You might also like

- Flash Memory AnalysisDocument25 pagesFlash Memory AnalysisTheicon420No ratings yet

- Seagate NewDocument22 pagesSeagate NewKaran VasheeNo ratings yet

- Sampa Video Case ExhibitsDocument1 pageSampa Video Case ExhibitsOnal RautNo ratings yet

- This Study Resource Was: Case Study - Flash Memory, IncDocument6 pagesThis Study Resource Was: Case Study - Flash Memory, IncWill TrầnNo ratings yet

- Debt Policy at UST Inc.Document11 pagesDebt Policy at UST Inc.Omkar BibikarNo ratings yet

- Final Exam Solutions 2012 1 SpringDocument123 pagesFinal Exam Solutions 2012 1 SpringBenny KhorNo ratings yet

- Debt Policy at UST IncDocument5 pagesDebt Policy at UST Incggrillo73No ratings yet

- Flash Memory IncDocument3 pagesFlash Memory IncAhsan IqbalNo ratings yet

- Mercury Athletic CaseDocument3 pagesMercury Athletic Casekrishnakumar rNo ratings yet

- Flash MemoryDocument9 pagesFlash MemoryJeffery KaoNo ratings yet

- Flash Memory AnalysisDocument25 pagesFlash Memory AnalysisaamirNo ratings yet

- Flash Memory IncDocument9 pagesFlash Memory Incxcmalsk100% (1)

- Fin 321 Case PresentationDocument19 pagesFin 321 Case PresentationJose ValdiviaNo ratings yet

- This Study Resource Was: Gain Control of Robertson Tool in May 2003?Document4 pagesThis Study Resource Was: Gain Control of Robertson Tool in May 2003?Pedro José ZapataNo ratings yet

- Sampa VideoDocument24 pagesSampa VideodoiNo ratings yet

- Flow Valuation, Case #KEL778Document20 pagesFlow Valuation, Case #KEL778SreeHarshaKazaNo ratings yet

- FlashMemory SLNDocument6 pagesFlashMemory SLNShubham BhatiaNo ratings yet

- Final AssignmentDocument15 pagesFinal AssignmentUttam DwaNo ratings yet

- New Heritage DoolDocument9 pagesNew Heritage DoolVidya Sagar KonaNo ratings yet

- Flow Valuation, Case #KEL778Document31 pagesFlow Valuation, Case #KEL778javaid jamshaidNo ratings yet

- History of Human Resources Management in The PhilippinesDocument10 pagesHistory of Human Resources Management in The Philippinesmarjo617100% (1)

- Payroll and Benefits PDFDocument16 pagesPayroll and Benefits PDFNeha MohnotNo ratings yet

- Jules Michelet's "L'amour" or "Love"Document368 pagesJules Michelet's "L'amour" or "Love"rsjonmoeas100% (1)

- MgtOp 340 Topic 5Document31 pagesMgtOp 340 Topic 5ranjitd07No ratings yet

- In The Court of District & Sessions Judge, Rajkot Bail Application No. 106 of 2019Document4 pagesIn The Court of District & Sessions Judge, Rajkot Bail Application No. 106 of 2019Deep HiraniNo ratings yet

- Ocean Carriers - Case (Final)Document18 pagesOcean Carriers - Case (Final)Namit LalNo ratings yet

- Queen's SquareDocument45 pagesQueen's SquareGarifuna NationNo ratings yet

- Evaluation of Digital Realty Trust IncDocument18 pagesEvaluation of Digital Realty Trust Incwafula stanNo ratings yet

- Sun Microsystems Case JasdeepDocument6 pagesSun Microsystems Case JasdeepJasdeep SinghNo ratings yet

- Sprint Rebuts AT&T and T-Mobile MergerDocument299 pagesSprint Rebuts AT&T and T-Mobile MergerJonathan Fingas100% (1)

- Group-13 Case 12Document80 pagesGroup-13 Case 12Abu HorayraNo ratings yet

- Fullan 8 Forces AnalysisDocument6 pagesFullan 8 Forces Analysisranjitd07No ratings yet

- Flash Memory Inc Student Spreadsheet SupplementDocument5 pagesFlash Memory Inc Student Spreadsheet Supplementjamn1979No ratings yet

- Case: Flash Memory, Inc. (4232)Document1 pageCase: Flash Memory, Inc. (4232)陳子奕No ratings yet

- Flash Memory, Inc. - Group 8Document1 pageFlash Memory, Inc. - Group 8Bryan MezaNo ratings yet

- Radent Case QuestionsDocument2 pagesRadent Case QuestionsmahieNo ratings yet

- Flash Memory, Inc.Document2 pagesFlash Memory, Inc.Stella Zukhbaia0% (5)

- Finance Simulation - Capital BudgetingDocument1 pageFinance Simulation - Capital BudgetingKarthi KeyanNo ratings yet

- Michael McClintock Case1Document2 pagesMichael McClintock Case1Mike MCNo ratings yet

- Jet IPO ValuationDocument2 pagesJet IPO Valuationprtkshnkr50% (2)

- 25th June - Sampa VideoDocument6 pages25th June - Sampa VideoAmol MahajanNo ratings yet

- Wells Fargo CaseDocument58 pagesWells Fargo CaseMeenaNo ratings yet

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasDocument2 pagesDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005No ratings yet

- Mckenzie CorporationDocument2 pagesMckenzie CorporationVipin KumarNo ratings yet

- Mercury Athletic Historical Income StatementsDocument18 pagesMercury Athletic Historical Income StatementskarthikawarrierNo ratings yet

- XLS EngDocument26 pagesXLS EngcellgadizNo ratings yet

- Mariott Corp AnalysisDocument14 pagesMariott Corp AnalysisvarjinNo ratings yet

- CASE Exhibits - HertzDocument15 pagesCASE Exhibits - HertzSeemaNo ratings yet

- In-Class Project 2: Due 4/13/2019 Your Name: Valuation of The Leveraged Buyout (LBO) of RJR Nabisco 1. Cash Flow EstimatesDocument5 pagesIn-Class Project 2: Due 4/13/2019 Your Name: Valuation of The Leveraged Buyout (LBO) of RJR Nabisco 1. Cash Flow EstimatesDinhkhanh NguyenNo ratings yet

- Shimano 3Document14 pagesShimano 3Tigist AlemayehuNo ratings yet

- Section A - Group DDocument6 pagesSection A - Group DAbhishek Verma100% (1)

- DCF Application - Asian PaintsDocument6 pagesDCF Application - Asian PaintsKashish PopliNo ratings yet

- Caso TeuerDocument46 pagesCaso Teuerjoaquin bullNo ratings yet

- Wikler Case Competition PowerpointDocument16 pagesWikler Case Competition Powerpointbtlala0% (1)

- Ejercicio 7.5Document6 pagesEjercicio 7.5Enrique M.No ratings yet

- APV and EVA Approach of Firm Valuation Module 8 (Class 37 and 38)Document23 pagesAPV and EVA Approach of Firm Valuation Module 8 (Class 37 and 38)Vineet AgarwalNo ratings yet

- PS4 SolutionsDocument17 pagesPS4 SolutionsShreyas DalviNo ratings yet

- Mercury Athletic QuestionsDocument1 pageMercury Athletic QuestionsRazi UllahNo ratings yet

- Bed Bath Beyond (BBBY) Stock ReportDocument14 pagesBed Bath Beyond (BBBY) Stock Reportcollegeanalysts100% (2)

- M&a Assignment - Syndicate C FINALDocument8 pagesM&a Assignment - Syndicate C FINALNikhil ReddyNo ratings yet

- Uk Gilts - Analysis of Bond Investments: (Revised Submission)Document6 pagesUk Gilts - Analysis of Bond Investments: (Revised Submission)Mayuresh D PradhanNo ratings yet

- RJR Nabisco ValuationDocument33 pagesRJR Nabisco ValuationKrishna Chaitanya KothapalliNo ratings yet

- 10 BrazosDocument20 pages10 BrazosAlexander Jason LumantaoNo ratings yet

- Tire City AssignmentDocument6 pagesTire City AssignmentXRiloXNo ratings yet

- Harley DavidsonDocument4 pagesHarley DavidsonExpert AnswersNo ratings yet

- Group BDocument10 pagesGroup BHitin KumarNo ratings yet

- Case 3 Nikki 111Document6 pagesCase 3 Nikki 111Mahmudur Rahman TituNo ratings yet

- MFL06477229 MC-7689MSRDocument44 pagesMFL06477229 MC-7689MSRranjitd07No ratings yet

- Nike Inc., Price To Earnings (P/E) : Selected Financial Data (USD $)Document10 pagesNike Inc., Price To Earnings (P/E) : Selected Financial Data (USD $)ranjitd07No ratings yet

- Anheier Institutional Voids BrnoDocument32 pagesAnheier Institutional Voids Brnoranjitd07No ratings yet

- Eskimo Pie Case 2006Document10 pagesEskimo Pie Case 2006Luiz EduardoNo ratings yet

- 25 Years of HIV - Africa and Beyond: Carol Ciesielski, MDDocument68 pages25 Years of HIV - Africa and Beyond: Carol Ciesielski, MDranjitd07No ratings yet

- Common Mistakes in Interpretation of Regression CoefficientsDocument2 pagesCommon Mistakes in Interpretation of Regression Coefficientsranjitd07No ratings yet

- MGMT 469 Regression BasicsDocument26 pagesMGMT 469 Regression Basicsranjitd07No ratings yet

- Kitting: Slide 3Document5 pagesKitting: Slide 3ranjitd07No ratings yet

- ICMAI Registration ProcessDocument1 pageICMAI Registration Processranjitd07No ratings yet

- Weighted Average Cost of Capital: Timothy A. Thompson Executive Masters ProgramDocument24 pagesWeighted Average Cost of Capital: Timothy A. Thompson Executive Masters Programranjitd07No ratings yet

- Deepak Yadav (@deepakyadav0047)Document11 pagesDeepak Yadav (@deepakyadav0047)Deepak YadavNo ratings yet

- 168-2013 - Approval Authorities L CategoryDocument5 pages168-2013 - Approval Authorities L CategoryDevaraj DHANAKOTTINo ratings yet

- Chapter-4 Business Acquisition & FranchaisingDocument35 pagesChapter-4 Business Acquisition & FranchaisingLowzil Rayan AranhaNo ratings yet

- TEH Study Questions 5.6Document3 pagesTEH Study Questions 5.6Summit Woods Baptist ChurchNo ratings yet

- Myanmar Customer List For SteelDocument3 pagesMyanmar Customer List For SteelCao SonNo ratings yet

- Despawn The OnionDocument2 pagesDespawn The OnionfsasfaNo ratings yet

- Araling PanlipunanDocument4 pagesAraling PanlipunanRoland Dave Vesorio EstoyNo ratings yet

- An Analysis On Music Entertainment From The Perspective Fourth Year Students of Fiqh and FatwaDocument24 pagesAn Analysis On Music Entertainment From The Perspective Fourth Year Students of Fiqh and FatwaMOHAMMAD NoumaanNo ratings yet

- History Lecture 8 Notes PDFDocument3 pagesHistory Lecture 8 Notes PDFHari KrishnaNo ratings yet

- CRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesDocument110 pagesCRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesKyle Ethan AringoNo ratings yet

- Discrimination in Emloyment LawDocument1 pageDiscrimination in Emloyment LawFrancis Njihia KaburuNo ratings yet

- Stock Exchange Project BSTDocument12 pagesStock Exchange Project BSTJay NegiNo ratings yet

- Compilation of HadithDocument11 pagesCompilation of HadithMuiz “Daddy” AyubiNo ratings yet

- Scalpers.comDocument5 pagesScalpers.comDomainNameWireNo ratings yet

- 2015-16 SARS ELogbookDocument17 pages2015-16 SARS ELogbookmhassim123No ratings yet

- 4.0 AkhlaqDocument49 pages4.0 Akhlaqmmasfufah97No ratings yet

- Types of Crime MappingDocument32 pagesTypes of Crime MappingThelma Avelina Garcia CadivinNo ratings yet

- Tazkira Ullama e Ahle Sunnat by Mehmood Ahmad QadriDocument135 pagesTazkira Ullama e Ahle Sunnat by Mehmood Ahmad QadriTariq Mehmood Tariq100% (3)

- EEE 1 Meeting 2 - Circuit Elements. KCL, KVL, Circuit SimplificationDocument26 pagesEEE 1 Meeting 2 - Circuit Elements. KCL, KVL, Circuit SimplificationCyril John Caraig NarismaNo ratings yet

- New History of KoreaDocument8 pagesNew History of Koreapeter_9_11No ratings yet

- QuotationDocument44 pagesQuotationTusharGuptaNo ratings yet

- BECG-2 Ethical Concepts and TheoriesDocument26 pagesBECG-2 Ethical Concepts and Theoriesshefalibaid71% (7)

- Full Ebook of Aspen Treatise For National Security Law 2Nd Edition Geoffrey Corn Online PDF All ChapterDocument69 pagesFull Ebook of Aspen Treatise For National Security Law 2Nd Edition Geoffrey Corn Online PDF All Chapterjociyeini100% (13)

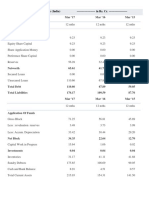

- Balance Sheet of Shakti PumpsDocument2 pagesBalance Sheet of Shakti PumpsAnonymous 3OudFL5xNo ratings yet