You might also like

- Co-Ownership, Estate and TrustDocument6 pagesCo-Ownership, Estate and TrustRyan Christian Balanquit100% (2)

- Annexure-1 To Purchase Order CAPEX TOOLING Tools, Jigs & Fixtures ("Tooling") Owned by Ozone Overseas Tooling Cost For DevelopmentDocument3 pagesAnnexure-1 To Purchase Order CAPEX TOOLING Tools, Jigs & Fixtures ("Tooling") Owned by Ozone Overseas Tooling Cost For DevelopmentSanjay KumarNo ratings yet

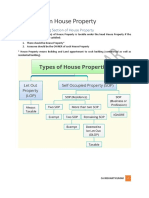

- Income From House PropertyDocument8 pagesIncome From House PropertyVineet KumarNo ratings yet

- EXTRA JUDICIAL SUCCESSION SampleDocument2 pagesEXTRA JUDICIAL SUCCESSION SampleJui ProvidoNo ratings yet

- Heirs of Sarili Vs LagrosaDocument2 pagesHeirs of Sarili Vs LagrosaAshreabai Kam Sinarimbo100% (1)

- Jurisprudence On Quieting of Title and ReconveyanceDocument7 pagesJurisprudence On Quieting of Title and ReconveyancePhilip AmelingNo ratings yet

- PFR Examples Art. 15-41Document10 pagesPFR Examples Art. 15-41Tom HerreraNo ratings yet

- Position of Guarantor Under Sarfaesi ActDocument13 pagesPosition of Guarantor Under Sarfaesi ActAASHISH GUPTA100% (1)

- Pecson Vs CADocument2 pagesPecson Vs CAErika Angela Galceran100% (1)

- Chapter - 8 - TAXDocument11 pagesChapter - 8 - TAXAshek AHmedNo ratings yet

- House Property TaxationDocument13 pagesHouse Property TaxationAnupam BaliNo ratings yet

- Tax ProjectDocument40 pagesTax ProjectGunaNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House PropertyKamini PawarNo ratings yet

- Chapter 5Document9 pagesChapter 5CA Mohit SharmaNo ratings yet

- Income Tax Question BankDocument8 pagesIncome Tax Question Banksurya.notes19No ratings yet

- Income Under The Head House PropertyDocument17 pagesIncome Under The Head House PropertystudywagishaNo ratings yet

- Tax HandoutDocument6 pagesTax Handoutshekharsuhani5No ratings yet

- House PropertyDocument33 pagesHouse PropertypriyaNo ratings yet

- Income Tax ActDocument9 pagesIncome Tax Actbishtrohan064No ratings yet

- Income From House PropertyDocument27 pagesIncome From House PropertyPARTH NAIKNo ratings yet

- Income From House Property: Prepared By: Vaishali NaroliaDocument15 pagesIncome From House Property: Prepared By: Vaishali NaroliaROYNo ratings yet

- CHP 3Document23 pagesCHP 3Laiba SadafNo ratings yet

- Session 11-12 Income From House PropertyDocument7 pagesSession 11-12 Income From House PropertyNoob GamerNo ratings yet

- Kajal Goud 5 Sybbi Income TaxDocument8 pagesKajal Goud 5 Sybbi Income TaxKajal GoudNo ratings yet

- Income Tax LawsDocument47 pagesIncome Tax LawsBhaskar MajumderNo ratings yet

- Ection 24 of The Income Tax ActDocument8 pagesEction 24 of The Income Tax Actdinesh babuNo ratings yet

- Income From HP - March, 2023Document5 pagesIncome From HP - March, 2023Ayush BholeNo ratings yet

- Kartik Black BookDocument3 pagesKartik Black Bookhemant jainNo ratings yet

- Assignment On Income From House PropertyDocument17 pagesAssignment On Income From House PropertySandeep ChawdaNo ratings yet

- Wealth Tax Flow ChartDocument3 pagesWealth Tax Flow ChartParasuram IyerNo ratings yet

- Chapter 7, 8, 12Document41 pagesChapter 7, 8, 12assadrafaqNo ratings yet

- Income From House PropertyDocument5 pagesIncome From House PropertyParas SinghNo ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument31 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaBharath SimhaReddyNaiduNo ratings yet

- U1.3 Introduction To Income Taxation 2 U1.4 Tax Accounting MethodsDocument17 pagesU1.3 Introduction To Income Taxation 2 U1.4 Tax Accounting Methodsfrancis dungcaNo ratings yet

- Income From House PropertyDocument9 pagesIncome From House PropertyArpit LilaNo ratings yet

- House PropertyDocument18 pagesHouse PropertyNidhi LathNo ratings yet

- Income From House Property - Income Tax Deductions On Home Loans & PropertyDocument13 pagesIncome From House Property - Income Tax Deductions On Home Loans & Propertyrajesh_bNo ratings yet

- Income From House PropertyDocument74 pagesIncome From House PropertyHarshit YNo ratings yet

- VND Openxmlformats-Officedocument WordprocessingmlDocument25 pagesVND Openxmlformats-Officedocument WordprocessingmlHimanshu RajputNo ratings yet

- Income From House Property: Ms. Harmanpreet Kaur Assistant Professor Shivaji College University of DelhiDocument40 pagesIncome From House Property: Ms. Harmanpreet Kaur Assistant Professor Shivaji College University of DelhiRAKESH KUMAR GOUTAMNo ratings yet

- Annual Value of House PropertyDocument3 pagesAnnual Value of House PropertyAyub ChowdhuryNo ratings yet

- Unit 2 (Income From House Property)Document13 pagesUnit 2 (Income From House Property)Vijay GiriNo ratings yet

- Property Income - July 2023Document5 pagesProperty Income - July 2023maharajabby81No ratings yet

- 02 House Property Notes 23Document14 pages02 House Property Notes 23Hritik HarlalkaNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House Propertyshreshthasethi05No ratings yet

- Income From House Property: Section/Rule Subject MatterDocument21 pagesIncome From House Property: Section/Rule Subject Matterphanidhar varanasiNo ratings yet

- Incomefromhouse Property JeevithaDocument22 pagesIncomefromhouse Property Jeevitharyanraj008No ratings yet

- House Property Exam QP - 9-12-19Document16 pagesHouse Property Exam QP - 9-12-19geddadaarunNo ratings yet

- Chapter-8 (House Property)Document40 pagesChapter-8 (House Property)BoRO TriAngLENo ratings yet

- Tax Law AssignmentDocument18 pagesTax Law AssignmentAditya Pandey100% (1)

- Pre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFDocument106 pagesPre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFParmeet NainNo ratings yet

- Tax ManagementDocument31 pagesTax ManagementrakeshkakaniNo ratings yet

- Income From House PropertyDocument14 pagesIncome From House Propertyjack2529007No ratings yet

- How To Calculate Income From House PropertyDocument3 pagesHow To Calculate Income From House PropertyanjanaNo ratings yet

- Income From HP PDFDocument14 pagesIncome From HP PDFNanda NanduNo ratings yet

- Unit - 2: Income From House Property: After Studying This Chapter, You Would Be Able ToDocument47 pagesUnit - 2: Income From House Property: After Studying This Chapter, You Would Be Able Toadityaraj purohitNo ratings yet

- Income From House Property: Chapter - 4 Unit - 3Document24 pagesIncome From House Property: Chapter - 4 Unit - 3srinidhivrNo ratings yet

- Wealth TaxDocument36 pagesWealth TaxGourav BhattacharjeeNo ratings yet

- Tax Law - I: Income From House PropertyDocument23 pagesTax Law - I: Income From House PropertyArghia -No ratings yet

- Heads of Income TaxDocument6 pagesHeads of Income Taxkanchan100% (1)

- Direct Tax-1Document17 pagesDirect Tax-1Akash GholapNo ratings yet

- Income Under The Head "Income From House Property" and Its ComputationDocument20 pagesIncome Under The Head "Income From House Property" and Its ComputationAanchal SinghalNo ratings yet

- 56465bos45796cp4u2 PDFDocument49 pages56465bos45796cp4u2 PDFNarendra VasavanNo ratings yet

- Deductions From House Property IncomeDocument6 pagesDeductions From House Property Incomedinesh babuNo ratings yet

- Income Tax Law & PracticeDocument32 pagesIncome Tax Law & PracticeGautam TamtaNo ratings yet

- Definations: Income TaxDocument6 pagesDefinations: Income Taxsini rayNo ratings yet

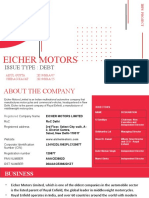

- Eicher Motors Issue Type PresentationDocument16 pagesEicher Motors Issue Type PresentationIshaan DuaNo ratings yet

- Sheela Foam LTD.: Issue Type: DebtDocument15 pagesSheela Foam LTD.: Issue Type: DebtIshaan DuaNo ratings yet

- Sheela Foam LTD.: Issue Type: DebtDocument15 pagesSheela Foam LTD.: Issue Type: DebtIshaan DuaNo ratings yet

- A 039 035 FinalDocument23 pagesA 039 035 FinalIshaan DuaNo ratings yet

- Ishaan Dua (2k19-Bba-39) Harshit Bhatia (2k19-Bba-39) Ibfs Mte ProjectDocument15 pagesIshaan Dua (2k19-Bba-39) Harshit Bhatia (2k19-Bba-39) Ibfs Mte ProjectIshaan DuaNo ratings yet

- KUMAR BIRLA Entrepreneur PresentationDocument8 pagesKUMAR BIRLA Entrepreneur PresentationIshaan DuaNo ratings yet

- Ishaan Dua: EducationDocument2 pagesIshaan Dua: EducationIshaan DuaNo ratings yet

- Tanedo Vs CADocument4 pagesTanedo Vs CAVernon ArquinesNo ratings yet

- Missing Persons Act: Acts 2811978, 17/1979 (S, 17), 2911981,2011991,2011994 (SDocument6 pagesMissing Persons Act: Acts 2811978, 17/1979 (S, 17), 2911981,2011991,2011994 (SLarona MogapiNo ratings yet

- Virginia Tax Exemption Code - 84-178Document12 pagesVirginia Tax Exemption Code - 84-178tysontaylorNo ratings yet

- Conduct Rules, Discipline Rules and Leave Rules 6.1 Conduct RulesDocument41 pagesConduct Rules, Discipline Rules and Leave Rules 6.1 Conduct RulesPrathapa Naveen KumarNo ratings yet

- Marx and JusticeDocument9 pagesMarx and JusticeNicholas GichukiNo ratings yet

- Dales Camp MapDocument1 pageDales Camp MapFabianIrsyadNo ratings yet

- THE World Republic of Letters: Pascale CasanovaDocument58 pagesTHE World Republic of Letters: Pascale CasanovaDavidNo ratings yet

- ReyesVsLimjap L 5396Document4 pagesReyesVsLimjap L 5396Cyber QuestNo ratings yet

- 17.republic Vs AFP RetirementDocument2 pages17.republic Vs AFP RetirementJoseph DimalantaNo ratings yet

- Heirs of Tan Eng Kee vs. CA, 341 SCRA 740 (2000)Document11 pagesHeirs of Tan Eng Kee vs. CA, 341 SCRA 740 (2000)Dianne BalagsoNo ratings yet

- Telecommunications and Broadcast Attorneys of The Philippines, Inc. vs. Commission On ElectionsDocument43 pagesTelecommunications and Broadcast Attorneys of The Philippines, Inc. vs. Commission On ElectionsBurn-Cindy AbadNo ratings yet

- Deed of Absolute SaleDocument2 pagesDeed of Absolute SaleJenelle EsongaNo ratings yet

- Canadian Mortgage Calculator: Inputs Balance at TermDocument33 pagesCanadian Mortgage Calculator: Inputs Balance at Termbracilides82No ratings yet

- Friday Foreclosure List For Pierce County, Washington Including Tacoma, Gig Harbor, Puyallup, Bank Owned Homes For SaleDocument13 pagesFriday Foreclosure List For Pierce County, Washington Including Tacoma, Gig Harbor, Puyallup, Bank Owned Homes For SaleTom TuttleNo ratings yet

- Bucton vs. GabarDocument1 pageBucton vs. GabarJesa DumocloyNo ratings yet

- A.t.kamaraj-Corp - Bank-5th FieldDocument8 pagesA.t.kamaraj-Corp - Bank-5th FieldJaya SankarNo ratings yet

- PHD SynopsisDocument12 pagesPHD SynopsisAnanthNo ratings yet

- Insurance LawDocument44 pagesInsurance LawJannelle ParaisoNo ratings yet

- PP 6 - Research Collaboration Agreement - Short TemplateDocument12 pagesPP 6 - Research Collaboration Agreement - Short TemplateNorfadzilah Abd WahabNo ratings yet

- The Political Environment of International BusinessDocument22 pagesThe Political Environment of International BusinessdinescNo ratings yet

- Republic Act 6675Document16 pagesRepublic Act 6675Choi Han KyotNo ratings yet

- Tayabas Land v. SharrufDocument4 pagesTayabas Land v. SharrufQuina IgnacioNo ratings yet

- Transfer To Benefit of Unborn Child Section 13-20: Submitted To: D.R. Nisha JindalDocument25 pagesTransfer To Benefit of Unborn Child Section 13-20: Submitted To: D.R. Nisha JindalriyaNo ratings yet