You might also like

- Project Report On RozyDocument48 pagesProject Report On RozyrimpyanitaNo ratings yet

- Project Report On "A DETAILED STUDY OF RECRUITMENT AND RETENTION STRATEGIES OF FCs IN LIFE INSURANCE INDUSTRY WITH A SPECIAL FOCUS TO HDFC SLIC"Document50 pagesProject Report On "A DETAILED STUDY OF RECRUITMENT AND RETENTION STRATEGIES OF FCs IN LIFE INSURANCE INDUSTRY WITH A SPECIAL FOCUS TO HDFC SLIC"Alisha SharmaNo ratings yet

- Bibhanshu KumarDocument82 pagesBibhanshu KumarAnkur SrivastavNo ratings yet

- A Summar Project Report On "A Collective Study On Retail Marketing and Their Products inDocument105 pagesA Summar Project Report On "A Collective Study On Retail Marketing and Their Products inchandan sharmaNo ratings yet

- Final Bajaj ProjectDocument28 pagesFinal Bajaj Projectjayesh_korna01No ratings yet

- Summer Training ReportDocument52 pagesSummer Training ReportShikha SinghalNo ratings yet

- A Project Report On Recruitment and Selection of Financial Consultant in HDFCDocument90 pagesA Project Report On Recruitment and Selection of Financial Consultant in HDFCBishnujyoti DasNo ratings yet

- Akash 808Document44 pagesAkash 808AKASHNo ratings yet

- Summer Training Report: Submitted in Partial Fulfillment of The Requirement For The Postgraduate Diploma in ManagementDocument8 pagesSummer Training Report: Submitted in Partial Fulfillment of The Requirement For The Postgraduate Diploma in Managementharshdave07No ratings yet

- Project On Insurance SectorDocument72 pagesProject On Insurance Sectormayur9664501232No ratings yet

- Acknowledgement: HDFC Standard Life Insurance CompanyDocument14 pagesAcknowledgement: HDFC Standard Life Insurance CompanyToibaNo ratings yet

- Project Title: Effectiveness of Recruitment and Training Programs For Sales Force A Case Study of HDFC Standard LifeDocument47 pagesProject Title: Effectiveness of Recruitment and Training Programs For Sales Force A Case Study of HDFC Standard Lifeanon_45072No ratings yet

- Name REG Istration No. Programme Address For CorrespondenceDocument39 pagesName REG Istration No. Programme Address For CorrespondencePriti ChauhanNo ratings yet

- Literature Review of HDFC Standard Life InsuranceDocument4 pagesLiterature Review of HDFC Standard Life InsurancewoeatlrifNo ratings yet

- Study of Consumer Awareness and Customer Response Towards Reliance LifeDocument46 pagesStudy of Consumer Awareness and Customer Response Towards Reliance Lifehimsimmc67% (3)

- Summer Training Report: Submitted in Partial Fulfillment of The Requirement For The Postgraduate Diploma in ManagementDocument11 pagesSummer Training Report: Submitted in Partial Fulfillment of The Requirement For The Postgraduate Diploma in ManagementsagarnaikwadeNo ratings yet

- Summer Training Report ON "Recruitment & Selection" At: HDFC Standard Life Insurance Co. Ltd.Document71 pagesSummer Training Report ON "Recruitment & Selection" At: HDFC Standard Life Insurance Co. Ltd.dheeru88_8No ratings yet

- Retention StrategyDocument70 pagesRetention StrategyShivbhushanPandeyNo ratings yet

- 3cet Report On HDFCDocument17 pages3cet Report On HDFCppoooopopopooopopNo ratings yet

- Malathi Nidhila.v Sandhya Murali RaviDocument15 pagesMalathi Nidhila.v Sandhya Murali Ravireddy_1243No ratings yet

- HDFC Repaired 22222Document124 pagesHDFC Repaired 22222rahulsogani123No ratings yet

- Training Report On Ratio Analysis in HDFC Standard Life Insurance.Document75 pagesTraining Report On Ratio Analysis in HDFC Standard Life Insurance.yadavnirmal7No ratings yet

- Project On Insurance SectorDocument75 pagesProject On Insurance SectorHemant SharmaNo ratings yet

- Bikram ProjectDocument85 pagesBikram ProjectSumit DuttaNo ratings yet

- HDFC Selling PolicyDocument103 pagesHDFC Selling PolicydheerajpagalNo ratings yet

- Project Report On Field Study in Insurance SectorDocument86 pagesProject Report On Field Study in Insurance Sectorsunny_choudhary@hotmail.com100% (1)

- To Determine Customer - Thrift Behaviour With ADocument61 pagesTo Determine Customer - Thrift Behaviour With AlingzenpauliNo ratings yet

- HDFC-STNDRD LyfDocument117 pagesHDFC-STNDRD Lyfguptav12349402100% (1)

- HDFC Standard Life Insurance Corporation LimittedDocument37 pagesHDFC Standard Life Insurance Corporation LimittedGyagarin SagolsemNo ratings yet

- A Summer Training Report On HDFC LifeDocument43 pagesA Summer Training Report On HDFC LifeNeel MkpcbmNo ratings yet

- Dmdfndnfdmfndproject TwoDocument96 pagesDmdfndnfdmfndproject TwoSalman QureshiNo ratings yet

- Recuritment and Selection of Idbi Federal Insurance Co. Ltd.Document49 pagesRecuritment and Selection of Idbi Federal Insurance Co. Ltd.Pratibha Negi0% (1)

- Interim Report 15Document14 pagesInterim Report 15Prasant Kumar PradhanNo ratings yet

- Sourin Mukherjee (PG-10-084)Document17 pagesSourin Mukherjee (PG-10-084)ppoooopopopooopopNo ratings yet

- PANDEYDocument38 pagesPANDEYSanobar fatimahNo ratings yet

- Amit Kumar VermaDocument65 pagesAmit Kumar VermaAmitkumar VermaNo ratings yet

- Recruitment & Selection - at ICICI PrudentialDocument97 pagesRecruitment & Selection - at ICICI PrudentialVikas Sharma100% (1)

- Marketing L HDFC Life InsuranceDocument65 pagesMarketing L HDFC Life InsuranceSamuel Davis100% (1)

- Summer Training Report: Distribution Enhancement and Study of Product of HDFC Standard Life Insurance CompanyDocument82 pagesSummer Training Report: Distribution Enhancement and Study of Product of HDFC Standard Life Insurance CompanyVaibhav JainNo ratings yet

- Report For TuritinDocument22 pagesReport For TuritinRakesh ChitraNo ratings yet

- Company Overview: Life InsuranceDocument23 pagesCompany Overview: Life InsuranceChetan NagarNo ratings yet

- Icici Bba ProjectDocument51 pagesIcici Bba ProjectHarsha GuptaNo ratings yet

- HDFC Standard Life Insurance: Final ReportDocument29 pagesHDFC Standard Life Insurance: Final ReportKunal JalanNo ratings yet

- Project Report HDFCDocument58 pagesProject Report HDFCKr Ish NaNo ratings yet

- IDBI Federal Project ReportDocument54 pagesIDBI Federal Project Reportajugalex@gmail,com83% (12)

- A Project Study Report On Titled "Comparative Study of HDFC Standard Life With Tata - Aig Life Insurance"Document114 pagesA Project Study Report On Titled "Comparative Study of HDFC Standard Life With Tata - Aig Life Insurance"garish009100% (1)

- Recruitment and Selection ProcessDocument33 pagesRecruitment and Selection Processurmi_patel22No ratings yet

- Recruitment and Selection Process: ICICI Life Insurance Company LTDDocument45 pagesRecruitment and Selection Process: ICICI Life Insurance Company LTDMuthu PriyaNo ratings yet

- My ProjectDocument93 pagesMy ProjectSaheli Halder100% (2)

- Project Report On BHARTI AXA Life InsuraDocument50 pagesProject Report On BHARTI AXA Life InsuraArvindSinghNo ratings yet

- HDFC LIFE INSURANCE Irm AssignDocument11 pagesHDFC LIFE INSURANCE Irm AssignMilin NagarNo ratings yet

- Recruitment and Selection Process: ICICI Life Insurance Company LTDDocument44 pagesRecruitment and Selection Process: ICICI Life Insurance Company LTDSmruti Ranjan ChhualsinghNo ratings yet

- A Project Report ON: "The Role of Financial Planning in Portfolio Management"Document31 pagesA Project Report ON: "The Role of Financial Planning in Portfolio Management"Shivani BajpeyiNo ratings yet

- Financial Analysis of HDFC LifeDocument77 pagesFinancial Analysis of HDFC LifeSankalp SamantNo ratings yet

- Assessment of Microinsurance as Emerging Microfinance Service for the Poor: The Case of the PhilippinesFrom EverandAssessment of Microinsurance as Emerging Microfinance Service for the Poor: The Case of the PhilippinesNo ratings yet

- The 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesFrom EverandThe 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesNo ratings yet

- 2009 Annual ReportDocument264 pages2009 Annual ReportasangasdNo ratings yet

- IBPS Clerk Prelimsl Previous PaperDocument26 pagesIBPS Clerk Prelimsl Previous PapershakthiNo ratings yet

- Solutions Chapter 5 Balance of PaymentsDocument13 pagesSolutions Chapter 5 Balance of Paymentsfahdly67% (3)

- Nestle Multinational CompanyDocument3 pagesNestle Multinational CompanyShebel AgrimanoNo ratings yet

- The Role of Sustainability in Brand Equity Value in The Financial SectorDocument19 pagesThe Role of Sustainability in Brand Equity Value in The Financial SectorPrasiddha PradhanNo ratings yet

- This Study Resource Was: Correct!Document5 pagesThis Study Resource Was: Correct!Angelie De LeonNo ratings yet

- Notes To Finacial Statements: Question 6-1Document23 pagesNotes To Finacial Statements: Question 6-1Kim FloresNo ratings yet

- FOREXDocument7 pagesFOREXpoppy2890No ratings yet

- Canvass: Capturing News With An Analytical EdgeDocument6 pagesCanvass: Capturing News With An Analytical EdgeRanjith RoshanNo ratings yet

- Working Capital and Current Assets Management: Learning GoalsDocument2 pagesWorking Capital and Current Assets Management: Learning GoalsKristel SumabatNo ratings yet

- Act 3122 Intermediate Financial Accounting Ii: Lecturer: Dr. Mazrah Malek Room: A302Document10 pagesAct 3122 Intermediate Financial Accounting Ii: Lecturer: Dr. Mazrah Malek Room: A302Shahrul FadreenNo ratings yet

- Q & A - Test 1 Acc106 - 114Document8 pagesQ & A - Test 1 Acc106 - 114Jamilah EdwardNo ratings yet

- Egypt's Cement Industry Still Growing Strong: Expansion ProjectsDocument6 pagesEgypt's Cement Industry Still Growing Strong: Expansion ProjectsMohamed Ahmed ElsangaryNo ratings yet

- Itm 11. Interpreneureship With Fundamentals of CooperativeDocument20 pagesItm 11. Interpreneureship With Fundamentals of Cooperativelaliy palaciosNo ratings yet

- Entrepreneurship and Small Business Management Diana DumitruDocument14 pagesEntrepreneurship and Small Business Management Diana DumitruDumitru Dragos RazvanNo ratings yet

- AFC 1000 Exam 2012 S2Document9 pagesAFC 1000 Exam 2012 S2tusharNo ratings yet

- GMAT Practice Set 13 - VerbalDocument73 pagesGMAT Practice Set 13 - VerbalKaplanGMATNo ratings yet

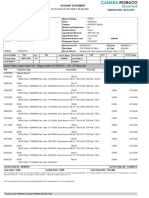

- Canara Robeco Equity Hybrid Fund - Regular Monthly IDCW (GBDP) - ISIN: INF760K01068Document2 pagesCanara Robeco Equity Hybrid Fund - Regular Monthly IDCW (GBDP) - ISIN: INF760K01068brotoNo ratings yet

- Regulatory Deferral Accounts: IFRS Standard 14Document24 pagesRegulatory Deferral Accounts: IFRS Standard 14Teja JurakNo ratings yet

- Wrigley Gum 21Document18 pagesWrigley Gum 21Fidelity RoadNo ratings yet

- Leges Et Ivra P. R. Restitvit. A New Aureus of Octavian and The Settlement of 28-27 BC - J.W. Rich and J.H. C. Williams (The Numismatic Chronicle, Vol. 159, 1999) PDFDocument48 pagesLeges Et Ivra P. R. Restitvit. A New Aureus of Octavian and The Settlement of 28-27 BC - J.W. Rich and J.H. C. Williams (The Numismatic Chronicle, Vol. 159, 1999) PDFjamuleti1263100% (1)

- Corporate Profile - M&M Labour and Business Consultancy - Sir. AshleyDocument15 pagesCorporate Profile - M&M Labour and Business Consultancy - Sir. AshleyAshley MukweshaNo ratings yet

- Firestone CaseDocument2 pagesFirestone Caseel060275100% (2)

- Chapter 10Document36 pagesChapter 10chiny0% (1)

- Agricultural Banking of PakistanDocument28 pagesAgricultural Banking of PakistanAdeel ChaudharyNo ratings yet

- The Pitch and Business Plan For Investors and Partners PDFDocument6 pagesThe Pitch and Business Plan For Investors and Partners PDFparamedicboy1No ratings yet

- Business Policy and Strategic ManagementDocument89 pagesBusiness Policy and Strategic Managementanmol100% (1)

- Why Europe Planned The Great Bank RobberyDocument2 pagesWhy Europe Planned The Great Bank RobberyRakesh SimhaNo ratings yet

- Case 3: Rockboro Machine Tools Corporation Executive SummaryDocument1 pageCase 3: Rockboro Machine Tools Corporation Executive SummaryMaricel GuarinoNo ratings yet

- Murray Scott 050111 ResumeDocument2 pagesMurray Scott 050111 Resumescottm8571No ratings yet