TricksNo ratings yet

- 5BAP5D03 PPEforprintingDocument8 pages5BAP5D03 PPEforprintingCykee Hanna Quizo LumongsodNo ratings yet

- ND 10 To ND 14Document164 pagesND 10 To ND 14Abdullah al MahmudNo ratings yet

- Acco 30053 - Audit of Ppe - MarpDocument10 pagesAcco 30053 - Audit of Ppe - MarpBanna SplitNo ratings yet

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelAnonymous OtUvYI4No ratings yet

- Chapter 1-Job and Batch Costing: Ref: Cost & Management Accounting by K.S.AdigaDocument14 pagesChapter 1-Job and Batch Costing: Ref: Cost & Management Accounting by K.S.AdigaAR Ananth Rohith BhatNo ratings yet

- 11.11.2017 Audit of PPEDocument9 pages11.11.2017 Audit of PPEPatOcampoNo ratings yet

- BU5504BU5501Document4 pagesBU5504BU5501abinaya590455No ratings yet

- Exercises Ppe PDFDocument6 pagesExercises Ppe PDFمعن الفاعوري100% (1)

- Midterm 5101Document4 pagesMidterm 5101MD Hafizul Islam HafizNo ratings yet

- Acc3201 (F) Aug2014Document5 pagesAcc3201 (F) Aug2014natlyhNo ratings yet

- Number 4Document5 pagesNumber 4Marie Fe GullesNo ratings yet

- June 2021Document64 pagesJune 2021new yearNo ratings yet

- PM Quiz 1Document7 pagesPM Quiz 1Daniyal NasirNo ratings yet

- CIX Pilot Auction Press ReleaseDocument5 pagesCIX Pilot Auction Press ReleaseJNo ratings yet

- CPMI - Cross Border PaymentsDocument60 pagesCPMI - Cross Border PaymentsTarik IrrouNo ratings yet

- Caf 6 Tax Autumn 2015Document4 pagesCaf 6 Tax Autumn 2015ملک محمد کاشف شہزاد اعوانNo ratings yet

- Introduction To Public IssueDocument15 pagesIntroduction To Public IssuePappu ChoudharyNo ratings yet

- Test Bank For Global Business 3rd Edition PengDocument11 pagesTest Bank For Global Business 3rd Edition Pengamplywidenessbwjf100% (47)

- Financial Crises: Lessons From The Past, Preparation For The FutureDocument298 pagesFinancial Crises: Lessons From The Past, Preparation For The FutureJayeshNo ratings yet

- Liquidity GapsDocument18 pagesLiquidity Gapsjessicashergill100% (1)

- How To Read Your Account Analysis StatementDocument2 pagesHow To Read Your Account Analysis StatementhanhNo ratings yet

- Case 3 - 1: Maynard Company (B) : DR Ashish Varma / IMTDocument4 pagesCase 3 - 1: Maynard Company (B) : DR Ashish Varma / IMTkunalNo ratings yet

- Frutybox S.A.: Week # 45 Commercial Invoice No. 001-001-0003012Document1 pageFrutybox S.A.: Week # 45 Commercial Invoice No. 001-001-0003012danielNo ratings yet

- 11 7110 22 FP Webonly AfpDocument89 pages11 7110 22 FP Webonly AfpAminaarshadwarriachNo ratings yet

- Acknowledgement: Mr. Rahul Shah For His Exemplary Guidance, Monitoring and Constant EncouragementDocument42 pagesAcknowledgement: Mr. Rahul Shah For His Exemplary Guidance, Monitoring and Constant EncouragementVineeth MudaliyarNo ratings yet

- Fas 141 R PDFDocument2 pagesFas 141 R PDFToniaNo ratings yet

- MM 314 Engineering Economy - 2. Interest Rate and Economic EquivalenceDocument61 pagesMM 314 Engineering Economy - 2. Interest Rate and Economic EquivalenceOğulcan AytaçNo ratings yet

- Chapter 18 - Equity Valuation ModelsDocument44 pagesChapter 18 - Equity Valuation ModelsQingXu1986No ratings yet

- SEx 2Document20 pagesSEx 2Amir Madani100% (3)

- Rent Receipt Generator Online - House Rent ReceiptDocument5 pagesRent Receipt Generator Online - House Rent ReceiptManish GhadgeNo ratings yet

- RR 2-98 (As Amended)Document74 pagesRR 2-98 (As Amended)Mariano RentomesNo ratings yet

- Orchids The International SchoolDocument1 pageOrchids The International SchoolPrafulla Kailash TajaneNo ratings yet

- Week 2 - Fabm 1 - Accounting Cycle of A Merchandising BusinessDocument19 pagesWeek 2 - Fabm 1 - Accounting Cycle of A Merchandising BusinessSheila Marie Ann Magcalas-GaluraNo ratings yet

- 1-4e Income Taxes: Formula For Federal Income Tax On IndividualsDocument3 pages1-4e Income Taxes: Formula For Federal Income Tax On IndividualsMeriton KrivcaNo ratings yet

- Ea2 TaxationDocument3 pagesEa2 TaxationBlythe teckNo ratings yet

- Case Study - LBO Tata Tea and TetleyDocument4 pagesCase Study - LBO Tata Tea and TetleySumit RathiNo ratings yet

- Tradewinds Corporation BHDDocument10 pagesTradewinds Corporation BHDkhldHANo ratings yet

- Export Document Covering LetterDocument4 pagesExport Document Covering Lettertechindia2010No ratings yet

- Credit Line AgreementDocument14 pagesCredit Line AgreementAdriana MendozaNo ratings yet

- IAS 8 - How To Account For Artwork Under IFRSDocument5 pagesIAS 8 - How To Account For Artwork Under IFRSMuhammad Moin khanNo ratings yet

- Tyler Tysdal September 2019 Securities and Exchange Commission OrderDocument15 pagesTyler Tysdal September 2019 Securities and Exchange Commission OrderMichael_Roberts2019No ratings yet

- Class Slides - Chapter 7Document54 pagesClass Slides - Chapter 7rav kundiNo ratings yet